Table of contents

"What used to take hours or days is now done in minutes"

Donald Campbell

Partner at Capstone Family Office

Schedule Demo

TL;DR

Inheriting a family business is a great honor but a complex undertaking. This guide covers seven practical steps to prepare: mapping ownership and control, building a tax and liquidity plan, documenting operations, aligning governance, tidying the capital stack, creating reporting views, and setting up workflows. Preparation beats reaction.

Beyond Tax: The Operating Side of Inheritance

Inheriting a family business means more than receiving an asset. You’re stepping into a legacy – and one that comes with operational responsibilities, governance obligations, and tax implications that can easily catch unprepared heirs off guard.

It’s also important to distinguish what you own from the roles you take on. Simply being a shareholder doesn’t automatically put you in charge of running the business. But if you become a director, officer, trustee, or controlling shareholder, fiduciary duties may attach – meaning you must act in the best interests of the company and its stakeholders, not just yourself.

Most guidance on business inheritance focuses heavily on estate taxes and gift taxes. That's important, but it's not the whole picture. The heirs who manage smooth transitions are the ones who prepare beyond tax. They:

- Understand ownership structures

- Document operations

- Align with family members

- Build reporting systems before they're needed

This guide outlines seven steps to help the next generation prepare to inherit shares in a family business, whether they're gaining operational control, board influence, or an economic interest. We'll cover what to do, why it matters, and how modern tools can help you manage the complexity.

Note: Tax rules vary by jurisdiction. The examples below reference common US structures, but always work with qualified financial advisors and legal counsel for your specific circumstances.

7 Steps That Make Inheriting a Family Business Easier

These steps turn a complex handover into a manageable plan, with clear actions before paperwork and emotions peak. Use them as a checklist to align stakeholders, surface gaps, and put reporting and controls in place early.

1. Map Ownership, Roles, and Control for Business Inheritance

Before anything else, you need to understand who owns what (and who controls what). These aren't always the same.

- Start by mapping economic ownership versus control: share classes, voting arrangements, and shareholder agreements.

- Document board appointment rights and any trustee or protector powers if ownership is held through trusts or holding companies (and, where applicable, non-U.S. foundation structures). Note any trustee powers and any protector or committee rights, if they exist.

- Capture authorized signers, account authorities, and the corporate/board resolutions and bank signatory forms that evidence that authority —these details matter when a business owner passes and someone needs to act quickly.

Unclear ownership creates decision bottlenecks during transition and authority gaps in a crisis. Knowing exactly who can sign, approve, and act prevents costly delays.

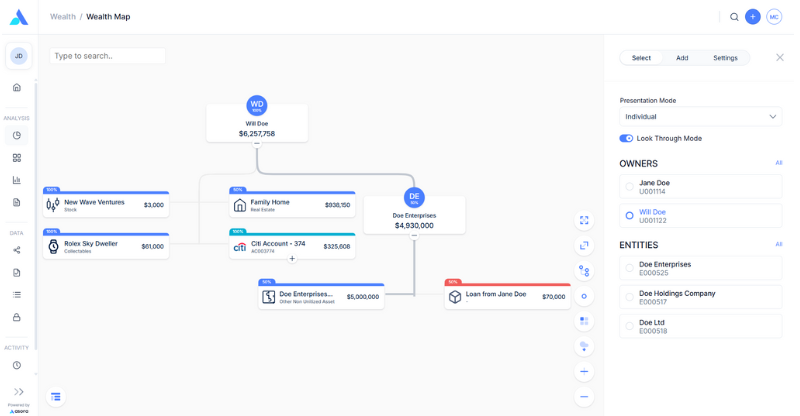

How Asora helps: The Wealth Map visualizes ownership across people and entities; Documents link directly to the relevant entities and holdings.

2. Build a Tax & Liquidity Game Plan for Succession

Family business inheritance tax planning is where many business owners focus first. Estate taxes, capital gains taxes, and transfer taxes can create major tax bills that can create liquidity pressure.

Estimate transfer-tax consequences across scenarios: death, lifetime gifting, trust distributions, and restructurings. Identify available reliefs in the relevant jurisdiction (for example, UK: business property relief and rollover relief; US: QSBS exclusion and step-up in basis). Then model liquidity sources: dividends, distributions, refinancing, asset sales, insurance proceeds, or family capital injections.

Depending on the jurisdiction, certain irrevocable trust structures can shift future appreciation to heirs and may reduce the taxable estate if the trust is properly drafted, funded, and administered. Outcomes depend on local tax rules.

Without a plan, heirs face forced scenarios, such as selling business interests at fair market value under time pressure or borrowing against business assets in an emergency. Many business owners underestimate how estate taxes can reduce the amount the next generation inherits.

How Asora helps: Private Assets tracking provides valuation snapshots, and the Wealth Map offers look-through visibility to underlying holdings for planning conversations with advisors.

3. Document the "Operator's Manual."

Every family business runs on institutional knowledge, but much of it is stuck in people's heads. That's key person risk, common in closely held businesses, and it becomes acute during generational transitions.

- Capture standard operating procedures for banking, payment approvals, and treasury cadence.

- Document payroll cycles, vendor relationships, required filings, and deadlines by domain (tax, payroll, corporate annual returns, licences, industry regulation, privacy/security obligations).

- List insurance renewals and covenant reporting requirements.

- Create incident playbooks for cyber events or operational disruptions.

If the current business owner becomes incapacitated or passes unexpectedly, successors need immediate operational clarity. The goal is a written record of how the company actually runs and not just what it owns.

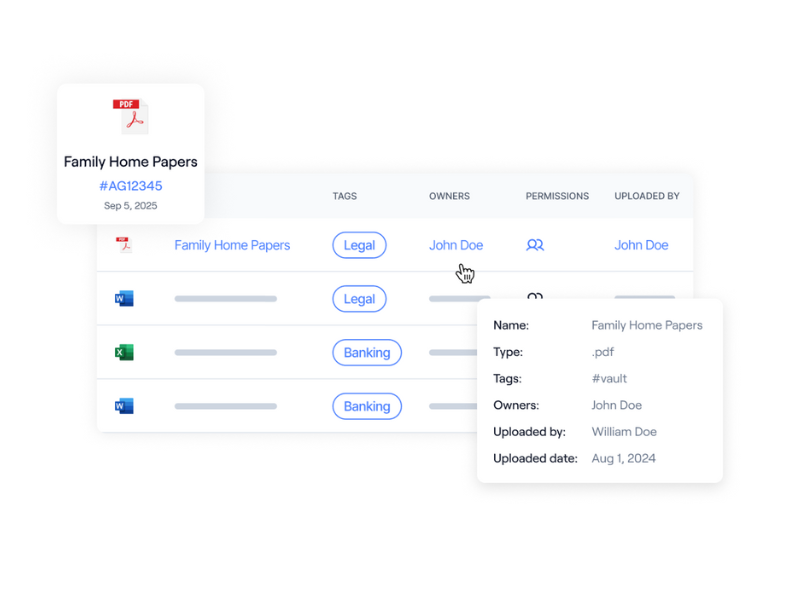

How Asora helps: Documents stored in context with tags and link them to entities; track renewal obligations as tasks via workflow support in Asora’s family office software.

4. Align Governance & Business Succession

Ownership succession and leadership succession are different things. A child might inherit shares but not be ready (or willing) to run the company. Clarity here prevents family business inheritance issues down the road.

Clarify board composition, decision rights, and escalation paths. Document meeting cadence and tie-break mechanisms. Review any family constitution or governance protocol, and separate executive succession planning from ownership transfer.

The person who inherits the company isn't necessarily the person who should lead it. Governance gaps create conflict. A clear succession plan keeps strategy intact and family members aligned even when circumstances change.

How Asora helps: Store meeting notes in Documents and link them to entities or assets; use workflow support to create tasks so follow-ups are tracked and decisions aren’t lost.

5. Tidy the Capital Stack & Agreements

Before the transition, catalogue the documents governing ownership, control, and cash flow.

- Review articles of incorporation, operating agreements, shareholder agreements, and trust deeds.

- Identify change-of-control triggers in loan agreements, key contracts, and regulatory licenses,

- Note relevant clauses (drag-along, tag-along, pre-emption rights, buy-sell provisions) and check for powers of attorney that need updating.

You don't want surprises when other assets or relationships become subject to third-party claims during transition.

How Asora helps: Store governing documents in Documents and link them to the relevant entities; use workflow support to create tasks with assigned owners to track covenant compliance and renewal dates.

6. Create Reporting for Principals & Advisors

The new owner will need visibility. So will advisors, family members, and any external stakeholders.

Build role-based reporting views:

- Principal/heir view with plain language summaries of key risks, liquidity, and structure

- Finance/ops view covering ownership schedule/share register, debt terms and covenant compliance (where applicable), cash flow, and KPIs

- Scoped reports for external advisors aligned to their specific mandates

Good decisions require good information, and building this infrastructure before transition means the new owner isn't scrambling to determine what they actually inherited.

How Asora helps: Performance monitoring and automated data aggregation power dashboards, and structured exports reduce manual rework for advisor packs.

7. Set Up Workflows and Task Tracking

Ongoing obligations don't pause for transition. Capital calls, debt maturities, insurance renewals, and statutory filings continue regardless of who's in charge.

Track obligations and key dates, assign tasks to family business owners, and provide clear escalation paths. Attach supporting documents and notes to create an internal record; use appropriate retention/approval controls where regulatory or lender requirements apply. Define who receives operational reminders versus financial risk flags. Small lapses, such as missed filings or overlooked renewals, can become costly problems, but systematic tracking prevents them.

How Asora helps: Use workflow support to assign and track tasks; store supporting files in Documents, linked in context to the relevant entity or task as evidence of completion.

Advantages and Disadvantages of Inheriting a Family Business

Before making final decisions about your role, consider both sides honestly.

- Advantages of family-inherited business: Inheriting a family business offers continuity of leadership, culture, and relationships. You become a steward of legacy across future generations, with the potential to create long-term wealth aligned with family purpose and values.

- Disadvantages of family-inherited businesses: The role comes with a governance burden and role-based fiduciary responsibilities. There's reputational risk tied to business performance, potential misalignment between operating needs and shareholder liquidity, and a tax burden that may require selling other assets or taking on debt.

Whether you're gaining operational control, board influence, or only an economic interest, understand what you're actually inheriting (and what it will require of you).

For more on preparing heirs, generational wealth planning, and family wealth protection, see our related guides.

Conclusion

Inheriting a family business doesn't have to mean inheriting chaos. With preparation, you can reduce the tax burden, avoid governance gaps, and step into ownership with confidence.

The seven steps above give you a practical starting point. Preparation beats reaction. Aim to shorten reporting cycles by improving data readiness, consolidation, and version control so routine reporting is faster and exceptions get attention.

Asora helps family businesses organize entities, documents, obligations, and reporting in one place. Request a demo to see how it works for your situation.

FAQ

Do you pay inheritance tax on family businesses?

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

What are the tax implications of inheriting shares in a family business?

Inherited assets generally receive a basis adjustment to fair market value at death (or alternate valuation date, if elected), but outcomes can vary by entity and trust structure. However, the taxable value of those shares may increase the taxable estate, potentially triggering estate taxes. Planning structures such as irrevocable trusts or a grantor-retained annuity trust can help manage exposure.

What are common family business inheritance issues?

Common issues include unclear ownership and retention of control structures, governance conflicts among family members, liquidity shortfalls to pay estate taxes, key-person risk when institutional knowledge isn't documented, and misalignment between heirs who want to sell versus those who want to manage the company. Asora helps on the operational side by mapping ownership, consolidating accounts and private assets, and linking documents to entities so stakeholders work from the same record.

How do I create a succession plan for a family business?

A succession plan should address ownership transfer (who inherits what, when, and how), leadership succession (who runs the business operationally), governance structures (board composition and decision rights), and financial planning (tax optimization and liquidity for heirs). Start by mapping current ownership and documenting operations, then work with legal and financial advisors to formalize the plan. Asora supports the process with consolidated reporting, document-in-context storage, and workflow support for task assignment and tracking across entities.

.png)

.jpg)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.webp)