.png)

Author

Table of contents

"What used to take hours or days is now done in minutes"

A family office investment strategy defines how a family allocates capital across liquid and illiquid assets, manages liquidity constraints, and governs investment decisions across multiple entities and family members. The best investment strategies for family offices begin with a total-wealth baseline that aggregates bank accounts, custodians, and private markets into a single view, then layer in entity look-through, private commitment pacing, liquidity guardrails, and automated reporting.

Most family offices have an investment strategy somewhere. It might reside in a slide deck from three years ago, an email thread with an advisor, or a mental model the principal carries around but hasn't committed to writing down.

The problem isn't having ideas about asset allocation or risk tolerance. It's turning those ideas into an operating loop that handles the reality of family office investment management:

Investment strategies for family offices need to be more than strategic weights on a page. They need to be backed by data aggregation, entity look-through, and automated workflows.

This guide offers practical advice for developing a family office investment strategy that is effective in real-world applications.

.webp)

A family office investment strategy outlines how the family allocates wealth across various asset classes, manages liquidity, mitigates risk, and makes informed investing decisions across multiple generations.

For single family offices, this scope includes marketable securities (such as stocks and bonds), private markets (including private equity, venture capital, and private credit), tangible assets (such as real estate, infrastructure, and farmland), and operating businesses that the family controls.

It also includes the entity structures that hold those assets, such as trusts, SPVs, and holding companies, as well as the governance framework that determines who makes decisions, how much risk the family is willing to tolerate, and what liquidity guardrails protect against forced sales.

The outputs to aim for include:

The execution reality is that the strategy lives or dies by three things: (1) data aggregation that gives a total-wealth baseline, (2) entity look-through that prevents double-counting across structures, and (3) disciplined workflows that surface exceptions and trigger reviews before problems compound.

What follows is a practical checklist for building and implementing an investment strategy that withstands real-world conditions. Emphasis is on clean data, accurate look-through, and repeatable processes.

Family objectives should be prioritized and documented. Are you building generational wealth for future generations? Supporting philanthropic goals? Maintaining family values? Maintaining family legacy through operating businesses?

Drawdown tolerance, cash needs, tax constraints, and governance preferences require a clear definition.

Operationalize it: Capture beneficiaries and entities in your system. Attach mandate documents (investment policy statements, trust agreements, family mission statements) to the appropriate records. Configure reporting views to reflect the constraints that matter.

A credible baseline starts with a complete inventory of current holdings. Aggregate bank accounts, custodian holdings, and markets (commitments, capital calls, distributions, valuations) into one live view.

Include everything:

Operationalize it: Connect automated feeds from banks and custodians to streamline the process. Securely ingest fund documents and capital statements. Seed opening positions for private assets so valuations and cash flows update from a clean baseline.

Wealth is often held in trusts, SPVs, holding companies, and individual names. Model these structures once, then configure roll-ups to family or beneficiary views that avoid double-counting.

When Trust A owns SPV B, which owns private equity, the system should show total family wealth without adding the same asset twice at different levels.

Operationalize it: Maintain a living entity tree that updates as structures change. Build reusable roll-ups to ensure monthly reports accurately reflect the consolidated net worth across all legal structures.

Strategic weights are set for each asset class.

Include min/max bands around each weight (e.g., equities 30-40%, private equity 15-25%). Define your cash policy, FX stance, and review cadence.

Operationalize it: Monitor drift against target ranges to ensure accuracy. Surface FX exposure when it exceeds policy limits. Trigger workflows for rebalance reviews when bands are breached.

Private markets require commitment pacing. It's not possible to invest everything at once because capital is spread out over the years. Plan how much you'll commit annually, diversify across vintage years, assess manager capacity, and model cash flows to guarantee sufficient liquidity for calls.

Include a secondaries policy for when you need liquidity or want to exit underperforming positions early.

Operationalize it: Track commitments, capital calls, distributions, and capital accounts in the same system. Store LPAs, call notices, and quarterly statements as documents linked to each fund. Set workflow reminders for notice review and payment deadlines.

Illiquid assets, such as private equity and real estate, can lock up capital for a decade. Liquidity is organized in laddered buckets (immediate cash, 1-year accessible, 3-year, 5-year+). Record loan-to-value ratios for real estate and review regularly. Maintain a calendar of upcoming capital calls, fund lock-ups, and redemption gates to ensure timely awareness and compliance.

Operationalize it: Tag assets with liquidity profiles. Attach loan documents to each property. Configure a Capital Calls & Redemption Gates workflow to surface upcoming call deadlines and redemption windows, so cash is ready before the cut-off dates.

Standardize due diligence questionnaires for new managers. Track fees (management, performance, other) to measure impact on net returns. Store side letters and meeting notes linked to the entity or asset they affect.

Build an audit trail showing who reviewed what, when decisions were made, and which documents supported those decisions.

Operationalize it: Bind DDQ files, fee schedules, and side letters to manager records. Log meeting notes and tasks directly on the investment. Maintain version history and access logs for governance reviews.

Track time-weighted return (TWR, for liquid portfolios) for all investments private markets, add IRR, MOIC (multiple of invested capital), TVPI (total value to paid-in capital), and DPI (distributions to paid-in capital). Monitor fee impact, cash drag from uninvested capital, concentration risk, and FX exposure.

Use family office software to create executive packs in minutes and provide advisors with drill-down exports. Provide principals with mobile views for quick reviews.

Operationalize it: Performance monitoring draws from live data sources, including custodian feeds, logged transactions, and quarterly valuations. Reports refresh automatically. Principals review on mobile with biometric access.

Surface mismatches between custodian positions and internal records. Assign reconciliation issues to owners for resolution. Log the fix and maintain an audit trail. Define valuation policies (when to mark private assets, who approves changes, and key employees who own direct investments). Configure permissions by role so family members, trustees, and external advisors see only what they need.

Operationalize it: Accounting flags reconciliation issues automatically. Users can assign tasks to resolve reconciliation errors to the right person. Two-factor authentication and biometric access protect sensitive data.

A platform like Asora bundles aggregation, private assets, entity look-through, documents, workflows, reporting, and mobile access so your investment strategy runs as an automated operating loop.

Real estate serves multiple roles in family office investment strategies in 2026, including income generation, inflation hedge, and collateral for borrowing. Family office real estate investment strategies must account for illiquidity (sales can take months), leverage risk (including loan covenants and interest rate exposure), and ongoing expenditures.

Here are some family office real estate investment strategies:

Real estate investments require more operational oversight than liquid holdings, so document management and workflow reminders become critical for lease renewals, refinancing, and property sales.

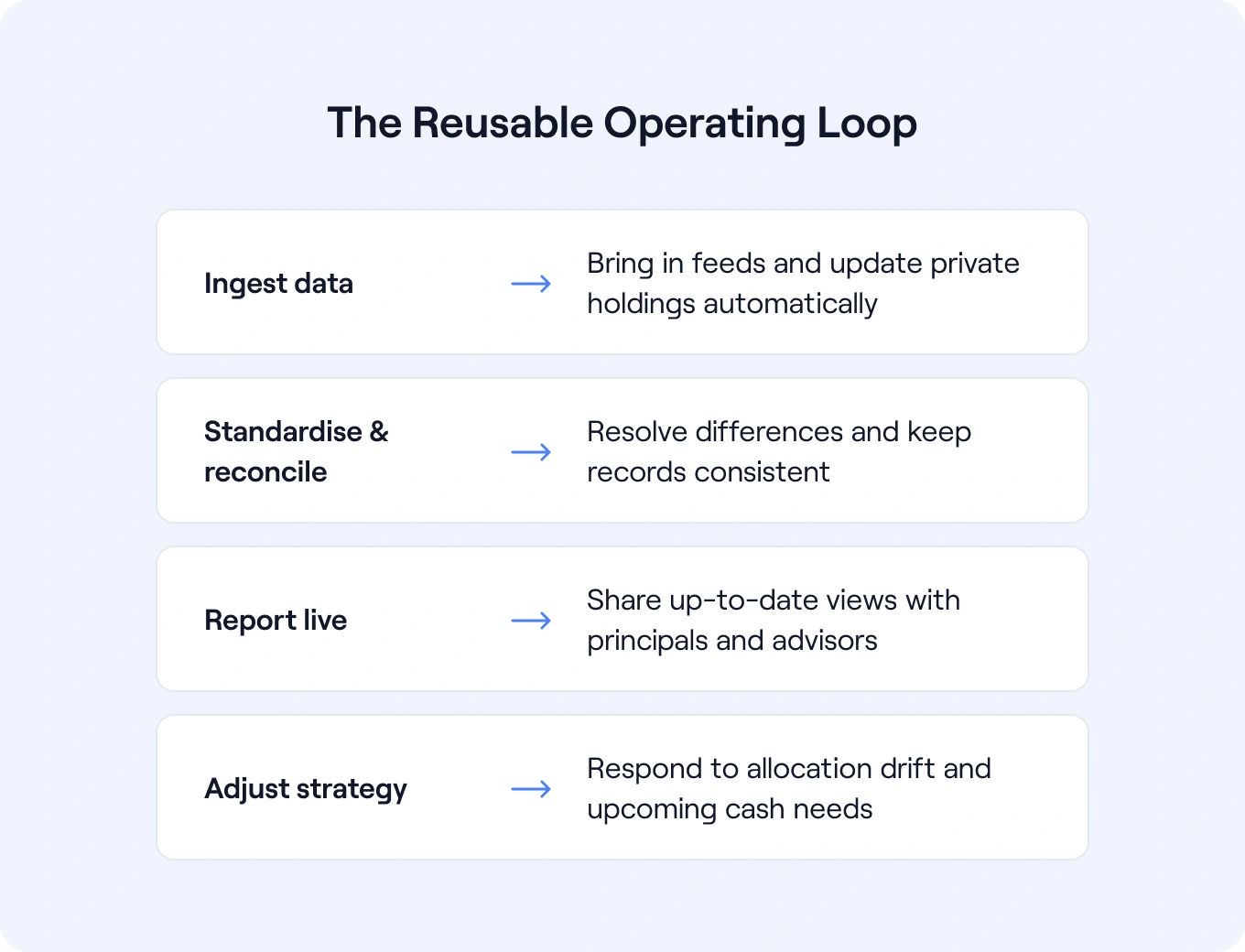

Your investment strategy should run as a repeatable process (not a one-time project). To keep this from being a one-off exercise, embed it in workflow and data. Technology can support your strategy in these ways:

This loop replaces the days-long consolidation cycle that happens when data lives in spreadsheets, emails, and shared drives.

After moving from spreadsheets to an integrated platform like Asora, several things improve immediately.

Fewer parallel spreadsheets to maintain. Documents live beside the data they support, not scattered across email. Month-end and quarter-end close runs faster because timely, standardized data is already in one place, so finance spends less time chasing figures and compiling packs. (See our Family Trust case study: reporting prep time reduced by 60%. Meeting prep becomes clearer when everyone (principals, family office staff, advisors) sees the same live record.

Governance gets an uplift, too. Every figure is traced back to a source file and a decision log. When trustees or auditors ask how you valued a private investment or why you rebalanced, the evidence is shown in seconds.

An investment strategy isn't a one-time slide deck presentation. It's an operating loop backed by one live record where data, documents, and workflows connect.

Prioritize building a total-wealth baseline, enabling entity look-through, enforcing private markets discipline through commitment pacing, maintaining liquidity guardrails, and automating reporting so you spend less time consolidating and more time making informed decisions.

The outcome is minutes, not days, of reporting, fewer manual joins across systems, cleaner audit trails, and better investment opportunities captured because you have the data to act quickly.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Start with a total-wealth baseline that aggregates all holdings, including bank accounts, custodial accounts, private markets, tangible assets, and operating businesses. Define strategic weights with minimum and maximum bands for each asset class based on investment objectives, risk appetite, and liquidity requirements. Account for private market commitments that call capital over years; model cash flows to avoid holding excessive uninvested cash.

Model commitment pacing across vintage years to diversify timing risk management. Estimate capital call schedules based on historical fund behavior (typically 3–5 years). Ladder liquidity buckets (immediate cash, 1-year accessible, longer-term) to ensure you can meet calls without forced sales. Track unfunded commitments, upcoming distribution schedules, and redemption windows for hedge funds. Maintain a capital call calendar with workflow reminders to ensure timely follow-up.

Use IRR, MOIC (plus TVPI/DPI) for private markets; use TWR for liquid/marketable portfolios. Monitor the impact of fees (wealth management fees, carried interest, transaction costs). Measure cash drag from uninvested capital awaiting deployment. Track concentration risk (single manager, sector, geography). Review FX exposure when holdings span multiple currencies.

A single platform eliminates duplicate data entry across systems. Data aggregation, entity look-through, and reconciliation happen automatically. Documents link to assets and entities, rather than email threads. Workflows trigger reminders for fund capital calls, valuations, and rebalancing reviews. Reports pull from live data (no manual consolidation). Principals access dashboards on mobile. Investment advisors export details without custom requests.

.png)

.jpg)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.webp)