.png)

TL;DR

Choosing between a single-family office vs multi-family office depends on your wealth level, control preferences, and cost considerations. Single-family offices offer complete customization and privacy for families with $100M+, while multi-family offices provide cost efficiency and shared resources for families with $25M+ through pooled services across multiple families.

You've built significant wealth, and now you're facing a decision that will shape how your family manages that wealth for generations: should you establish a single-family office or join a multi-family office?

This isn't just about picking a wealth management service—it's about choosing the foundation for your family's financial future.

The choice between multi-family office vs single-family office structures has real consequences. Get it right, and you'll have a system that grows and protects your wealth while aligning with your family's values. Get it wrong, and you could end up paying too much for services that don't fit your needs, or worse, watching your wealth erode due to poor management.

Let's cut through the industry jargon and examine what each option actually means for your family.

Your Family Office Options

Single-Family Office

A single-family office is a private organization dedicated exclusively to managing one family's wealth. Every decision, every investment, and every strategy revolves around your specific goals.

Single-family offices typically serve families with significant wealth (usually $100 million or more) because the operational costs can add up. You're essentially building your own wealth management company, complete with investment managers, tax specialists, estate planners, and administrative staff.

Modern single-family offices manage more than just investments. They handle everything from tax planning and estate management to family governance, philanthropic planning, and even concierge services. Some coordinate charitable giving, manage business interests, and prepare the next generations for stewardship.

Multi-Family Office

A multi-family office serves multiple families—typically 10 to 50—offering comprehensive wealth management while sharing costs. This makes sophisticated wealth management accessible to families who might not have the resources to justify their own dedicated team.

Families benefit from shared resources and expertise, but multi-family offices must balance needs across clients. They usually standardize processes and investment strategies to work well for most, though customization is limited compared to single-family offices.

Single-Family Office vs. Multi-Family Office

Control and Customization

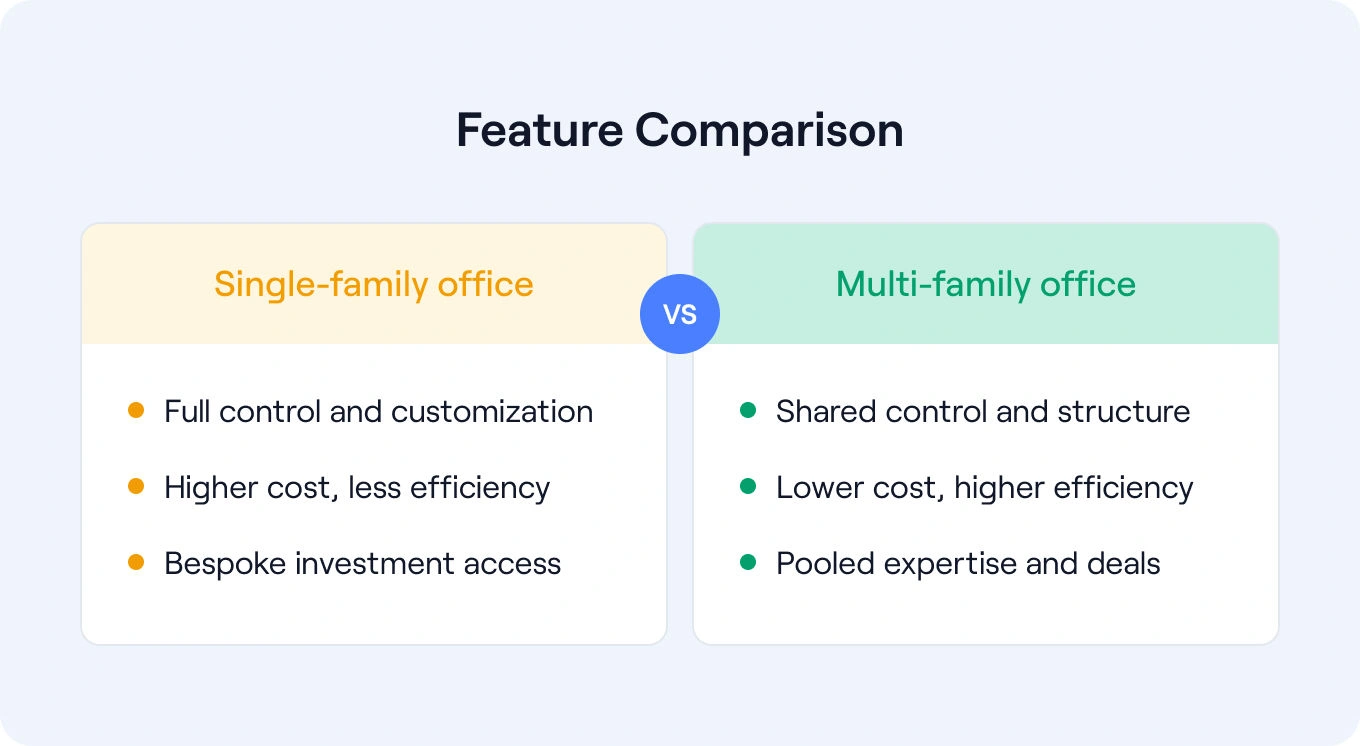

Single-family offices give you complete control over every decision—from investments to governance—allowing fully bespoke structures and policies. Multi-family offices offer less control but more professional management, ideal for families preferring delegation without losing oversight.

Cost Considerations and Efficiency

The cost difference is significant. Single-family offices typically require $100–250M in assets to justify operational expenses, which can reach 1–2% annually. Multi-family offices spread costs across families, making them suitable for $25–100M ranges. While more affordable, premium multi-family offices can still command high fees.

Access to Investment Opportunities and Expertise

Single-family offices can pursue bespoke opportunities that match the family's goals and risk management strategy. Multi-family offices offer pooled access to institutional-quality deals but must balance interests across families, sometimes limiting specialization.

How to Choose the Right Family-Office Structure

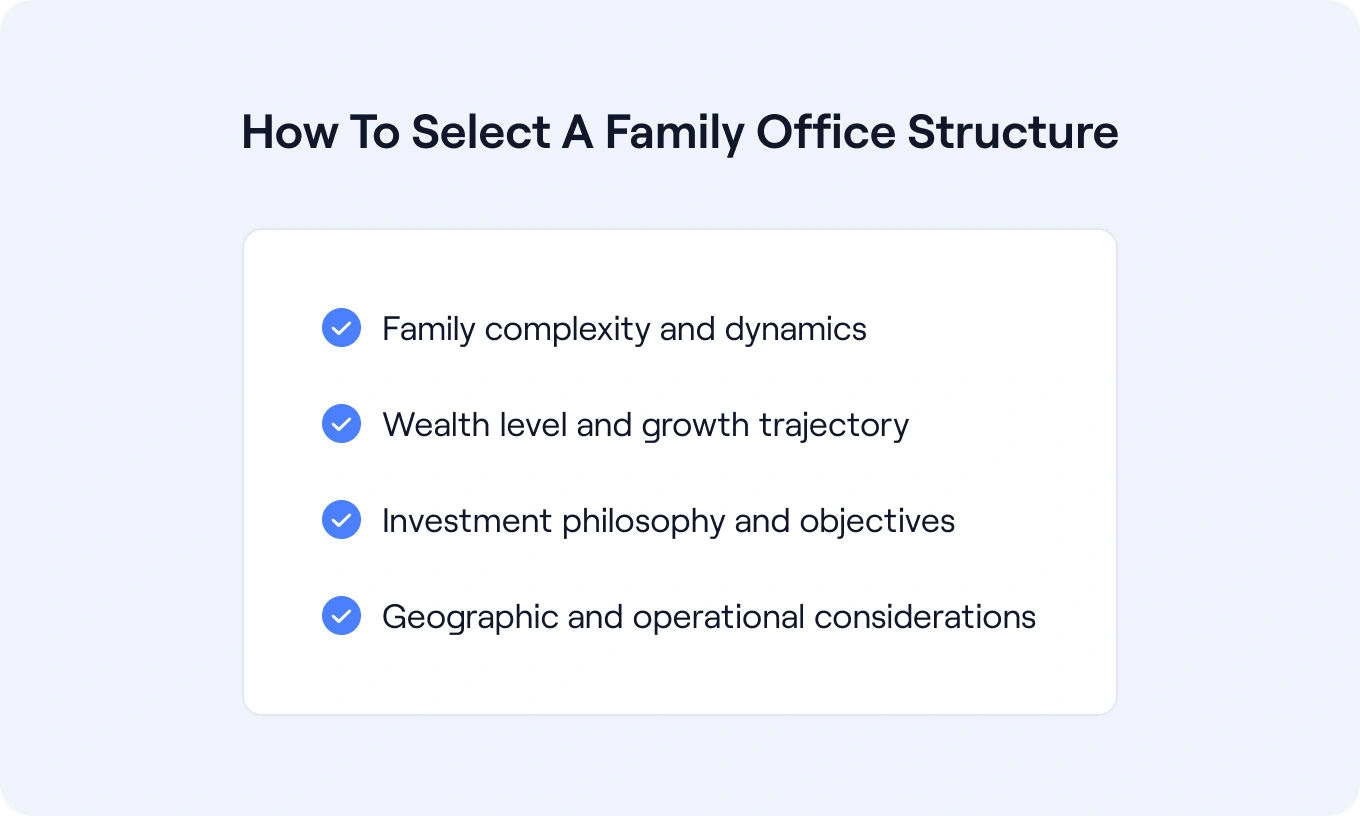

Family Complexity and Dynamics

Large, multi-generational families or those with complex business interests often benefit from single-family offices. Smaller families or those preferring professional management without direct oversight often choose multi-family offices.

Wealth Level and Growth Trajectory

Families with $25–100M often start with multi-family offices and transition later as wealth grows. Families with $100M+ can decide based on control and preference rather than cost efficiency.

Investment Philosophy and Objectives

Families with unique ESG priorities, risk profiles, or bespoke investment needs often prefer single-family offices. Multi-family offices suit those who prefer delegated professional management within broad investment parameters.

Geographic and Operational Considerations

Single-family offices can operate from any preferred location. Multi-family offices often have fixed structures, so families align to their operational model. Consider how you want to engage—virtually, locally, or globally—before deciding.

Common Mistakes to Avoid When Choosing Your Office Structure

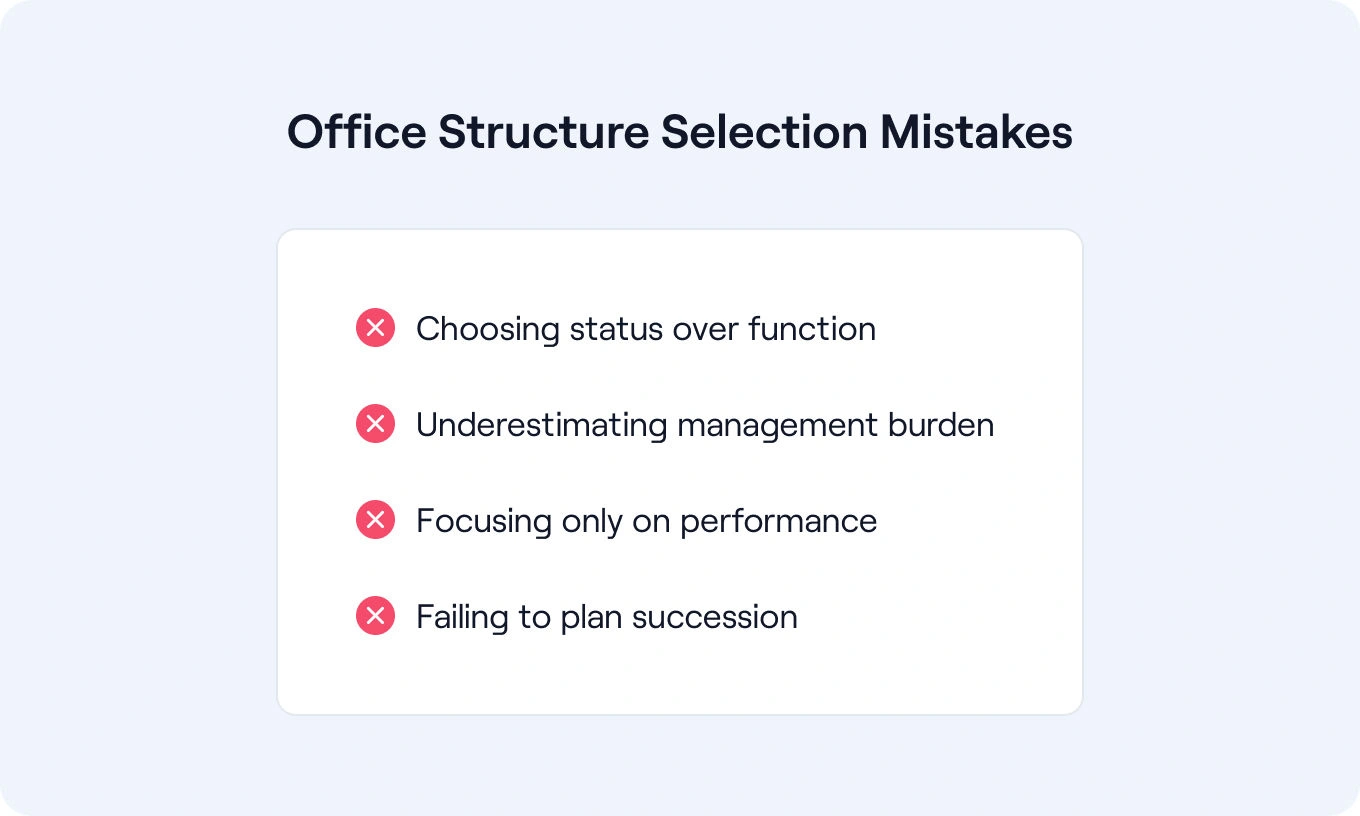

- Choosing Based on Status Rather Than Function: Don’t pick a single-family office for prestige or a multi-family office for cost. Choose based on alignment with your family’s goals.

- Underestimating the Management Burden: Single-family offices require governance and oversight—expect active involvement in management and decision-making.

- Focusing Only on Investment Performance: Governance, reporting, and family education matter as much as investment returns.

- Failing to Plan for Succession: Think long-term—will future generations prefer autonomy or professional management? Plan governance accordingly.

Your Next Steps

Choosing between a single-family office and multi-family office takes reflection. Define your family’s goals, evaluate both structures carefully, and talk to providers before deciding. The right structure provides confidence, continuity, and clarity—not just performance.

Your decision doesn’t have to be permanent; as your wealth and needs evolve, you can transition. The best setup is one that grows with your family and preserves both wealth and values.

FAQ

Can I switch from a multi-family office to a single-family office later?

Yes. Many families start with a multi-family office and transition later as wealth and complexity grow. It’s a natural progression for scaling control and internal management.

How do single-family and multi-family offices compare on investment performance?

Performance depends on team quality, not structure. Single-family offices can target niche or direct deals, while multi-family offices leverage pooled access to institutional opportunities. Both can perform well with the right governance and strategy.

What level of control do I maintain in a multi-family office vs single-family office?

Single-family offices offer total control over decisions and hiring. Multi-family offices provide limited operational control but full oversight through structured governance and reporting.

How do costs typically compare between single-family office vs multi-family office structures?

Single-family offices often cost 1–2% of assets annually. Multi-family offices charge similar rates but share infrastructure, giving families access to broader services at lower total cost.

.png)

.png)