Conventional Way

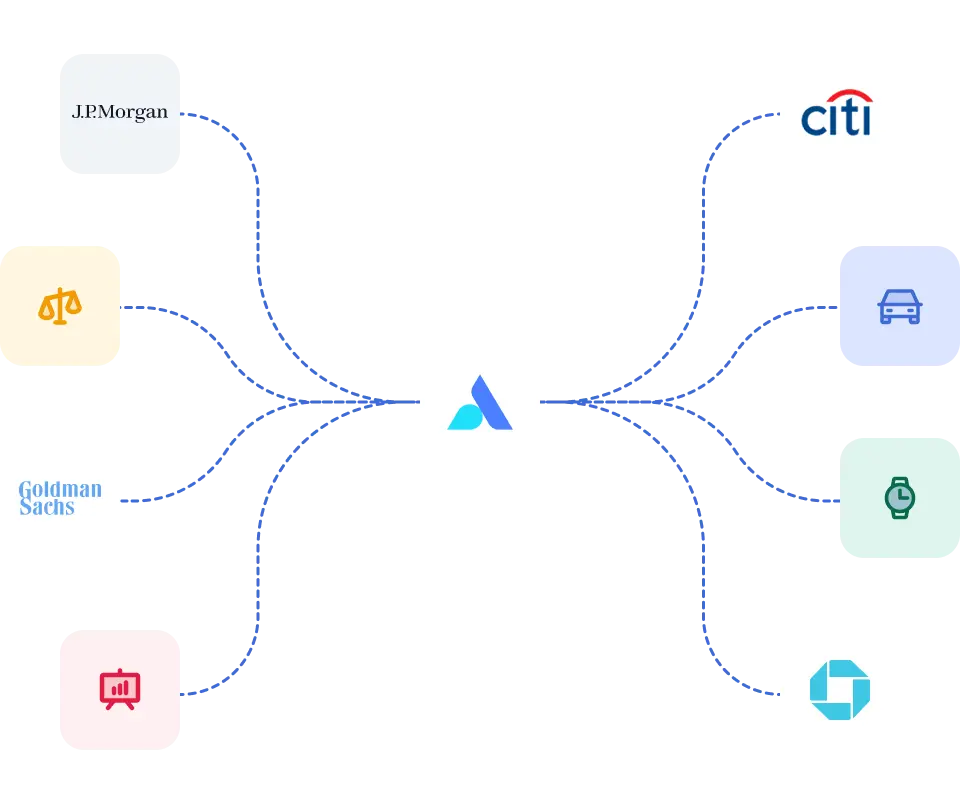

Fragmented Financial Data

Spreadsheet overload

Data spread across banks portals, PDFs and Excel files

Time consuming reporting

Slow outdated insights that make decision making harder

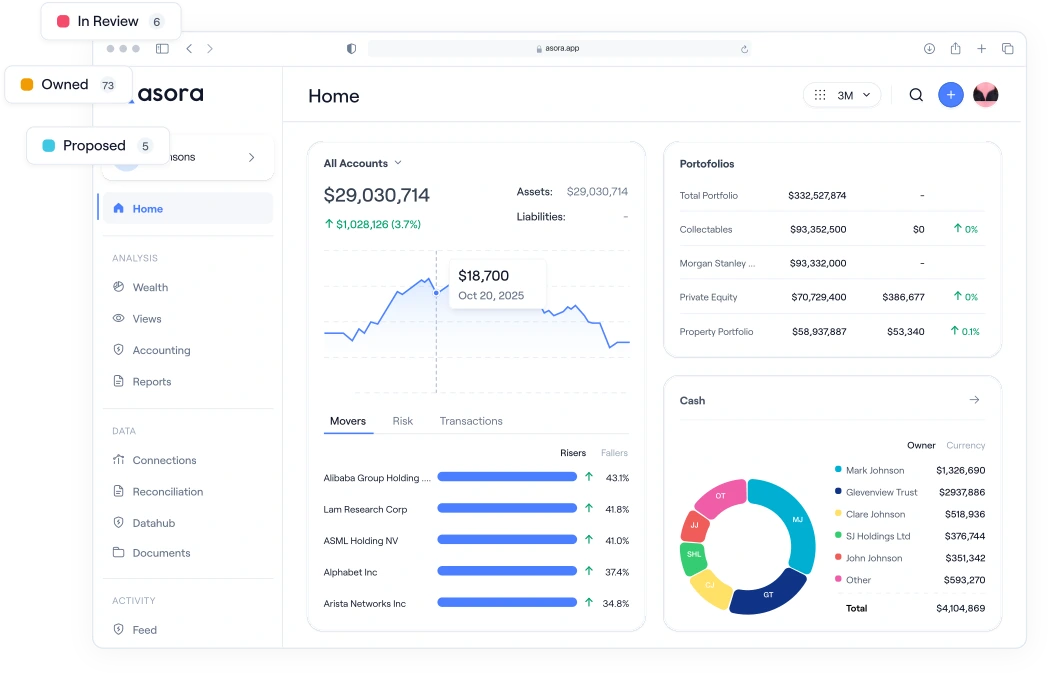

Asora Way

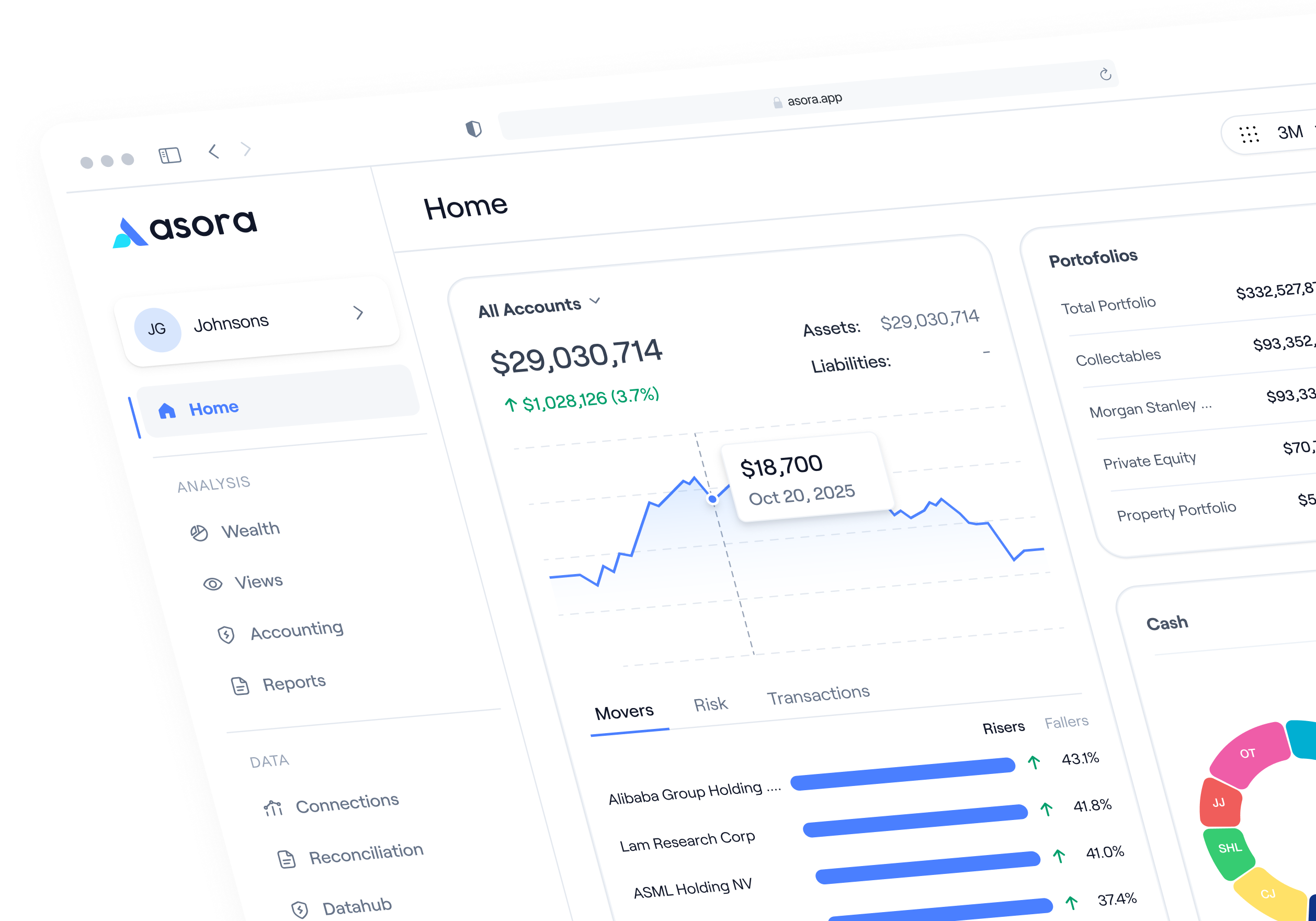

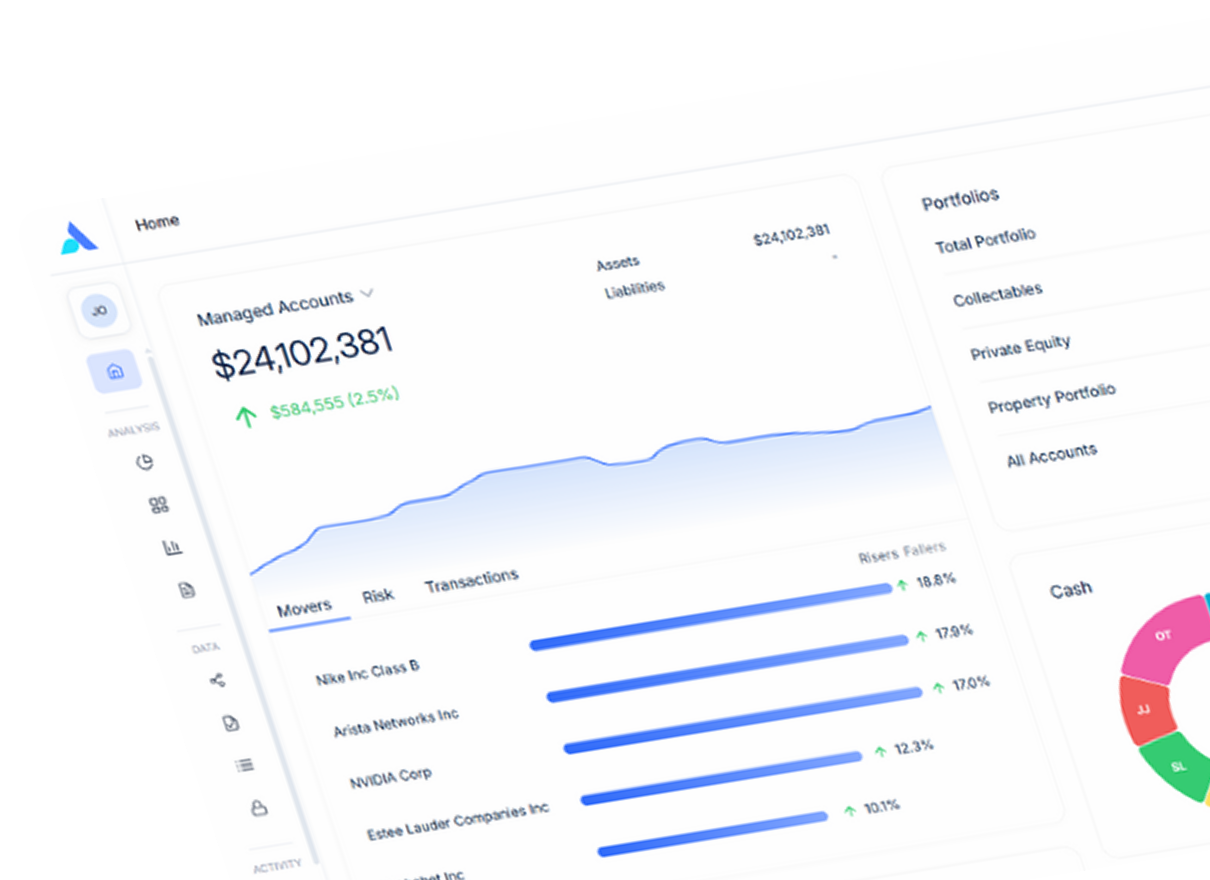

One Platform, Total Clarity

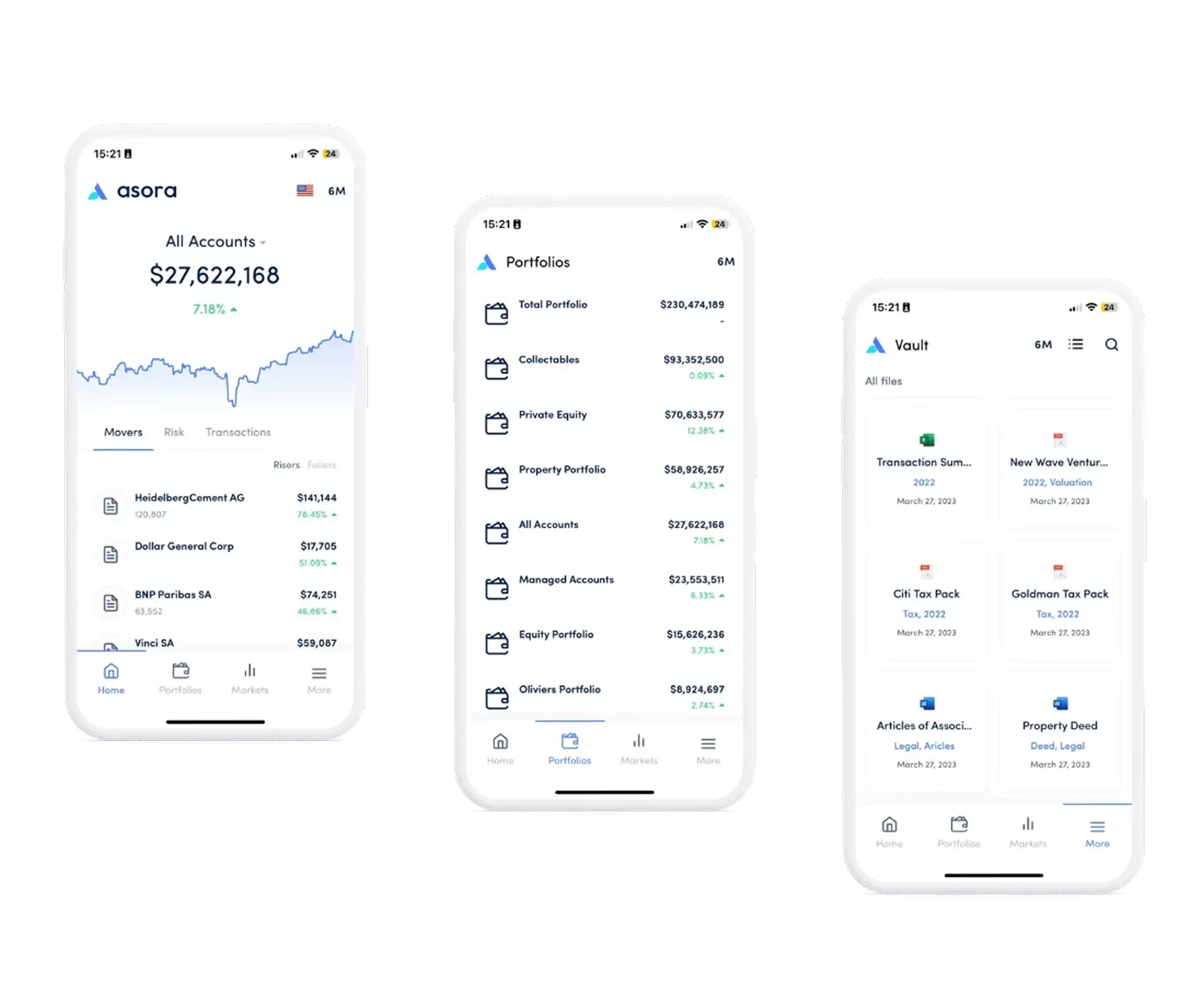

A unified operating platform

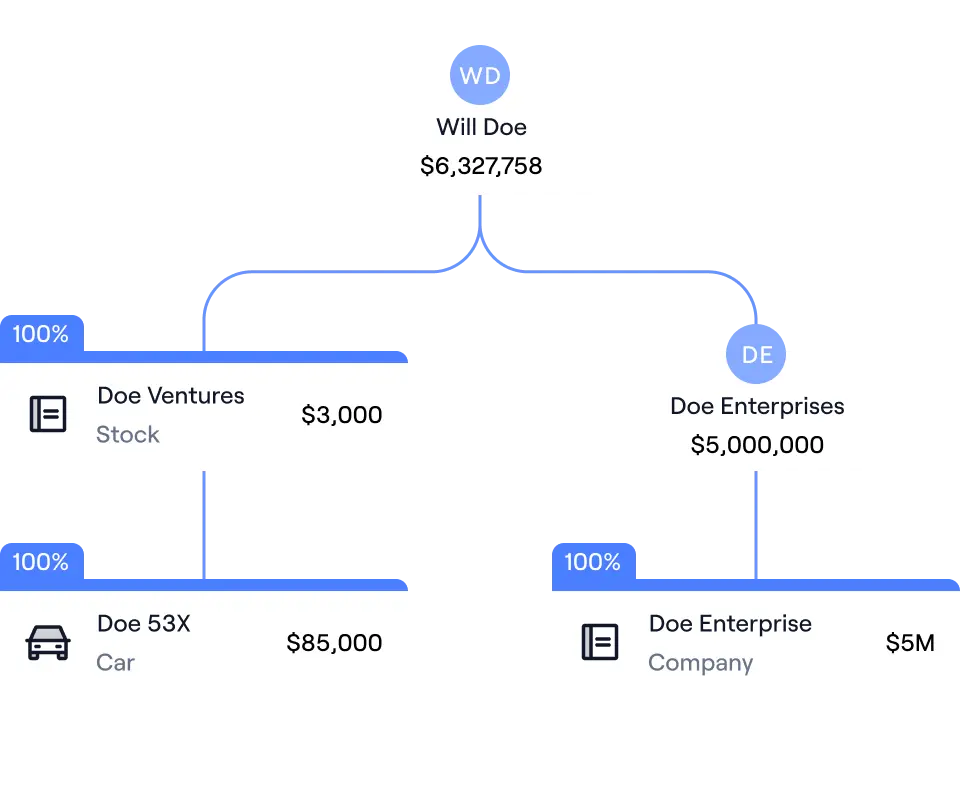

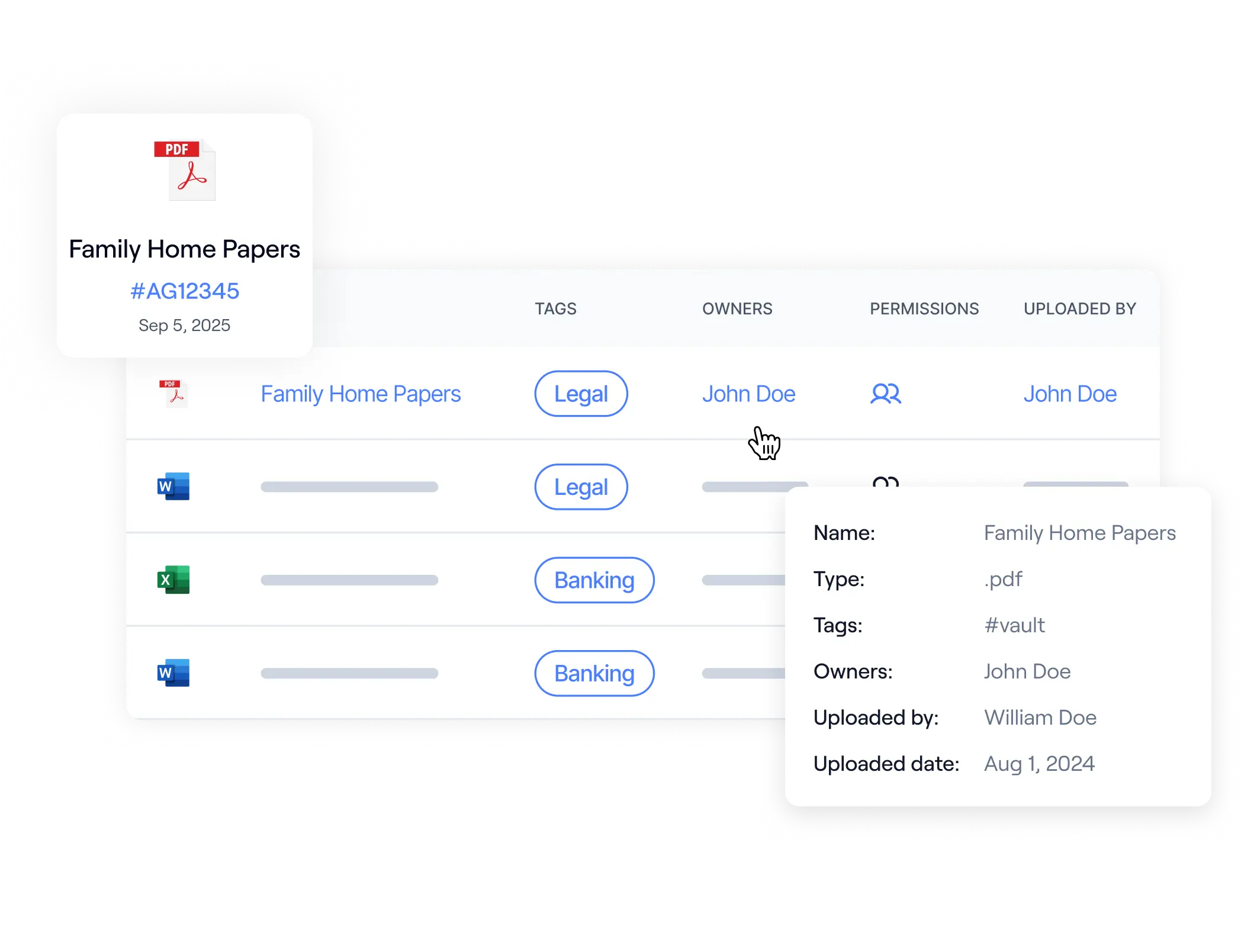

Single source of truth for all your data

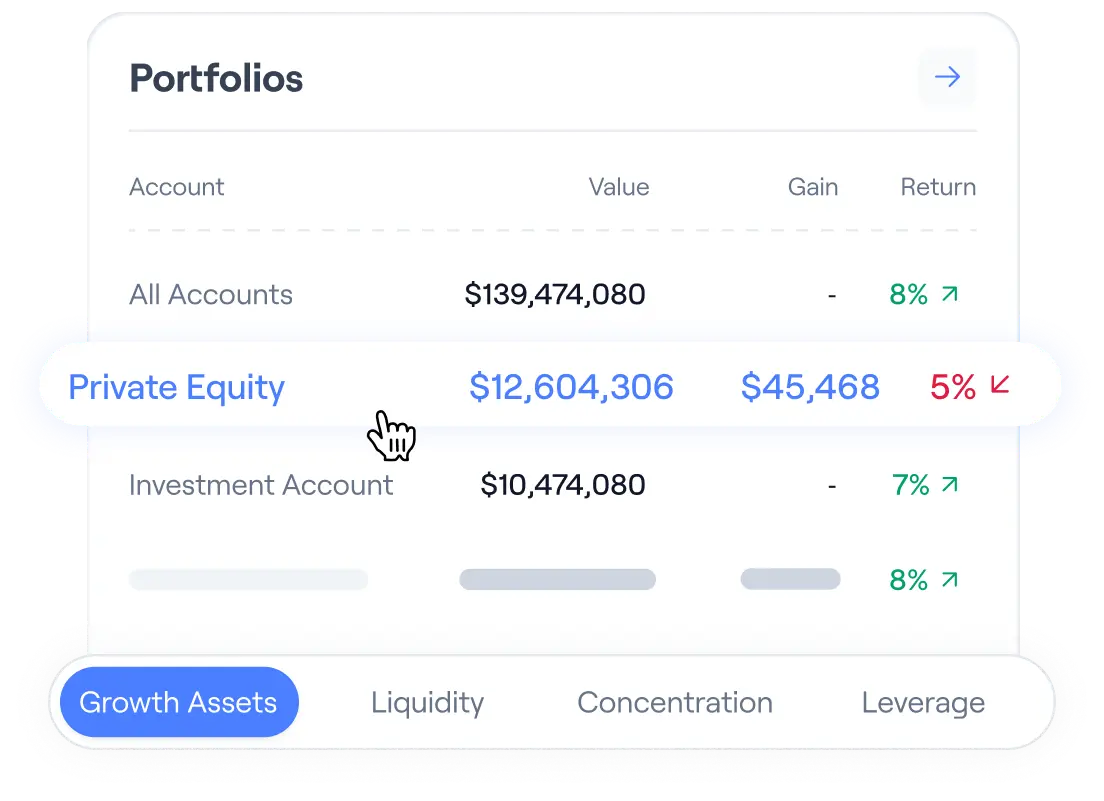

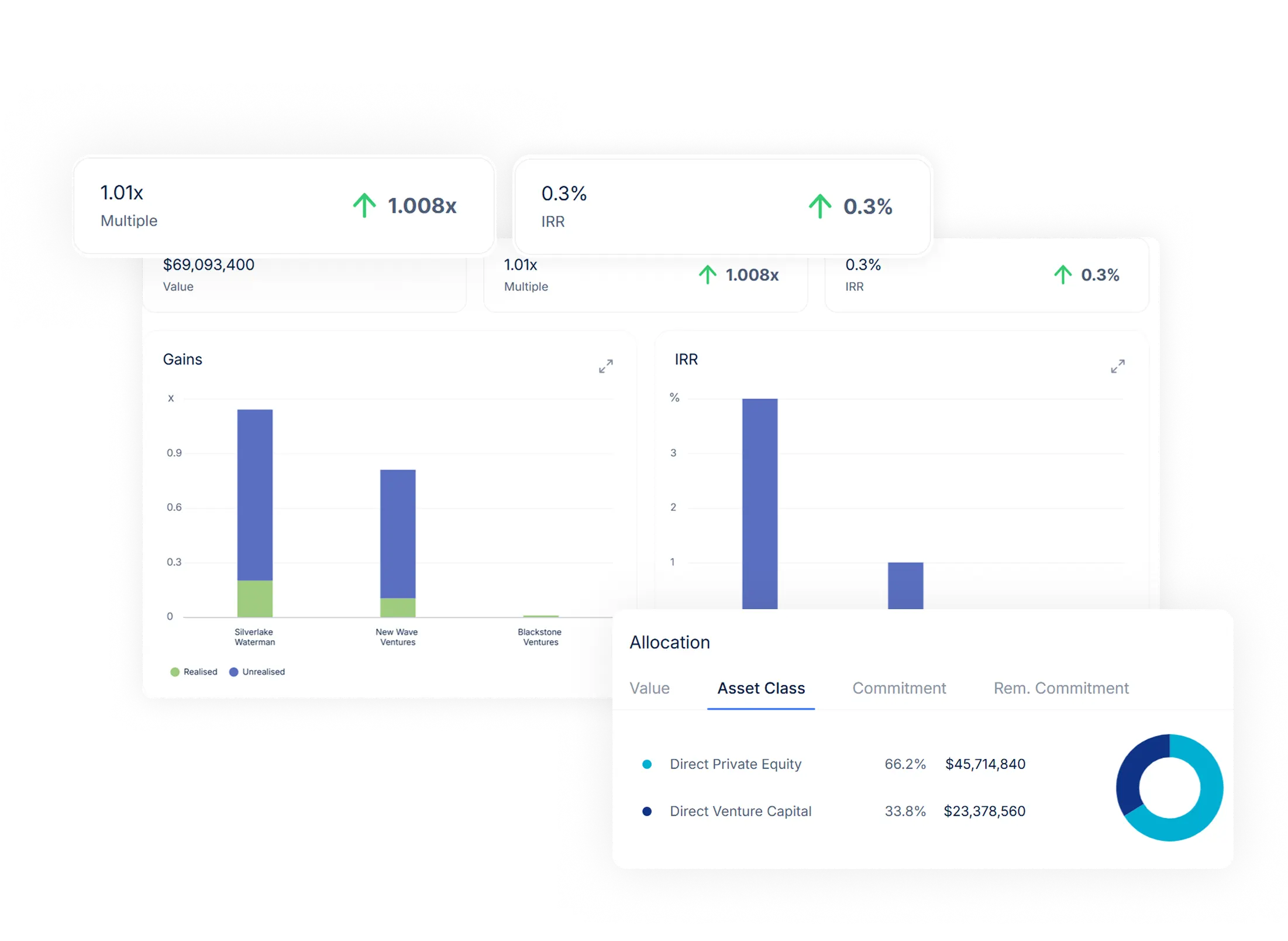

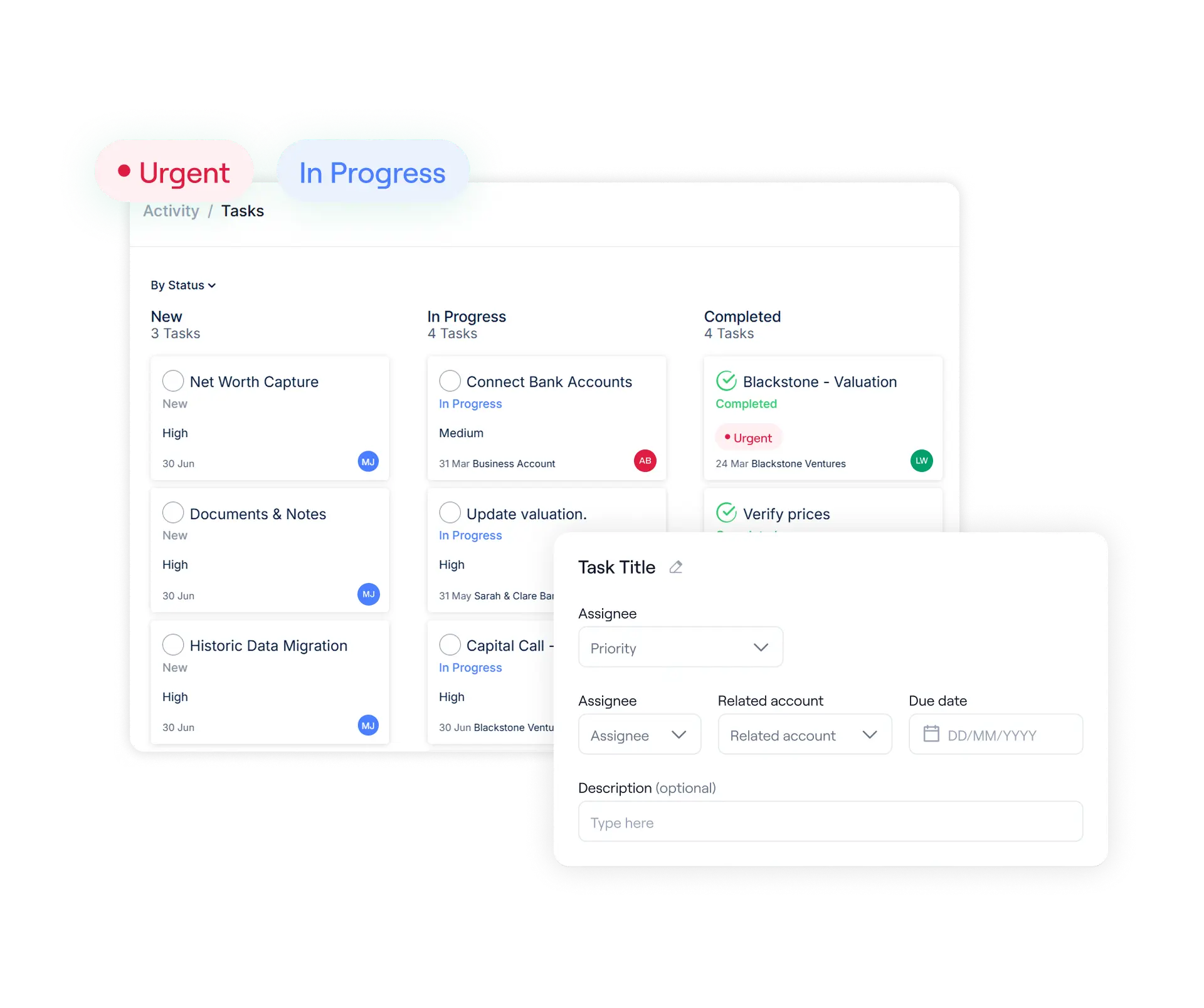

On-demand reports ready in minutes

Timely insights across your portfolio

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.png)