.jpg)

TL;DR

Running an ultra-high-net-worth family office means managing entities, trusts, and multi-asset wealth with formal governance (often on non-institutional tools). This guide covers seven operational playbooks for UHNW families, plus a 30-day starter plan to move from scattered spreadsheets to one system of record.

UHNW Family Office Context: What "Running a Family Office" Really Means

An ultra-high-net-worth family office is the operating function behind a wealthy family's financial and administrative life. It is the infrastructure that manages entities, trusts, and diversified portfolios with institutional-level rigor, often adopting institutional-style policies and oversight (for example, an IPS, committee cadence, and documented decisions), tailored to one family’s objectives, values, and dynamics.

Unlike a typical private bank relationship, a family office can coordinate the entire ecosystem of advisors, entities, and operations, and may manage investments directly or via an OCIO or RIA, depending on staffing and mandate. Its role is to keep the whole picture aligned, clarify decision rights, and document decisions so multiple family members stay coordinated across generations.

Who this guide is for:

- Principals and family members overseeing significant wealth

- Family office leaders (CIO, CFO, COO) are responsible for daily operations

- Trustees and board members with fiduciary duties

- External advisors (legal, tax, investment) supporting the UHNW family office

We’ll focus on UHNW family offices in major jurisdictions (US, UK, European jurisdictions (country-specific rules vary)) with diversified portfolios spanning public markets, private equity, hedge funds, real estate, and operating companies. We'll address both single-family office and multi-family office structures, including hybrid models that blend in-house teams with outsourced support.

Ultimately, many early-stage or lean ultra-high-net-worth family offices carry institutional responsibilities on non-institutional tooling. Financial affairs live in spreadsheets. Documents are scattered across inboxes and shared drives. Governance happens in meetings, but decisions are often not consistently documented in a searchable, auditable way.

This creates operational, reporting, and information security risks, plus data governance gaps as complexity grows. That compounds as wealth complexity grows and the next generation enters the picture.

The playbooks below address that tension directly.

7 Proven Playbooks for UHNW Operations

Each playbook is a tested pattern for lean teams: what to do, who owns it, and the checkpoints that keep multi-entity, multi-asset operations on track. Pick one to deploy this quarter.

1. Ownership, Governance, and Decision Cadence

Running a UHNW family office starts with clarity on who owns what, who decides what, and how often decisions get made. Without this foundation, everything else (investment management, reporting, succession planning) operates on shaky ground.

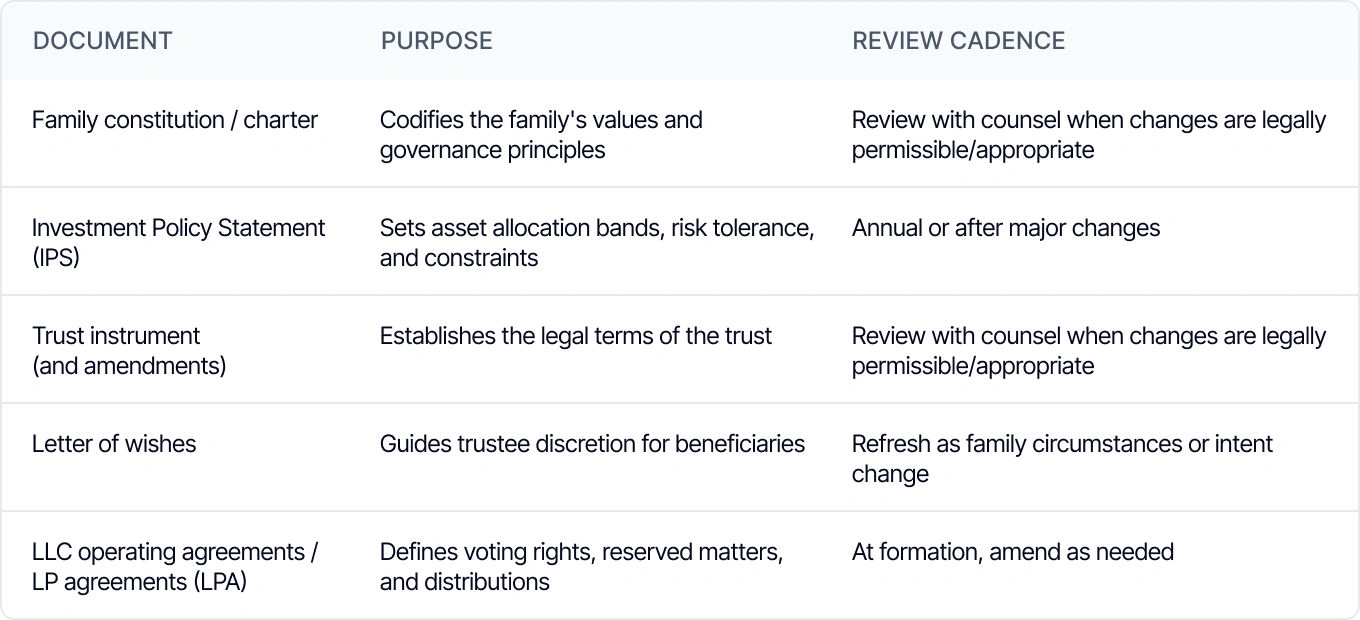

| Document | Purpose | Review Cadence |

|---|---|---|

| Family constitution/charter | Codifies the family's values and governance principles | Annual |

| Investment Policy Statement (IPS) | Sets asset allocation bands, risk tolerance, and constraints | Annual or after major changes |

| Trust instrument (and amendments) | Establishes the legal terms of the trust | Review with counsel when changes are legally permissible/appropriate |

| Letter of wishes | Guides trustee discretion for beneficiaries | Refresh as family circumstances or intent change |

| LLC operating agreements / LP agreements (LPA) | Defines voting rights, reserved matters, and distributions | At formation, amend as needed |

And here are the decision bodies you’ll want to establish:

- Investment committee: Reviews portfolio, approves new managers, monitors performance. Monthly for active public markets or high activity; quarterly plus ad-hoc approvals for private-market-heavy portfolios

- Family council: Addresses family dynamics, education, philanthropy, and legacy planning. Quarterly or semi-annual.

- Trustees/board: Handles fiduciary matters, major distributions, and structural changes. As needed.

Keep agendas short and outcome-focused. Maintain a decision log (linked to minutes/resolutions and supporting documents) capturing what was approved, when, and by whom. Create an entity structure map showing ownership/control, trustees/beneficiaries (where relevant), and links to key accounts/assets.

How Asora Helps: Asora’s Wealth Map is an ownership chart that links people to entities across trusts, SPVs, and holding companies; meeting notes can be stored in Documents and linked to entities, and Workflows provide task-tracking and follow-up support.

2. Investment Oversight & Liquidity Planning

Whether your UHNW family office manages investments in-house or partners through a combination of an OCIO or RIA, a private bank for custody and lending, and specialist managers, you still need oversight infrastructure to coordinate governance, reconcile data, track risk and liquidity, and document decisions. The UHNWI family office role is to monitor, coordinate, and help ensure investments align with the family's goals and risk tolerance.

What to document:

- Asset allocation bands: Target ranges by asset class (e.g., 20–30% private equity, 10–15% real estate)

- Liquidity buckets: Operating/tax (0-3 months), known obligations (3-12 months), planned spend (12-36 months), strategic (3+ years).

- Concentration limits: Maximum exposure to any single manager, sector, or geography

- Spending and distributions: Spending policy (lifestyle and philanthropy budgets) plus a funding plan for obligations (tax, debt service, capital commitments), coordinated with trust and entity distribution constraints.

- Private markets pacing: Commitment schedule for PE/VC to manage unfunded obligations

- Debt profile: Maturity dates plus rate resets, covenants, collateral, and margin or liquidity triggers, not just when loans technically come due.

Hold regular check-ins—monthly for active portfolios, quarterly for more stable allocations. Maintain a forward-looking cash flow forecast with base and downside scenarios. Tie each obligation to source documents: capital call notices, loan statements, distribution notices.

How Asora Helps: Automated data aggregation pulls data from banks and custodians. Store call notices in Documents, and export reports for advisor sessions.

3. Private Assets & Alternative Investments

Private funds (PE/VC), semi-liquid alternatives (many hedge funds), direct real estate, and collectibles each have different reporting/valuation mechanics. Valuations lag. Documents drive data. And the administrative burden scales with each new commitment.

For private funds, the best UHNW private wealth management and family offices track:

| Data Point | Source | Update Frequency |

|---|---|---|

| Commitment amount | Subscription docs | At closing |

| Called capital | Capital call notices | As received |

| Unfunded commitment | Calculated | After each call |

| Distributions | Distribution notices | As received |

| GP-reported NAV | GP or administrator | Quarterly (as-of quarter-end, received with lag) |

| Fees & expenses | Fund statements / LPA | Quarterly (management fees & expenses); carried interest per fund terms |

| Tax reporting (e.g., K-1 in the US) | Partnership/fund administrator | Annually (often late; may be amended; jurisdiction-dependent) |

For direct real estate, track:

- Ownership entity and debt terms

- Rent roll and net operating income (NOI)

- Capex plan and major improvements

- Valuations and appraisals (note "as of" date and source)

Maintain an integrated private assets inventory, with sub-registers by asset type to capture the right fields and workflows. Link documents to each holding. Flag data timeliness. Private valuations are inherently lagged, so always record the "as of" date and valuation source (custodian, administrator, GP statement).

How Asora Helps: Private asset registers with document linking.Documents link files to the live record to reduce email back-and-forth.

4. Documents-in-Context & Due Diligence

A family office UHNW accumulates thousands of documents: LPAs, side letters, facility agreements, insurance policies, trust deeds, tax returns, and more. The challenge isn't storage, though. That’s the easy part. It's retrieval.

Can you find the right document when you need it?

Document categories to organize:

- Investment documents: LPAs, subscription agreements, side letters, quarterly statements

- Entity documents: Operating agreements, trust deeds, corporate minutes

- Legal/compliance (where applicable): Lending documents, guarantees, entity filings, and any required regulatory/tax filings, depending on structure and jurisdiction

- Insurance: Policies, certificates, claims history

- Tax: Returns, elections, correspondence with authorities

- Privileged materials: Attorney-client communications (separate access tier)

Use standard naming conventions. Tag by entity and asset. Set renewal reminders for policies and agreements. Define retention periods and access tiers. Not everyone needs access to everything.

Clarify whether due diligence is handled internally or via external advisors. Either way, the UHNW private family office should maintain an investment memo trail, approvals, and key DD artefacts proportionate to risk.

How Asora Helps: Documents stored in context with tags; link them to entities, assets, or transactions; use workflow support to assign and track renewal tasks.

5. Reporting Done the Right Way

Reporting serves two audiences with different needs: principals who want clarity, and advisors who need detail.

Principal reporting:

- Separate packages: net worth (balance sheet), performance (public and total-portfolio with valuation lag caveats), and liquidity/commitments (cash, debt, unfunded, known obligations)

- Tailored to preferences and security policy

- Mobile access is optional for principals who want it

- Frequency: monthly or quarterly, depending on engagement level

Advisor reporting:

- Investment advisor: Holdings, performance, transactions, forward commitments

- Tax advisor: Realized gains/losses, income, cost basis, entity-level detail

- Legal/estate advisor: Entity structure, ownership changes, governance decisions

Build from one source of truth. Use live dashboards for on-demand visibility and schedule exports to ensure reports go out consistently. Avoid rebuilding in spreadsheets, where errors creep in. For best practices, see our complete guide to family office reporting.

How Asora Helps: Consolidated reporting allows users to export reports directly from the platform; link notes and tasks to the underlying records (via workflow support on dashboards, not exported reports) so reporting packs can reference the period’s activity as well as the numbers.

6. Risk, Cyber, and Access Hygiene

UHNW families are high-value targets. Financial security requires more than strong passwords. It requires systematic risk management across people, processes, and vendors. That starts with implementing:

- MFA where supported: Every system, every user

- Role-based access: Least-privilege sharing—users see only what they need

- Vendor due diligence: Request SOC 2 Type II reports (attestation) and/or ISO 27001 certification where applicable; for financial institutions, obtain relevant control reports (often SOC 1), security questionnaires, and incident history

- Incident basics: Know who to call if something goes wrong

Review access on a defined schedule: quarterly at a minimum, plus every personnel or vendor change. Apply least privilege. Time-bound access for temporary needs. Confirm audit/event log availability, retention, and export options, plus incident notification SLAs.

For a deeper look at cybersecurity for UHNW single-family offices, see our cybersecurity guide.

How Asora Helps: MFA, role-based access controls, and ISO27001 certification. Exports for external advisors.

7. Succession and Next-Gen Education

Wealth preservation across multiple generations requires more than estate strategies and asset protection strategies. It requires preparing the next generation to be informed stewards. You do this by building:

- Quarterly learning plan: Structured education for next-gen family members and trustees

- Scenario-based training: Simulations and tabletop exercises (e.g., "What happens if the principal becomes incapacitated?") Include role clarity (trustees/POA/executors), access readiness (vaults, signatories), and decision triggers.

- Philanthropy as a training ground: One structured cycle per year where next-gen members participate in philanthropic advisory and grant decisions

Focus on small wins and clear responsibilities. Track dates, touchpoints, and outcomes (sessions completed, simulations run, and grants approved). Make learning visible so progress compounds.

How Asora Helps: Documents and notes are linked to entities, people, and vehicles. Progress tracking via task boards. The platform supports family office operations without replacing your existing advisors and tools.

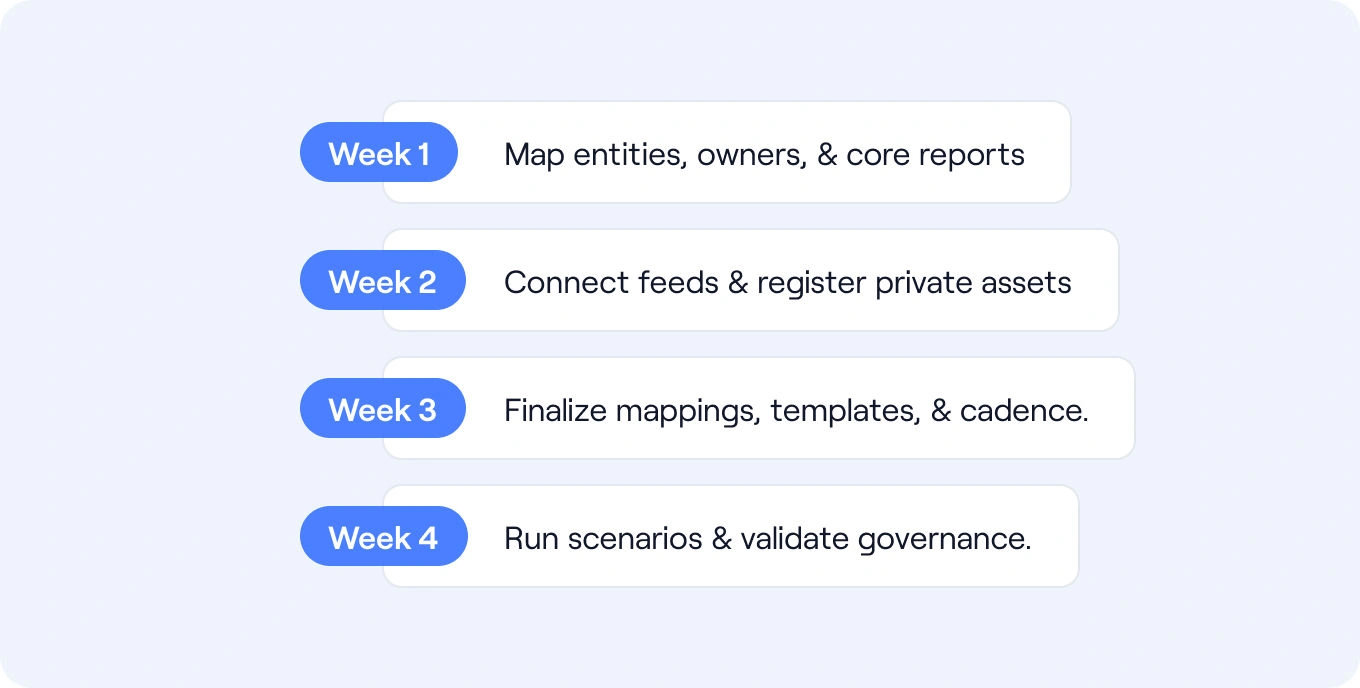

30-Day Starter Plan

Moving from scattered systems to structured operations doesn't happen overnight. Here's a realistic four-week plan:

Week 1: Foundation

- Map entities and owners

- Centralize your highest-value documents

- Define baseline reports (net worth, performance, liquidity)

Week 2: Connections

- Connect secure bank and investment feeds in your existing system; if feeds are unavailable, set a documented import cadence.

- Create private asset registers

- Tag documents with renewal dates

Week 3: Structure

- Finalize mappings: entities ↔ accounts ↔ owners

- Define classifications: asset class, liquidity buckets

- Create reporting templates

- Set meeting cadence and assign tasks

Week 4: Test

- Run a scenario: capital call funding + document capture + approval trail + post-transaction reconciliation

- Include a renewal/insurance review

- Use your governance body (investment committee, trustees, family council) to validate the process

By the end of 30 days, you'll have a baseline system of record foundation: an entity map, central documents, initial reporting definitions, and a tested workflow for a common event (e.g., a capital call) that drives UHNW family offices.

Conclusion

Running an ultra-high-net-worth family office means holding institutional responsibilities with a lean team. The families who do it well share common traits:

- One system for data, documents, and workflow support

- Short meetings with clear agendas

- Timely reporting that doesn't require rebuilding spreadsheets

- Fewer emails because information lives where it belongs

Whether you're running a single-family office, a multi-family office (MFO), or a hybrid model with external advisors, the playbooks above apply. Start with governance and ownership clarity. Build from there.

Asora supports UHNW family offices with data aggregation, private asset tracking, performance monitoring, and document management, all linked to one record.

Request a demo to see how it works for your structure.

FAQ

What's the difference between a single-family office and a multi-family office?

A single family office provides fully customized support to one family. A multi-family office serves multiple families, sharing infrastructure to lower costs. Some families start with an MFO and build a single-family office as their wealth and complexity grow; others remain MFO/hybrid long term or shift models over time.

What services does a UHNW family office provide?

Family office services for UHNWIs usually include investment oversight, tax planning, estate and legacy planning, trust and entity administration, financial reporting, risk and insurance management, philanthropy, and sometimes concierge or lifestyle support. The mix depends on the family’s needs and on what stays in-house versus what is outsourced.

How do UHNW families handle private equity and alternative investments?

Many UHNW families allocate a meaningful portion to private markets and alternatives, depending on liquidity needs, risk tolerance, and access. These assets need different tracking: delayed valuations, document-driven data, and growing admin work. Teams or platforms track commitments, capital calls, distributions, GP-reported NAV, and unfunded exposure by vintage, pacing vs. plan, fee/expense drag, and GP/strategy concentration, with proper as-of dates.

.png)