.jpg)

TL;DR

Family offices offer control, direct access to companies, and tailored governance, but require dedicated teams and workflows. Private equity funds offer manager expertise, vintage diversification, and established deal flow, but they also incur fees, carry, and limited liquidity. Asora brings direct and fund holdings into a single secure view, tracking governance documentation, fees, liquidity, and performance, so the trade-offs are clear and actionable.

What UHNW Families Must Weigh Before Picking a Model

If you’ve built significant wealth, you’ve likely considered investing beyond public markets. Private markets, spanning private equity, private credit, venture, and real assets (with room for secondaries and co-investments), are compelling. The practical question is how to access them: build in-house capability in a single-family office, allocate to funds as an LP, or blend both approaches?

Comparing options isn't really about which model is universally better; it's about understanding the operating requirements, risk profile, and resource demands of each approach so you can make informed investment decisions aligned with your family's capabilities and objectives.

This guide walks through what ultra-high-net-worth families should consider when evaluating family office direct investing versus private equity fund allocations (including the hybrid models many family offices use in practice).

What Each Model Is (Working Definitions)

Before comparing approaches, let's define terms clearly.

Family Office Investing (Direct/Hybrid)

An in-house investment mandate covers sourcing, due diligence, deal execution, and post-close ownership oversight. The family office builds internal capabilities to evaluate opportunities, negotiate terms, execute transactions, and directly monitor portfolio companies.

This model requires dedicated team members, specialist advisors, and operational infrastructure across the lifecycle. (Platforms like Asora centralise pipeline and investment records, documents, and performance monitoring in one secure system.) Capital is deployed on the family’s timetable, guided by shared values and a long-term vision.

Private Equity Fund Allocations (LP/Co-Invest)

You commit capital to private equity funds managed by firms with established track records. Fund managers (general partners) source deals, conduct diligence, negotiate transactions, and oversee portfolio companies. You participate as a limited partner, receiving quarterly reports and capital account statements.

Co-investment opportunities may provide access to specific deals alongside a fund's portfolio investments, often with reduced fees and expenses. This delegates execution to professional managers, allowing you to focus on selecting managers and constructing portfolios across vintages and strategies.

Quick note on related terms:

- Private office vs family office: ‘Private office’ isn’t standard terminology in wealth management. When used, it typically refers to either a single-family office or an executive support office supporting a principal’s personal and administrative needs.

- Family office vs private banking: Private banking services from financial institutions offer wealth management, lending, and trust services, but don't provide the comprehensive wealth management services or investment management capabilities of a dedicated family office. Private banking can cover many wealth services, but a dedicated family office typically provides broader coordination and oversight across providers and family priorities.

- Private trust company vs family office: A private trust company administers trusts for a family, handling fiduciary duties and estate planning functions. A family office provides a comprehensive range of services, including investment management, tax planning, lifestyle services, strategic planning, and trust administration.

Now let's compare the operating characteristics of each model.

Comparative Operating Considerations

The operating model drives outcomes, as staffing, processes, data flow, and cost cadence differ materially between direct investing and fund allocations. In brief, family office direct investing operates like a focused private equity shop, while PE allocations shift the work toward manager selection, pacing, and programme oversight.

Family Office Direct Investing

Your family office exercises discretion on investment pacing, deal structures, and governance. You create a bespoke mandate that reflects your family's risk tolerance, time horizon, and strategic interests, rather than fitting into a fund's predefined strategy. This provides greater control and flexibility in decision-making.

Running direct investments requires systematic processes:

- Deal intake and pipeline management tracking opportunities through various deal stages

- Due diligence protocols covering financial, legal, operational, and strategic analysis

- Investment committee cadence for review and approval of opportunities

- Post-close monitoring, including board participation, KPI tracking, and operational support

- Documentation standards ensuring proper contracts, governance docs, and compliance records

- Reporting infrastructure providing performance measurement and stakeholder communication (e.g., via Asora’s reporting dashboards and mobile access)

Unlike institutional investors with large teams, family offices typically operate with lean staff supplemented by advisors for specialized needs.

Family offices tend to invest where they already have an edge. Real estate families lean into property deals, while tech families gravitate toward venture. That focus can drive strong returns, but it also creates single-sector exposure and heavy reliance on one or two key people. Direct investing carries meaningful fixed costs, too:

- Investment staff

- Advisors

- Software

- Reporting tools

- Travel and diligence that go into each deal

The tradeoff is that all upside stays with the family, net of any incentive compensation paid to internal staff or external partners.

Owning companies directly provides access to rich information, including board seats, management meetings, data rooms, and regular operating metrics. The challenge is building systems so you don’t drown in unstructured data. And because execution risk sits entirely with your team, diversification only happens if you can source enough quality deals.

Asora links documents, workflows, and performance metrics to each asset, so information stays structured. Because execution risk resides with your team, diversification only occurs if you can source enough high-quality deals.

Strong family offices rely on co-invest partners, operating advisors, workflow tools, and periodic external reviews to manage risks effectively.

Private Equity (Fund/Co-Invest Allocations)

You gain access to manager expertise, established deal-flow networks, and operational resources that most individual families struggle to replicate, supporting long-term wealth preservation. Private capital firms invest across stages, including venture, growth equity, and buyouts, bringing specialist skills to each. Diversification follows by design: commit across multiple managers, vintages, and strategies to spread risk beyond what most single-family offices achieve through direct deals alone.

Allocating to private equity funds shifts work from deal execution to program management:

- Manager selection and operational due diligence, evaluating track records, team stability, process discipline, and alignment

- Pacing and unfunded commitment planning to ensure liquidity for capital calls while maintaining target exposure

- Document intake and organization as LP agreements, side letters, quarterly reports, K-1s, and capital account statements accumulate

- Capital call and distribution management, coordinating funding across multiple managers, and tracking deployed capital

- Ongoing monitoring through LPAC participation, annual meetings, and quarterly performance review

The work is substantial but different in character. You’re evaluating managers and monitoring portfolios rather than executing individual deals.

Private equity fund performance hinges on picking the right managers and spreading commitments across multiple vintages. A great manager in a favorable vintage can compound value for years, while poor manager selection (or committing too heavily in peak years) can drag down long-term results. Compared to direct investing, private equity funds typically diversify across sectors within a manager’s strategy and further diversify at the program level when you commit across multiple managers.

Costs come in the form of management fees and carried interest. A typical structure is ~2% management fees (often stepping down over time) and ~20% carry, though terms vary by fund. Internal overhead stays lean since you’re not running deals yourself, but fee drag compounds over a fund’s 10+ year life.

Information is received through standardized quarterly and annual reports, which vary in transparency across managers. Risk is reduced through fund diversification, but you still face the J-curve, long lockups, and limited liquidity. Savvy allocators manage these challenges through co-investments, negotiated side letters, selective secondary sales, competitive fee reviews, and ongoing monitoring of managers.

10 Key Differences Between Family Office Direct Investing and Private Equity Funds

Use this section as a quick diagnostic. It highlights the differences between family offices and private equity in terms of mandate, governance, pacing, resourcing, data, fees, liquidity, and risk, enabling decision-makers to determine where each model best fits.

1. Control vs Capacity

Family office: You maintain complete discretion over investment pacing (when to deploy capital), deal terms (governance rights, economics, timelines), and portfolio company engagement (board participation, operational input, exit timing). This control matters enormously when opportunities align with family capabilities or when governance preferences differ from typical PE approaches. You can be patient with capital when warranted, or move quickly when opportunities arise.

Private equity funds: You delegate discretion to firms in exchange for their capacity. General partners bring established deal flow, specialized sector expertise, operational resources, and network effects that individual families can't replicate. This capacity enables participation in opportunities you'd never access independently: exclusive investment opportunities driven by relationships, proprietary deal flow, and competitive positioning in processes. The trade-off: you accept their timeline, governance approach, and strategic decisions even when you might disagree.

2. Diversification and Concentration

Family office: Most family offices concentrate on domains where they have expertise or network advantages. A family that built wealth in manufacturing might focus its direct investments in industrials. A tech founder might concentrate on venture capital and growth equity. This concentration can generate superior returns where an edge exists, but it also creates portfolio risk. Building truly diversified direct portfolios requires broad deal flow and disciplined sizing.

Private equity: Fund structures create diversification at multiple levels. Each fund holds 10-30+ portfolio companies. Committing across 5-10 funds spanning vintages and investment strategies produces exposure to 50-200+ underlying companies. This program-level diversification significantly reduces the risk associated with a single company. Concentration risk shifts to the GP/strategy level but remains more diversified than typical family office direct portfolios.

3. Economics: Overhead vs Fee/Carry

Family office: Direct investing requires a team, advisors, and infrastructure. Overhead is highly variable; for a staffed direct investing program, it can run into the millions annually, depending on team size and structure. These are essentially fixed costs and persist regardless of whether you deploy $10M or $100M, making the model more attractive at scale. Critically, there's no carried interest, and 100% of gains flow to the family after costs are covered. For successful programs, this economic advantage compounds significantly over time. Technology that reduces manual work (e.g., Asora’s data aggregation and performance monitoring features) can lower the effective overhead per dollar deployed.

Private equity: Management fees (~2% of commitments, often $200K-$500K annually for typical allocations) plus carried interest (20% of profits) are externalized. Your internal team can be smaller (focused on manager selection and monitoring rather than deal execution), reducing base overhead. However, fee drag persists through market cycles. Over a fund's life, total fees often reach 5-8% of the committed capital, before considering the carry.

4. Liquidity Profile and Pacing

Family office: Exit timing rests entirely with your team. You can hold portfolio companies longer than PE funds (which face defined fund terms), capitalizing on patient capital advantages. Conversely, you can exit opportunistically when attractive offers emerge or strategic fit changes. This flexibility creates value in situations where timing is crucial, allowing for holding through short-term market dislocations or selling into valuation peaks. However, execution risk is yours.

Private equity: Funds operate with defined terms (typically 10 years or more, with extensions). This creates J-curve dynamics, where the early years involve capital calls and management fees, with minimal distributions as the portfolio companies mature. Liquidity emerges in later years through exits and distributions. If you need liquidity during mid-fund life, a secondary sale may be possible, but pricing depends on market conditions and fund quality; discounts to NAV can be meaningful in weaker markets.

5. Information Rights and Access

Family office: Direct ownership typically includes board seats or observer rights, regular management meetings, access to detailed operating KPIs, participation in strategic decisions, and data room access for specific initiatives. This information richness enables informed oversight and value creation through operational input. However, it creates a duty: you must standardize formats across portfolio companies, archive documents systematically, and create consolidated reporting across assets.

Private equity: LP reporting is delivered quarterly at the fund level, accompanied by annual audited financials. Transparency into underlying private companies varies significantly by manager—from comprehensive quarterly updates that include company-level operating metrics to minimal disclosure beyond fund-level NAV. Side letters can improve information rights for larger allocators, but you'll never achieve the granularity and timeliness of direct ownership.

6. Risk Management Levers

A family office's control over underwriting standards, post-close monitoring intensity, portfolio concentration limits, hedging policies, and exit strategies enables granular risk management. You set rules that match your family's risk tolerance, rather than accepting fund-level policies.

Private equity: Manager due diligence becomes your primary risk control, as choosing experienced teams with strong track records and aligned incentives is crucial. Vintage pacing spreads market risk across years. Secondaries offer liquidity options in case rebalancing becomes necessary. GP diversification across 5-10+ managers reduces the risk associated with a single manager.

7. Operating Rhythm and Governance

Family office: Direct investing follows a defined workflow—intake, diligence, investment committee approval, monitoring, and exit—under a governance framework that sets decision rights and authority levels, segregation of duties, conflict-management rules, risk limits (e.g., concentration, leverage, liquidity), documentation and minute-keeping standards, and approval/escalation protocols. Clear roles are one piece; the framework also covers the IC charter, valuation and impairment policies, legal/compliance checks (KYC/AML, related-party), and periodic audits/post-mortems to ensure accountability. Successful family offices view this as a serious operating infrastructure with workflow support to ensure consistent execution.

Private equity: Your work centers on quarterly fund-level activities, including reviewing capital account statements and NAV reports, analyzing fund performance against benchmarks and peer funds, participating in LPAC meetings on major fund decisions, managing capital call liquidity and pacing, and conducting periodic manager reviews. This quarterly cadence is more predictable than direct deal flow and requires less operational intensity; however, the cumulative work of managing 5-10 fund relationships remains substantial.

8. Talent and Key-Person Risk

Family office: Most single family offices depend on a small core, often one principal with investment background plus 1-2 professionals. This concentration creates significant key-person dependency: if your investment lead leaves or becomes unavailable, the program stalls. Mitigation requires conscious effort, including documented processes, external advisor relationships that provide continuity, succession planning to introduce next-generation family members, and systems that capture institutional knowledge.

Private equity: Private equity firms typically staff 10-50+ investment professionals with defined roles, succession plans, and institutional processes. While key-person risk exists (founding partners leaving or retiring can affect funds), you gain diversification across multiple GP teams in your portfolio. Single-manager risk in one fund is offset by the relationships with other funds.

9. Reporting Standards and Evidence

Family office: Direct holdings require asset-level fair value documentation, TWR (time-weighted return) or IRR (internal rate of return) calculations depending on cash flow patterns, roll-forwards between formal valuations, comprehensive reports supporting each position (board minutes, financial statements, valuation analyses), and both entity-level and consolidated reporting views. You bear full responsibility for developing and implementing defensible valuation methodologies, ensuring calculation accuracy, and providing documentation, organization, and evidence that link to support audit preparation. Technology supporting private assets tracking, performance monitoring, and document management becomes essential infrastructure rather than optional tooling.

Private equity: PE firms provide standardized capital account roll-forwards, quarterly NAV statements with fair value bases, IRR calculations by fund and vintage, annual audited financial statements, and K-1 or equivalent tax documents. You rely on management methodologies for valuations and performance calculations. The benefit is a reduced operational burden; the constraint is accepting their approaches and timelines.

10. Blending Models (Hybrid Approach)

Most sophisticated ultra-high-net-worth families blend both approaches strategically.

Family office: Lead direct investments where you have a genuine edge: sector expertise, network access, or operational capabilities, creating competitive advantages. Use co-investments with trusted PE partners for opportunities outside your core domain that you want exposure to. Maintain selective fund commitments to diversify, pace vintages, and access manager networks. This approach maximizes control where it matters while acknowledging capacity limitations.

Private equity: Build a core PE fund program that provides diversification and access to manager networks across strategies and vintages. Selectively pursue co-investment opportunities alongside fund commitments where you can secure fee relief (reduced or eliminated management fees and carry on co-invest capital) and gain direct exposure to attractive assets. This provides the benefit of manager expertise with some direct involvement and better economics on portions of capital.

Whether running direct investments, PE fund allocations, or hybrid approaches, you need operational infrastructure providing a single source of truth for:

- All assets

- Private asset registers with capital account roll-forwards and unfunded commitment tracking

- Document linking connecting LP agreements and board materials to specific private equity funds

- Workflow tasking managing capital calls, diligence processes, and monitoring requirements.

Asora provides a single, secure source of truth by unifying banks, funds, and private assets, along with performance monitoring, documents, and tasks, in one place.

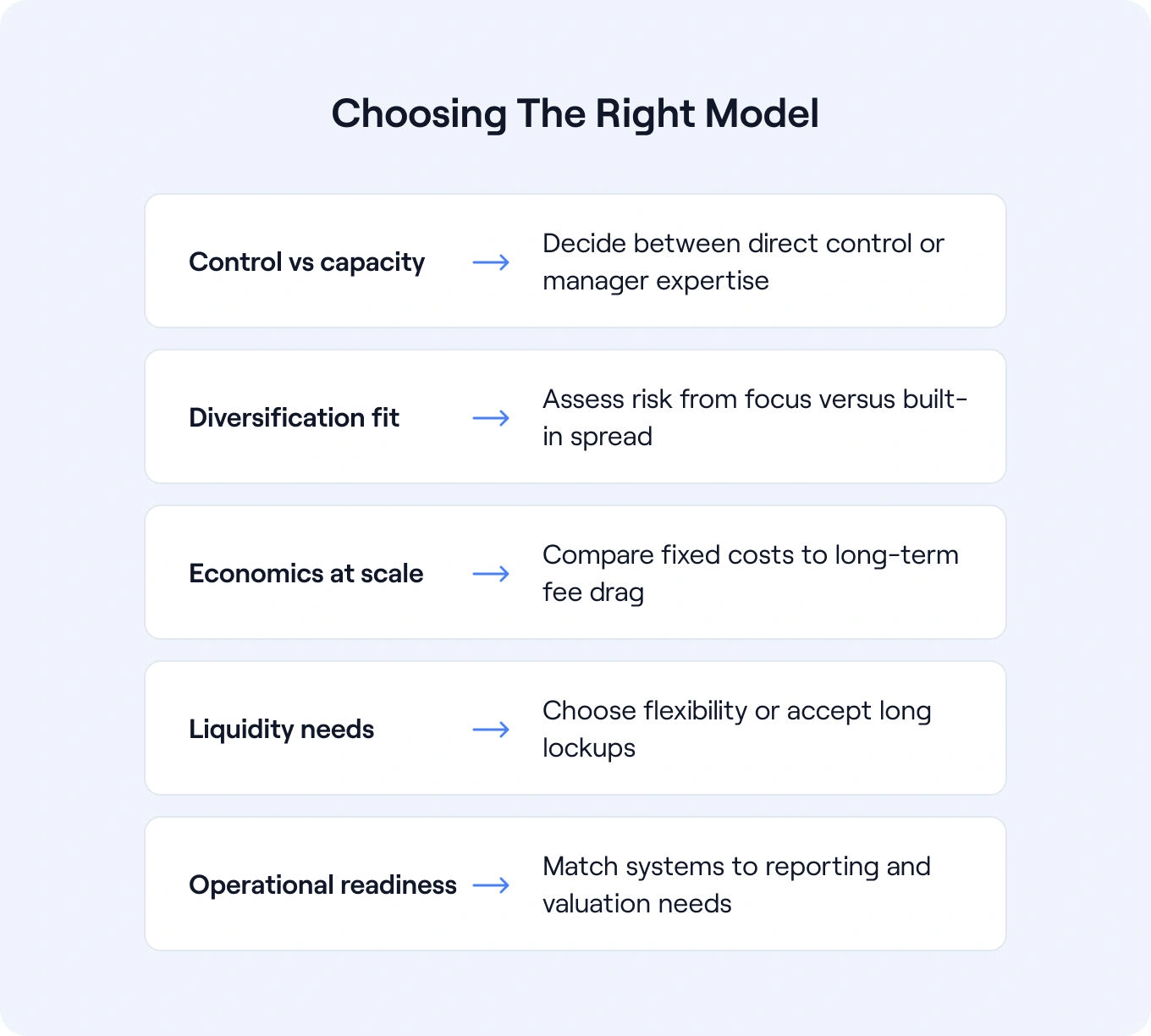

Matching Capabilities and Making a Choice

Ultimately, it’s all about matching your family's capabilities, resources, and objectives to the appropriate operating model.

- Control versus capacity: Do you have an edge justifying the effort to build direct investing capabilities, or is accessing firm expertise and deal flow a better use of resources?

- Diversification versus concentration: Can you realistically build a diversified direct portfolio, or does PE's structural diversification better manage risk?

- Economics at scale: At what asset level do direct investing economics (higher fixed costs, no carry) outperform PE allocations (lower overhead, persistent fees)?

- Liquidity requirements: Does your family need flexibility to generate liquidity on your timeline, or can you accept multi-year lockups with J-curve dynamics?

- Reporting and operational discipline: Do you have systems supporting defensible valuations, performance measurement, and evidence documentation, or does PE's standardized reporting better match your capabilities?

Whichever path you choose, direct, PE allocations, or a hybrid, the model must be operable by your team, monitorable with reliable systems, and defensible under advisor and auditor scrutiny. Asora provides UHNW families with a single, secure source of truth across banks, funds, and direct holdings, consolidating performance, documents, and tasks in one place.

See for yourself. Request a demo to see how your structure could work with Asora.

FAQ

How does family office versus private equity compensation compare?

Family office professionals are typically paid a salary and bonus, and investment gains accrue to the family after team costs. This is favourable for the family when programs succeed. PE funds charge management fees, typically around 2% of commitments, and carried interest, which is commonly ~20% carry, often subject to a preferred return in many buyout funds, though terms vary. This compensation for managers reduces net LP returns.

Should high-net-worth families invest directly or through private equity funds?

It depends on a few anchors: Asset scale. Direct economics improve at larger private market allocations where fee savings can justify internal overhead. Edge. Sector expertise, networks, or operating know-how that create an advantage. Organisational capacity. Team depth to run diligence, monitoring, and reporting, supported by systems to standardise workflows. Liquidity needs. Appetite for flexible exits in direct investing versus multi-year lockups in funds. Risk preferences. Discipline on diversification and position sizing for direct investing versus structural diversification in funds. Asora supports either path by aggregating bank and investment data, tracking commitments and capital calls, and standardising performance reporting and key metrics.

What are the key differences between a family office and private banking services?

Private banking offers advice, lending, and trust services, as well as access to products, but it typically does not provide the comprehensive investment management and coordination that a family office offers. A family office manages investments, taxes, governance, and operations from start to finish. Asora complements either setup by providing a single source of truth across accounts, funds, and private assets with audit-ready documentation.

How do ultra-high-net-worth families typically structure their private market investments?

Many use a hybrid. A common approach is 40 to 60 percent to PE funds across vintages and strategies for diversification and manager access, 20 to 30 percent to co-invests alongside trusted GPs for targeted exposure with reduced fees, and 10 to 40 percent to direct deals where the family has an edge. Asora makes hybrids operable by tagging holdings by strategy, maintaining private asset registers and capital activity, linking LPAs and board packs, and automating workflows for calls, distributions, and monitoring.

.png)