.jpg)

TL;DR

A hedge fund tracker helps family offices monitor hedge fund investments and holdings using manager statements, capital cash flows, and standardized reporting. It supports net performance calculation, liquidity planning, exposure monitoring, and document control without replacing accounting. This guide explains allocator-grade hedge fund tracking and outlines tools used by elite investors evaluating hedge fund trackers.

What a hedge fund tracker does for family offices

A hedge fund tracker helps family offices track hedge fund investments accurately across entities, strategies, and reporting periods. It sits between raw manager statements and consolidated reporting, providing a structured way to monitor hedge fund performance, liquidity terms, exposure, and capital activity without replacing core accounting or custodian systems. The global hedge fund industry now manages approximately $5 trillion in assets (HFR), underscoring the scale and influence of these strategies across public markets and alternative investments.

Many investors first encounter hedge fund activity trackers built on public disclosures such as Securities and Exchange Commission (SEC) filings or major shareholding notifications and transparency filings submitted to regulators across Europe. These sources can surface hedge fund news, fund name changes, and high-level hedge fund holdings in listed stocks, but they are delayed, partial, and not designed to calculate net hedge fund performance or reflect actual hedge fund trades at the portfolio level.

Allocator-grade hedge fund tracking relies instead on fund administrator NAV and capital account statements (distributed via the manager or administrator), alongside subscription, redemption, and cash movement records. Each fund reports on its own schedule and applies its own valuation policies. Funds may use leverage, which affects risk and exposure, as well as investor-specific liquidity and economic terms such as gates, lock-ups, or side-letters, that influence redemption planning and net outcomes.

Essentially, these trackers act as hedge fund performance trackers, standardizing returns, capital activity, and valuations across managers while supporting quarterly performance review, exposure and concentration analysis, liquidity planning, fee tracking, and ongoing operational due diligence.

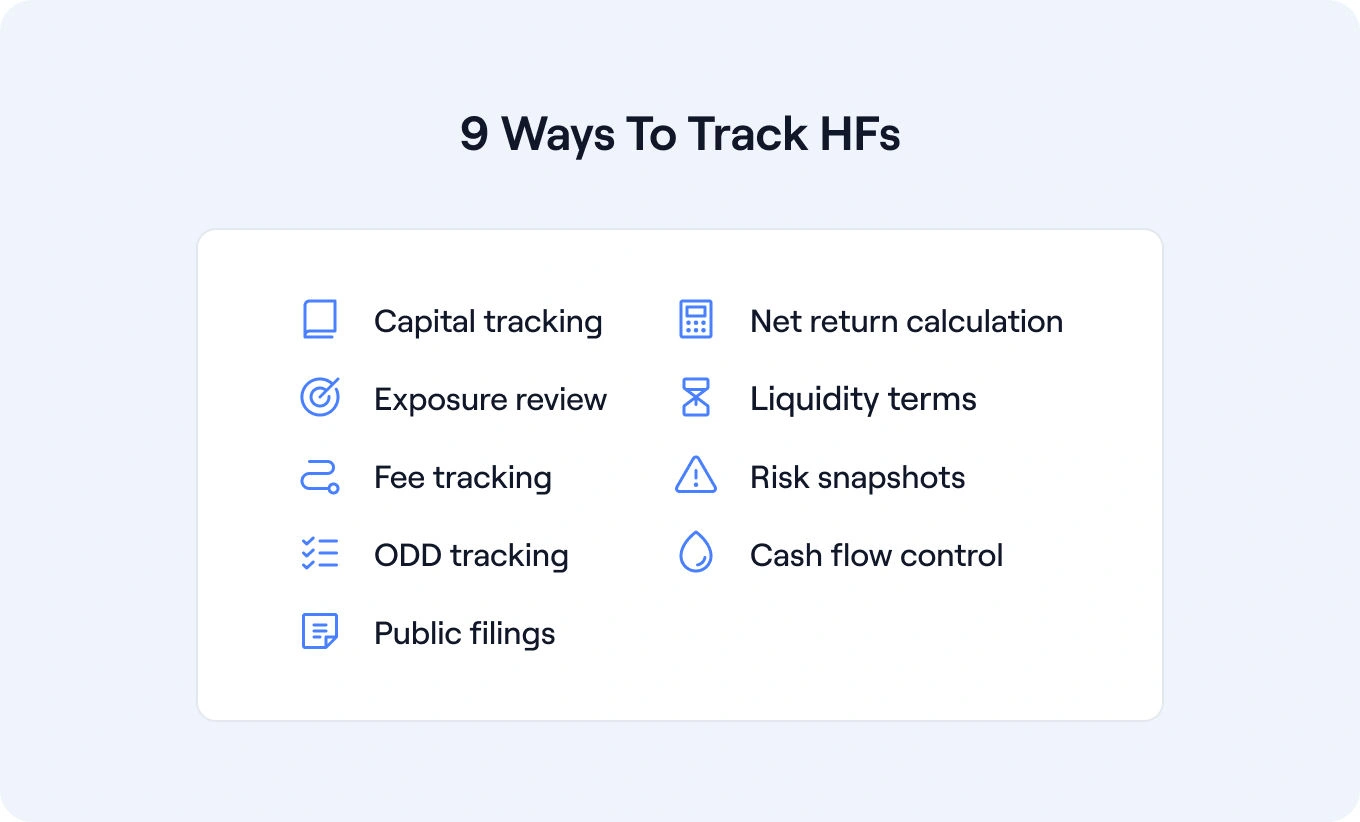

9 ways to monitor hedge fund performance

A hedge fund tracker is most useful when it mirrors how allocators actually review managers across a quarter. For family offices evaluating how to track hedge fund investments, the challenge is not access to data, but consistency, interpretation, and control.

This section outlines the core checks family offices use to assess performance, risk, and operational readiness before results roll up into consolidated reporting.

1. Capital account tracking

Capital account tracking is the foundation of any hedge fund portfolio tracker, as each fund reports performance and activity differently. Keeping the original manager statements intact ensures calculations can be traced back to the source data.

In practice, this means storing statements by fund, entity, and share class, then recording subscriptions, redemptions/withdrawals, transfers, equalisation (if applicable), and any special allocations or side-pocket movements. Linking this activity to the correct ownership structures produces a clear, auditable view of ownership interests by entity and share-class, and supports accurate quarter-end capital account roll-forwards.

2. Net performance calculation

Once capital activity is organized, the next step is calculating performance on a consistent basis.

Use manager-provided periodic net returns (typically monthly) and apply geometric linking to compare managers across funds and strategies. This supports consistent manager-to-manager analysis using time-weighted returns (TWR).

Use internal rate of return (IRR or XIRR) selectively where cash-flow timing materially affects results, such as at the total hedge fund portfolio level. IRR reflects the investor experience by incorporating subscription and redemption timing. Document the methodology and assumptions used so results remain consistent and defensible across reporting periods.

3. Exposure and concentration

Performance alone rarely tells the full story. Allocators also need to understand where risk is building. While no hedge fund position tracker offers real-time position-level transparency, allocator-grade tools standardize whatever exposure/risk reporting managers provide.

Track reported sector, geography, strategy, and underlying themes where managers disclose them. This helps teams understand how hedge fund holdings are distributed across strategies and stocks, and whether exposure is concentrated in certain sectors or market environments. Monitoring internal concentration thresholds allows allocators to spot crowding risk or positioning changes that may prompt questions, reallocation decisions, or redemption planning over time.

4. Liquidity and gates

Liquidity terms often drive portfolio decisions as much as performance. Register notice periods, lockups, gates, side pockets, and redemption windows at the fund level. Flag upcoming dates so teams can plan rebalancing, redemptions, or liquidity needs well before deadlines approach.

5. Fee terms and side letters

Fee mechanics can materially affect net results and year-end calculations. Record management fees, performance fees, hurdle rates, high-water marks, and crystallisation logic. Link side letters and amendments so analysts can quickly verify bespoke terms during reviews or audits.

6. Risk snapshots

When data history is available, a hedge fund tracker can provide high-level risk context. Track drawdown, rolling volatility, and simple return dispersion using net performance data. Link supporting manager reports (administrator statements, monthly letters, risk/exposure reports) and, where relevant, any external regulatory disclosures (eg, 13F at the manager level).

7. Operational due diligence

Ongoing diligence is an operational task, not a one-time exercise. Store Due Diligence Questionnaire (DDQs), audited financial statements, administrator confirmations, and available control reports. cadence (often annual) and event-driven refreshes (eg. service provider changes, key person events, control issues), with quarterly checkpoints where your governance process requires it.

8. Cash flow and year‑end readiness

As the year progresses, reporting and tax preparation become increasingly intertwined. Link K-1s (US) or local equivalents (eg UK tax packs, PFIC statements where applicable) to the relevant funds and entities. Support quarter-end performance, exposure, and cash-flow reporting without disrupting existing accounting or custodian workflows.

9. Public filings overlay

Public data can add context, but it should not drive allocator reporting.

Use US Form 13F disclosures to understand reported long-only US equity holdings, and similar regulatory filings in other jurisdictions such as major shareholding notifications under the EU Transparency Directive (implemented by national regulators including the UK’s Financial Conduct Authority and France’s Autorité des Marchés Financiers). These disclosures can highlight reported holdings in listed equities and indicate positioning changes over time.

However, such filings are delayed, partial by design, and typically limited to specific asset classes or thresholds. Allocator-grade tracking relies on administrator NAV and capital account statements, along with capital cash-flow records, to support performance measurement and portfolio oversight.

Vendor shortlist to evaluate

The tools below are commonly used by family offices building hedge fund portfolio trackers. Use them as references and confirm the scope against your requirements.

1. Asora

Asora is a wealth platform designed for UHNWI and lean single family offices that need allocator-grade visibility across hedge funds and other alternative assets, without enterprise overhead. It is positioned as the layer between manager reporting and consolidated family office reporting.

Features:

-

Data Aggregation: Supports aggregation of bank and investment data with timely updates, alongside manually entered hedge fund data.

-

Performance Monitoring: Calculates time-weighted returns (TWR) and internal rates of return (IRR) using manager-reported valuations and capital cash flows.

-

Private Assets: Registers hedge funds, private equity, real estate, and other alternatives at the entity level, with capital activity tracking.

-

Documents: Stores and links manager statements, side letters, DDQs, audited financials, and tax documents directly to accounts and entities.

-

Workflow support: Enables teams to create and assign tasks related to reporting, liquidity reviews, and due diligence. Deal pipeline views can be used to track diligence stages and manage follow-ups across investments. Approvals and reconciliations remain within external processes.

Asora is used by UHNWIs and lean single family offices managing 5–50 entities across public and private markets. It is typically adopted by teams that need clearer visibility across hedge funds and other alternatives and are moving away from Excel-based tracking toward a more structured reporting process.

Pricing is tier-based, starting at $900 per month for portfolios under $30M. All features are available across all tiers, with pricing scaled based on assets under management, along with optional add-ons.

Teams evaluating fit can request a demo to review workflows and reporting in context.

2. Black Diamond (SS&C)

.webp)

Black Diamond Wealth Platform is a modular, cloud-based wealth and reporting suite from SS&C, serving RIAs, family offices, and trust companies. It combines portfolio management and consolidated reporting with trading & rebalancing, CRM, compliance, and billing for a comprehensive workflow view.

Pricing for Black Diamond is quote-based and provided on request.

Features:

- Consolidated portfolio and performance reporting

- Trading & rebalancing integration

- CRM with unified workflows, contact management, and account tracking

- Billing, invoicing, and compliance modules

- Strong third-party integration ecosystem

Black Diamond is often used by teams seeking unified wealth reporting, operational workflows, and advisor-facing interfaces.

3. Masttro

Masttro is a family-office-focused wealth platform designed to consolidate complex, multi-entity balance sheets across public and private assets. It supports data aggregation, performance reporting, and wealth mapping for families operating across jurisdictions and custodians.

The platform is commonly used by multi-entity family offices seeking consolidated reporting and structured oversight of global wealth.

Masttro operates on a flat-fee subscription pricing model. Pricing is custom and provided on request, typically reflecting the number of entities, users, integrations, and configuration required. Vendor-stated materials indicate that fees are not tied to assets under management, meaning costs do not increase as AUM grows.

Features:

- Multi-entity, multi-jurisdiction wealth and investment data aggregation

- Interactive dashboards and performance reporting

- Direct custodian connections and AI-assisted document processing

- Secure encrypted data vaults with Swiss-based infrastructure

- Ownership/entity mapping

Masttro supports single family offices, multi-family offices, wealth advisors, financial institutions, and professional services firms seeking consolidated wealth visibility and structured reporting.

4. QPLIX

QPLIX is a consolidated portfolio-tracking and reporting platform that streamlines investment aggregation for complex portfolios. It focuses on multi-asset reporting and performance analytics, though detailed pricing is quote-based and typically configured by use case.

Contact the vendor for pricing.

Features:

- Data aggregation across public and private assets

- Performance dashboards, automated report creation, and distribution

- Trading and Rebalancing solutions

- Client portal and mobile app access for reporting and portfolio visibility

QPLIX supports (multi) family offices, independent wealth managers, banks and financial institutions, treasury departments, and foundations seeking consolidated reporting and multi-asset oversight across complex structures.

5. FundCount

FundCount is an integrated portfolio and partnership accounting platform that combines general ledger, investment reporting, and performance analysis in one system.

Pricing available on the vendor website, depending on whether the platform is configured for HNW individuals, single family offices, multi-family offices, or hedge fund operations.

Features:

- Partnership accounting and general ledger

- Multi-currency and multi-entity support

- Built-in performance tracking and customizable reports

- AI Document Intelligence

- Automated data aggregation from custodians, banks, and investment managers

FundCount is an option for teams that need deep accounting integration and reconciled performance tied to the books of record.

6. SEI Novus

.webp)

SEI Novus is a portfolio intelligence and analytics platform used by institutional investors, allocators, and investment teams. It delivers deep analytics, risk decomposition, and exposure visualization across multi-asset portfolios.

Pricing is not publicly available; contact the vendor for details.

Features:

- Attribution and risk analytics

- Exposure mapping and factor analysis

- Aggregation of manager data with validation and enrichment

- Collaboration tools for investment teams

- Institutional-grade reporting and insight layers

Novus is often considered by institutional investors and allocators who prioritize advanced analytics and transparency across manager data.

Reporting to standardize for quarter-end

Standardizing a core set of hedge fund reports helps family offices move from ad hoc reviews to a repeatable quarter-end process and ensures hedge fund data can be rolled up cleanly into consolidated family office reporting.

Quarter-end is where a hedge fund tracker proves its value. Family offices need to move from varied manager statements and cash-flow schedules to a consistent reporting view that supports allocator review and consolidated reporting.

Standardizing hedge fund reports creates a shared reference point across funds, strategies, and entities, reducing manual interpretation and making performance, risk, and liquidity easier to assess each quarter.

Capital account roll-forward report: provides a fund-by-fund and entity-level view of opening capital, subscriptions, capital calls, distributions, fees, net performance, and ending capital for the quarter. This report acts as the audit-friendly bridge between periods and is often relied on to validate performance calculations and reconcile reported values back to manager statements.

Net performance vs policy benchmark report: shows net hedge fund returns alongside internal policy benchmarks or reference indices. Using time-weighted return allows allocators to compare managers consistently across strategies and vintages, while highlighting periods of underperformance or divergence that may require follow-up or deeper analysis.

Exposure and concentration report: aggregates reported exposures by strategy, sector, geography, or manager where disclosures are available. Exposure and concentration views help investors identify crowding risk, thematic overlap, or outsized positions in certain stocks that could affect portfolio behaviour during periods of market stress.

For value investors and other long-term allocators, this context supports informed decisions about position sizing, rebalancing, or when to sell exposure as strategies evolve.

Liquidity calendar report: consolidates notice periods, lockups, gates, and redemption windows across all hedge fund investments into a forward-looking view. This report supports liquidity planning and helps teams avoid missed notice deadlines or unexpected constraints on capital availability.

Fee terms and hurdle summary report: summarizes management fees, performance fees, hurdle rates, high-water marks, and crystallisation schedules by fund. Having these terms clearly documented supports validation of net returns and simplifies quarter-end reviews, audits, and year-end planning.

Operational due diligence tracker report: tracks the status and currency of DDQs, audited financial statements, administrator confirmations, and other diligence materials. Review dates and refresh cycles are typically shown by quarter, giving teams a clear view of what has been reviewed, what is outstanding, and what requires follow-up.

Standardized quarter-end reports do not replace accounting or books of record. Instead, they support consistent allocator review and provide clean inputs for consolidated reporting across the broader portfolio.

These reports are used by principals to review hedge fund performance and liquidity at a portfolio level, by investment teams to compare managers and flag follow-up questions, and by operations teams to prepare consolidated reporting and year-end processes. This allows investment teams to research manager behaviour over time and analyze performance and exposure in a consistent framework. Having a shared, standardized reporting set reduces rework, shortens review cycles, and ensures each team is working from the same underlying data.

This shared foundation also simplifies implementation. Once reporting definitions and inputs are agreed upon, teams can focus on loading historical data, mapping entities, and configuring reports rather than debating formats each quarter.

Implementation in weeks

Once reporting users and outputs are clearly defined, implementation becomes a structured data exercise rather than an open-ended configuration project. Principals, investment teams, and operations staff already share a common reporting reference, reducing iteration and shortening time-to-value.

Implementation can range from ~30–90+ days (and longer for complex, multi-entity history), depending on data quality, manager count, and how much historical activity you load. The goal is not to automate hedge fund reporting, but to establish a consistent structure that supports repeatable quarter-end review.

Week 1: Define the scope and map entities.

Confirm which entities, funds, and share classes will be included in reporting. Gather recent hedge fund statements, capital account histories, side letters, and liquidity terms. Align on reporting definitions, including benchmarks, performance methodologies, and exposure categories. This step ensures hedge fund holdings, capital flows, and performance data are structured consistently before any reporting or review begins.

Weeks 2–3: Load historical data and link documentation.

Enter 12–36 months of capital activity and net valuations to establish reporting history. Link manager statements, DDQs, audited financials, and tax documents to the correct funds and entities. This step creates the reference layer used by investment and operations teams during reviews.

Weeks 4–6: Build and validate standard reports.

Configure standard quarter-end reports, including capital account roll-forwards, net performance, exposure views, and liquidity calendars. Review outputs with principals and investment teams to confirm they support decision-making and portfolio review. Export a sample reporting set to validate formatting and completeness.

Handover and ongoing process

Confirm that approvals, reconciliations, and official books and records continue within existing accounting and custodian workflows. From this point, each quarter focuses on updating inputs and reviewing outputs rather than rebuilding reports from scratch.

Why reliable hedge fund tracking software matters

Many websites track hedge fund activity, but not all of them pull data correctly or update it consistently. Most rely heavily on public disclosures, which are delayed, partial, and easy to misinterpret without context.

Hedge fund tracking tools typically aggregate regulatory filings from sources such as the SEC’s EDGAR database, including Form 13F disclosures. While these filings are valuable for understanding reported US stock holdings, they do not reflect full portfolios, derivatives, or real-time positioning. In Europe/UK, major shareholding notifications under the Transparency Directive (and national implementations such as the UK DTR regime) can provide partial visibility into significant positions, but they do not disclose full portfolios. These disclosures provide visibility, but also exclude full portfolio composition. Reliable sourcing and contextual interpretation are therefore critical for ensuring data accuracy in hedge fund tracking.

Some allocator platforms integrate hedge fund tracking into broader multi-asset portfolio reporting; others are hedge-fund/manager analytics tools that require integration for full balance-sheet coverage. This allows family offices to understand hedge fund positions in context rather than as isolated data points.

Some of the most competitive hedge fund tracking platforms go beyond surface-level reporting and help investors understand why hedge funds make certain trades by analyzing historical data, capital flows, and strategy context. This supports informed oversight, rather than reactive decision-making.

Importantly, no software can guarantee insight or accuracy on its own. Effective hedge fund tracking depends on disciplined processes, verified data, and tools designed for institutional use, not platforms built for quick clicks or simplified views of hedge fund activity.

Choosing the right hedge fund tracker

Choosing the right hedge fund tracker starts with understanding how hedge fund performance and holdings are reviewed within a family office. Elite investors rely on manager statements and capital cash flows, not inferred positions or public hedge fund news, to evaluate results and risk.

A hedge fund portfolio tracker should standardize how hedge fund holdings, performance data, and documentation are organized across entities and funds without replacing accounting systems. This structure allows teams to review exposure across strategies and regions, assess liquidity, and make informed portfolio decisions with confidence.

Public disclosure tools may surface hedge fund news or headline holdings, but they are not designed to accurately track hedge fund investments. Family offices evaluating a hedge fund tracker should prioritize tools that support allocator workflows, scale with structural complexity, and reflect how elite investors actually review hedge fund portfolios.

Asora and the other platforms outlined above are commonly reviewed by family offices seeking a structured way to track hedge fund investments and prepare consolidated reporting. Teams can request a demo to review hedge fund tracking workflows and quarter-end reports in context.

FAQ

How do family offices track hedge fund performance?

Family offices track hedge fund performance using manager-reported net valuations and capital cash flows. Time-weighted return (TWR) is commonly used to compare managers, while internal rate of return (IRR) is used selectively when cash flow timing matters. Platforms such as Asora support these calculations using manager-provided data rather than inferred positions.

Are hedge fund trackers useful for tracking hedge fund holdings?

Yes. A hedge fund tracker helps family offices maintain an accurate view of capital accounts, net asset value (NAV), and manager-reported exposures, including any look-through data provided, rather than assuming full underlying holdings transparency. This approach differs from tools designed for everyday investors, which often rely on delayed public disclosures and hedge fund news. In allocator-grade platforms like Asora, holdings and exposures are reviewed in the context of capital accounts and reported disclosures.

Can a hedge fund tracker replace accounting systems?

No. A hedge fund tracker supports performance review, exposure analysis, and document organization, but official books and records, reconciliations, and approvals remain within existing accounting and custodian systems.

Is a hedge fund tracker useful for non-US hedge funds?

Yes. Allocator-grade hedge fund tracking focuses on manager statements and cash flows, which are used globally. While public disclosures vary by jurisdiction, core performance and liquidity tracking processes are consistent across regions.

.png)