.png)

TL;DR

Family wealth protection succeeds when governance, education, cybersecurity, disciplined investing, and a modern operating stack work together. Utilize a unified system, such as Asora, to consolidate entities, holdings, documents, and tasks into a single view. This enhances wealth preservation, mitigates operational risk, and helps safeguard family wealth for future generations.

Why This Guide Matters

A modern family office touches many moving parts. There are operating companies, private funds, real estate vehicles, bank accounts, life insurance, and personal assets that matter both emotionally and financially. When information is stored in separate spreadsheets and email threads, no one sees the complete picture. Reports arrive late, approvals are delayed, and minor errors become costly.

A single system that records what the family owns, who makes the decisions, and which documents prove each position changes the tempo. The office operates on facts rather than guesswork; advisors view the same evidence, and the family can plan with confidence. Understanding the family's financial situation is crucial for developing an effective protection plan that addresses current needs and future goals. It also clarifies how to protect family wealth through repeatable habits.

Comprehensive wealth planning is crucial for high-net-worth individuals to protect their family's wealth across generations. This guide lays out practical ways to protect family wealth and links each step to habits that keep the plan alive.

Why Family Wealth Protection Matters Now

Intergenerational transfers are growing in size and frequency. Families are moving ownership of companies, properties, and portfolios while also teaching the next generation how to lead. The risk is not only market volatility or a single poor investment decision. The larger risk is a lack of shared information and unclear responsibility. If no one knows which version of the spreadsheet is final, or if a key document is missing when a bank or auditor asks for it, the family loses time and leverage.

Protection of family wealth begins with a shared understanding of assets, liabilities, and roles, ensuring that decisions are made quickly and are defensible. A Williams Group study found that the majority of family wealth transfers fail by the third generation, underscoring the need for proactive planning to avoid significant financial losses.

Private markets add another layer. Capital calls, waterfalls, side letters, carried interest, and partnership accounting complicate performance and tax treatment. Without a system that understands these mechanics, it becomes difficult to measure exposure, forecast liquidity, or model tax liability.

When the data is accurate and current, advisors can develop an effective estate plan, evaluate asset protection trusts, and identify tax-efficient strategies to minimize estate and income taxes over time. Good information does not remove hard choices, yet it makes every choice clearer.

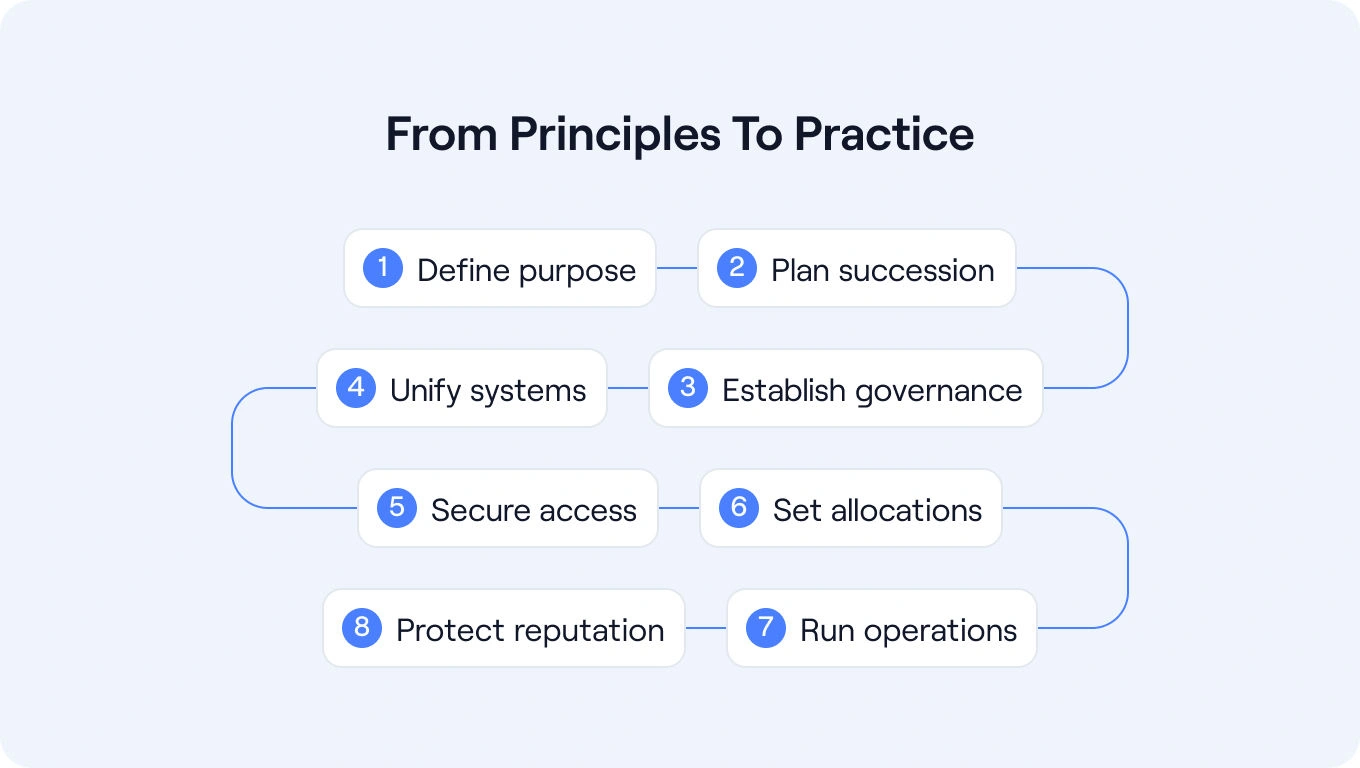

From Principles to Practice

The eight steps that follow move from purpose and people into data, technology, and daily routines. Each section builds on the one before it, so the plan is a connected program rather than a checklist. The goal is to create a family wealth protection plan that a small team can manage effectively, supporting long-term financial success through comprehensive wealth planning. The outcome is a practical set of strategies to protect family wealth the team can run.

Step 1. State the Purpose of Wealth and the Rules That Govern It

Every successful program for family wealth protection starts with a short statement that explains why the wealth exists and what it must achieve. Some families prioritize long-term ownership of a successful business. Others want to fund education, charitable giving, or new ventures. Write this down and store it in a location where all stakeholders can access it. Then define the rules that shape decisions. These include spending policy, liquidity needs, risk tolerance, and lines that cannot be crossed. Clear rules and structures are essential for safeguarding assets against legal and economic risks. Document the scope of the balance sheet. Include operating companies, real estate vehicles, private funds, bank accounts, art, carried interest, and digital assets. When everyone understands the purpose and rules, discussions move faster and become less personal. This is the first foundation for key strategies that protect wealth.

Link these choices to tax planning early. A clear purpose helps align asset protection with estate planning. If the objective is to preserve wealth for future generations, the plan may lean toward trusts that separate trust assets from personal creditors. If the objective is to seed new ventures, the plan may favor structures that allow tax-efficient funding and clear decision rights.

Step 2. Put Succession on a Calendar and Make Progress Visible

Succession planning is effective when it follows a well-defined timetable. Define decision rights for investments, distributions, divestments, and reputational matters. Map a training path for each heir that covers accounting basics, portfolio construction, fund mechanics, estate planning, and governance etiquette. Assign mentors and set dates for shadowing, co-decision making, and full responsibility. Record responsibilities, milestones, and reviews inside your operating system so progress is visible.

Having context turns training into participation and creates a trail that advisors and auditors can follow. Preparing the next generation is one of the most effective ways to protect family wealth, as it reduces the likelihood of missteps when control of the family wealth changes hands.

Business succession planning deserves the same discipline. Where a family owns a controlling interest in an operating company, document management succession, board composition, and a buy-sell agreement that sets terms for transfers at an owner's death or disability. Buy-sell agreements are often funded by life insurance policies, which provide liquidity to facilitate the transfer of ownership at the owner's death. These steps protect the business, reduce disputes among family members, and provide creditor protection where permitted by law.

Step 3. Build a Governance Framework That Keeps Pace with Growth

Families need forums that meet regularly and make decisions with confidence. Establish a family council to discuss values and policies. Create an investment and risk forum that reviews performance, pipeline, and exposures on a set cadence. It is worth inviting outside expertise where it adds value. Circulate concise materials before each meeting, record the decisions, and track actions to close.

A governance framework operates most effectively when it is tied to a document vault and utilizes repeatable workflows. Organizing estate planning documents, such as wills and trusts, in a secure document vault is crucial for protecting assets and ensuring a seamless inheritance.

Regular family meetings reinforce the plan. They align expectations, surface risks early, and ensure each family member understands the estate plan, the financial plan, and the steps required to transfer generational wealth responsibly.

Step 4. Replace Manual Spreadsheets With a Unified Operating System

Spreadsheets are powerful for analysis, but they are not a system of record. When multiple versions circulate, no one is sure which number is final. When access is not controlled, sensitive information is exposed. When workbooks grow, they slow down and break. A unified operating system addresses these problems by consolidating entities, people, accounts, and holdings into a single model. It reconciles transactions, calculates performance across currencies and entities, and provides look-through reporting across funds and direct holdings.

A modern system must also handle the documents that prove positions. Subscription agreements, capital call notices, distribution statements, valuation memos, and bank advices belong next to the assets they describe. With Asora, families transition from scattered folders to a structured vault, where every document is linked to the relevant investment, entity, and task. That single source of truth is the core of family wealth protection because it replaces fragile processes with repeatable ones and supports clean financial management.

Step 5. Treat Cybersecurity as a Financial Risk and Manage it Accordingly

Affluent families are targets for cybercrime. Attackers look for weak passwords, shared logins, unsecured email threads, and flat permissioning. A strong defense starts with access management. Every user signs in with multi-factor authentication. Each role has the minimum rights necessary to perform its duties. Data is encrypted in transit and at rest. Sensitive documents are shared securely rather than attached to an email. Vendors are reviewed for certifications, data residency, and incident response.

Cybersecurity is also behavior. Drills and phishing simulations reduce incidents and speed recovery because roles are defined and practiced. Embedding these practices in the same system that manages assets shortens the gap between the discovery of a risk and the action taken to remediate it.

Step 6. Build an Allocation That Can Be Governed and Monitor It Continuously

An allocation is only helpful if it can be implemented and overseen. Translate the family's purpose into policy ranges for cash, credit, equities, tangible assets, and alternative investments. Map liquidity against obligations such as capital calls, tax payments, and distributions to each family member. Determine how performance will be measured and what actions will be taken when exposures deviate outside the agreed-upon ranges. Document the circumstances that will trigger trimming, distribution, or exit so there is no guesswork during periods of stress.

Monitoring turns policy into control. Dashboards that highlight allocation, concentration, liquidity, and performance against objectives help families act early. With Asora, teams can track commitments, capital calls, and distributions to stay ahead of key actions. That visibility links strategy to timely execution and supports tax planning by providing advisors with up-to-date data on performance, gains, income, and cash activity before transactions are posted.

Step 7. Operationalize the Back Office so Tasks, Timelines, and Evidence Align

Value often leaks in the back office. Missed filings, late partner statements, unclaimed fee offsets, orphaned vehicles, and unsigned resolutions create cost and reputational risk. Close these gaps by converting recurring obligations into standard workflows. Onboarding a new investment should follow the same steps each time. Quarter-end and year-end should follow the same sequence. Requests for signatures, bank details, and valuations should be tracked from assignment to completion so nothing is forgotten during travel or holidays. Asora includes task management that sits next to your assets, accounts, entities, and documents. When a task is tied to the object it affects, the owner has the proper context, and reviewers can see status and activity in the shared workspace. Evidence is stored in the Document Vault, linked to the relevant records rather than being buried in personal inboxes. This improves reliability without adding headcount, making reviews and audits easier.

Step 8. Protect the Family Name, Narrative, and Asset Protection as Carefully as the Balance Sheet

Reputation compounds like capital. A respected family name opens doors with counterparties, communities, and future partners. Treat it with the same discipline applied to assets. Define how the name is used across operating companies, philanthropic initiatives, and public statements. Create a concise communications policy that explains who speaks, when they speak, and how decisions are reviewed. Store approved statements and media materials in the secure vault so everyone works from the latest version. A straightforward narrative helps the next generation. When heirs understand the history and purpose behind major decisions, they feel a deeper connection to the legacy. Protecting family wealth is about more than portfolio construction. It also encompasses the identity, relationships, and trust that have been built over the course of decades. A study found that 70% of families lose their capital in the second generation and 90% in the third, underscoring the importance of disciplined planning and communication.

Data Governance & Accuracy Standards for Family Offices

Adequate protection starts with clean, consistent data. A single register of entities, people, accounts, and holdings forms the backbone and stays current as structures evolve. Ownership and decision-making rights are clearly defined, including look-through interests across funds and special-purpose vehicles. Private assets receive the same level of attention as bankable securities, with commitments, capital calls, distributions, valuation details, fee terms, side letters, and notes all captured in a single model. When these details are organized together in Asora rather than scattered across files, advisors and principals work from the same evidence and act with confidence.

Accuracy rests on rhythm as much as rules. Feeds bring in banking and investment activity, allowing the team to view up-to-date positions. Validation occurs during the submission process, with required fields and sensible ranges, and records include supporting documents that justify each figure. Exceptions become work, not email: owners, due dates, and resolutions live inside workflows, so nothing disappears into inboxes.

Documents provide the proof behind the numbers. Subscription agreements, capital call notices, statements, valuation memos, and resolutions are stored in Asora's secure vault and linked directly to the position, entity, or task they support. Retention follows office policy, and access changes when roles change. Sensitive material remains in the right hands without slowing the pace of work.

Access mirrors responsibility. Role-based permissions ensure each person sees only what their role requires, with sign-in protected by multi-factor authentication. Data is encrypted both in transit and at rest, and activity related to tasks and documents is captured within the shared workspace. The result is a dependable operating core where data, documents, and decisions remain connected, and operational risk is mitigated across jurisdictions.

Technology-Enabled Wealth Planning & Decision-Making

Technology enhances the quality of planning by shortening the distance between facts and action. Aggregation across banks, custodians, and administrators gives a current picture of balances, flows, and exposures. Look-through reporting across entities, funds, and direct investments makes concentration and liquidity more transparent. With the whole picture in one place, planning conversations begin with what is true today, rather than last quarter's estimates.

Decision-making improves when models are grounded in real records. Capital commitments, call schedules, distributions, and performance sit beside the documents that support them, creating context for advisors and principals. Tasks, alerts, and approvals ensure key steps are completed on time, whether preparing a report, funding a call, or conducting a review. During periods of stress, timely visibility and notifications help the team act promptly and document what changed and why.

Traceability strengthens confidence. Proposals, decisions, and supporting files are located next to the assets they affect, allowing the office to retain a clear record of an allocation shift, a valuation update, or an approval. External advisors participate in a shared view with role-based access, which reduces rework and speeds up outcomes.

Asora is built for this flow. Performance, exposure, cash activity, and private-asset events are presented alongside documents and workflows, allowing a discussion to transition directly to an action and an action to a recorded result. Mobile apps keep principals informed on the go without widening risk. The outcome is a quieter operation with fewer surprises, cleaner reviews, and a planning cycle that keeps pace with the family's ambitions.

Investment Discipline That Preserves Optionality

Preserving wealth requires a balance between return seeking and risk control across the investment portfolio. Many families hold concentrated positions in an operating company or a favored sector. Concentration can build fortune, and it can increase vulnerability. A risk budget helps. The budget sets the maximum exposure to any issuer, manager, or theme and links that exposure to family purpose and spending policy. Liquidity deserves equal attention. Capital calls arrive on their own schedule. Tax events are certain even when markets are not. A liquidity schedule that looks forward by quarter and by year prevents forced sales and supports a more stable financial plan.

Monitoring is the daily expression of control. In Asora, performance attribution and exposure by asset classes appear in the same dashboard. When a threshold is breached, the person completes the necessary action, documenting the process. This enhances financial security, fosters a disciplined approach to wealth management, and mitigates stress during periods of market volatility.

Cybersecurity Woven Into Daily Habits

Security improves when it is integrated into everyday work rather than being a separate project. Team members sign in with multi-factor authentication. Documents are stored in the vault rather than as email attachments. Vendors are thoroughly reviewed before onboarding and closely monitored throughout the duration of the relationship. When an incident occurs, the response follows a script that is rehearsed and documented. These habits embed family wealth protection into daily behavior.

Some worry that controls will slow work. In practice, clear roles and secure sharing replace improvisation with routine. People spend less time searching for files and more time reviewing the information that matters to them. Advisors appreciate clean data and complete histories. The cumulative effect is a quieter operation with fewer surprises and better creditor protection, where legal structures permit, because ownership and authority are documented.

People and Culture

Family wealth protection runs on people. Systems still require clear communication and respect. Provide education that fits roles. Principals benefit from concise dashboards that keep them oriented. Next-generation members benefit from sessions that explain the mechanics of the private market, the logic behind allocation, and the purpose behind the rules. Staff benefit from refreshers on the system, on control procedures, and on cybersecurity. Each audience learns enough to perform its part and to understand how actions affect the whole. Regular family meetings reinforce the plan, keep the estate plan current, and ensure each family member understands how the parts fit together.

Implementation Roadmap

Turning strategy into reality works best with a short initial phase followed by steady refinement. Set objectives for the first quarter that include a complete entity register, a clean list of accounts, a portfolio import, and a secure document vault for priority positions. Configure the first reports to answer the questions principals ask most often. Load the first wave of governance meetings with owners and dates. Begin the training path for the next generation and assign mentors.

Once the core is stable, extend the scope. Bring in capital call schedules, look through fund exposures, and performance attribution by strategy and manager. Layer in more granular permissions as roles expand. Review cybersecurity posture and set a schedule for drills. This measured approach delivers momentum and builds confidence.

How Asora Supports the Plan

Asora serves families who want the clarity of an institutional view without an institutional-style implementation. The system aggregates data across entities and asset classes, storing the documents linked to each entity, asset, or account. Workflows and task management sit alongside the records they reference, so work has context. Performance reporting with look-through transparency across entities enables stakeholders to view underlying holdings and structures at a glance.

Mobile apps for iOS and Android provide secure, on-the-go access to portfolio data and documents. The data model treats private assets as first-class: SPVs, partnerships, and direct deals sit alongside marketable securities. Families can track commitments, capital calls, and distributions for private investments and view their exposure to funds and direct investments in one place, with bank and custodian data available through aggregation. The result is less manual effort and fewer tools, so a lean office can maintain strong control with a small team.

What to Do Next

Protecting family wealth is the operating rhythm of a modern family office. State the purpose and the rules. Schedule a handover and make progress visible. Build a governance framework that meets and decides. Replace scattered spreadsheets with a shared system that holds data, documents, and tasks together. Treat cybersecurity with the same seriousness as market risk. Run the back office with repeatable workflows. Protect the family name and narrative alongside the balance sheet.

Families that adopt this approach gain control quickly. They see cleaner reports, faster closes, and fewer surprises. Advisors work from the same facts. Audits are smoother. Most importantly, the next generation joins a system that supports good decisions. With Asora as the backbone, families move from fragmented tools to an integrated practice that preserves capital, reputation, and opportunity across generations. Book a demo to learn more.

FAQ

Can a family wealth protection platform handle private assets or only bankable securities?

A system designed for families can handle both. Asora supports special purpose vehicles, partnerships, capital accounts, waterfalls, capital calls and distributions, and look-through exposure across funds and directs. This capability is crucial for protecting family wealth when private markets comprise a significant portion of the investment portfolio.

How long does it take to see value?

Lean single family offices typically stand up core entities, accounts, and initial reporting in a matter of weeks. Because the focus is on the data that matters first, useful dashboards are created quickly, and the team can gradually retire spreadsheets. That early momentum encourages adoption and keeps the program moving.

What changes for family wealth protection once the data is unified?

Responsibilities and approvals should not live in inboxes. Heirs gain a clear view of assets, documents, and the decisions made. Tasks guide participation and create a history that mentors can review and reference for future reference. When control passes, the new principals inherit a system as well as a portfolio. That supports business succession planning and helps protect family wealth by reducing reliance on a few individuals.

How does Asora ensure the security of documents and data?

Data is encrypted in transit and at rest. Access is granted based on role and reviewed regularly. Sign-ins require multi-factor authentication. Secure sharing replaces email attachments, keeping sensitive information within the vault. These measures lower risk without slowing work and form part of a wider plan for protecting assets.

.png)

.png)