.png)

TL;DR

Family wealth education prepares the rising generation to understand the structures and responsibilities they'll inherit. This guide covers seven practical strategies: mapping ownership, learning from real documents, creating a living learning plan, using small decisions to teach big principles, building philanthropy modules, teaching security basics, and running simulations.

From Newcomer to Involved Owner

Family wealth doesn't come with an instruction manual. Whether your family oversees a liquid investment portfolio, an operating business, or both, the structures behind that wealth aren't obvious to someone encountering them for the first time.

This guide is for families working with a single-family office, multi-family office, corporate fiduciary/private trust company,, or team of trusted advisors who want to engage younger family members before they're thrust into decision-making roles unprepared.

The goal isn't to create mini-CFOs. It's to build informed confidence so the next generation can participate meaningfully in family governance, ask good questions, and eventually take on real responsibility.

Why Family Wealth Education Matters Now

Multi entity structures add moving parts: reporting requirements, decision rights, governance and approval paths, tax filings, and distribution rules. Where trusts or foundations are involved, you also need clear distribution policies and consistent communications with beneficiaries. Without education, younger generations inherit complexity they don't understand.

The risks of delay are real: Missteps in information sharing and approvals that lead to tax problems, poor liquidity planning, unnoticed concentration risk, governance drift as family dynamics shift, and surprise conflicts when distributions don't match expectations. Many families discover these gaps only when something goes wrong.

The desired outcome is simpler: Informed stewardship across generations, fewer surprises in decisions and distributions, and family members who can engage with financial advisors and legal counsel as partners rather than passive recipients.

Before starting any program, align on your disclosure philosophy. Some families prefer full transparency from an early age. Others stage information based on maturity or role. There's no single right answer, but there should be a deliberate choice that respects privacy, security, family dynamics, and any legal, fiduciary, or confidentiality obligations (including those of regulated advisors and fiduciaries).

7 Financial Education Strategies to Engage the Next Generation

These strategies make finance tangible for rising family members and build confidence through practice rather than theory. Use them to create a consistent rhythm for learning and participation.

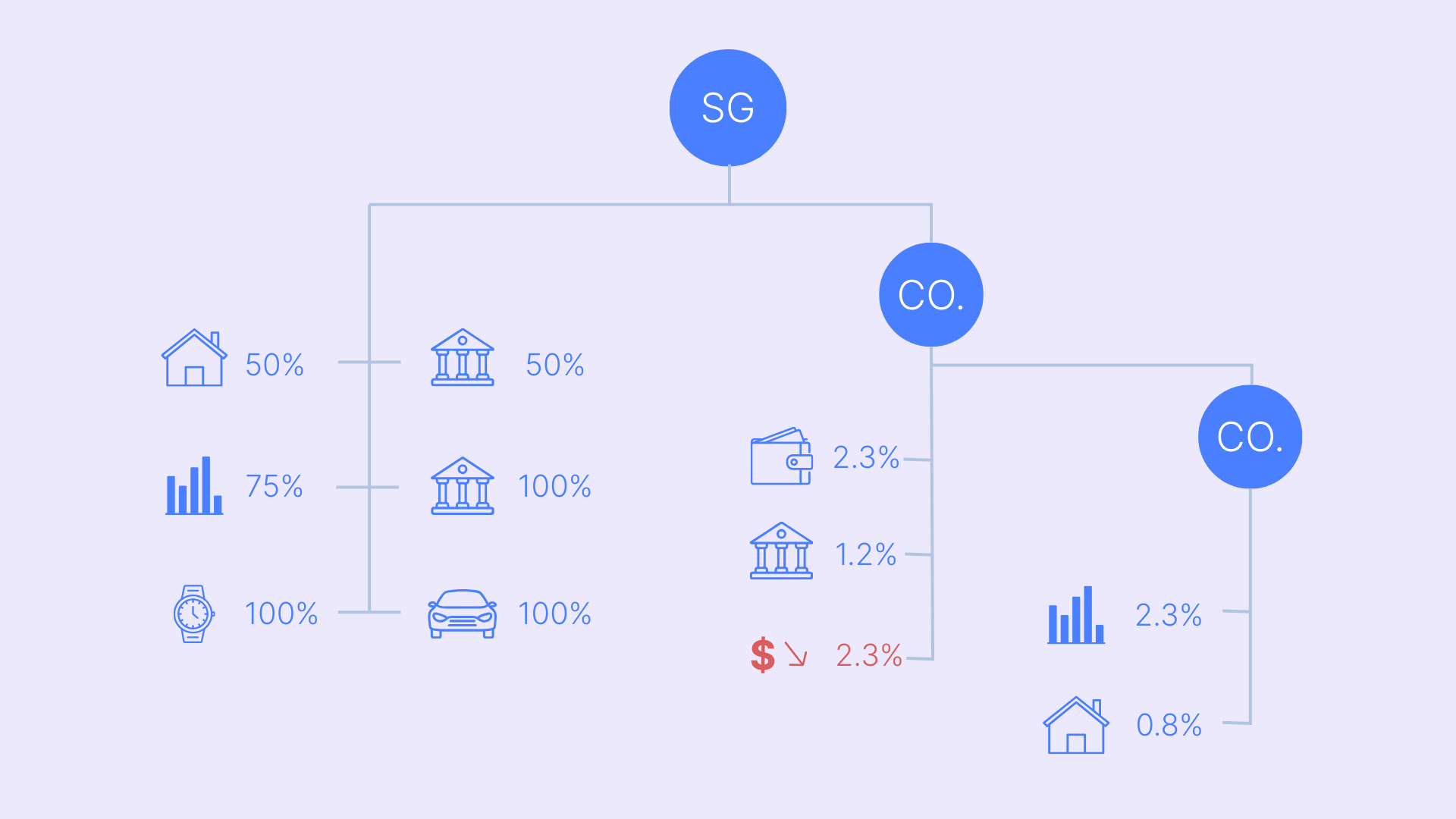

1. Define Roles with a Simple Ownership Map

Start with clarity on who holds what role and what that role actually means. Economic interests, control rights, and information rights are distinct and depend on the governing documents and jurisdiction. A beneficiary of a trust has different powers than a trustee, and beneficiary powers (if any) depend on the trust deed (e.g., removal rights, powers of appointment, protectors). A shareholder in a family business has different rights than a board member.

Create a simple entity map showing relationships, control, and beneficial interests across trusts, companies, foundations, and donor-advised funds. Specify where decisions legally sit.

This becomes the foundation for everything else.

Avoid describing trust assets as ‘owned’ by beneficiaries unless they have direct legal title or clearly defined withdrawal/appointment rights. That distinction matters for governance, tax, and family expectations.

2. Make Learning Concrete with Real Statements and Documents

Abstract financial concepts don't stick. Real documents do.

- Walk younger family members through actual bank statements, investment reports, partnership agreements, subscription documents, and distribution notices. Use redacted examples or role-based access to protect sensitive data.

- Show them an insurance schedule.

- Explain what a capital call notice means.

- Let them review common reports (custodian statements, manager letters, and private fund quarterly reports/capital account statements).

Wealth education helps build financial literacy by exposing them to the real materials they'll eventually need to understand.

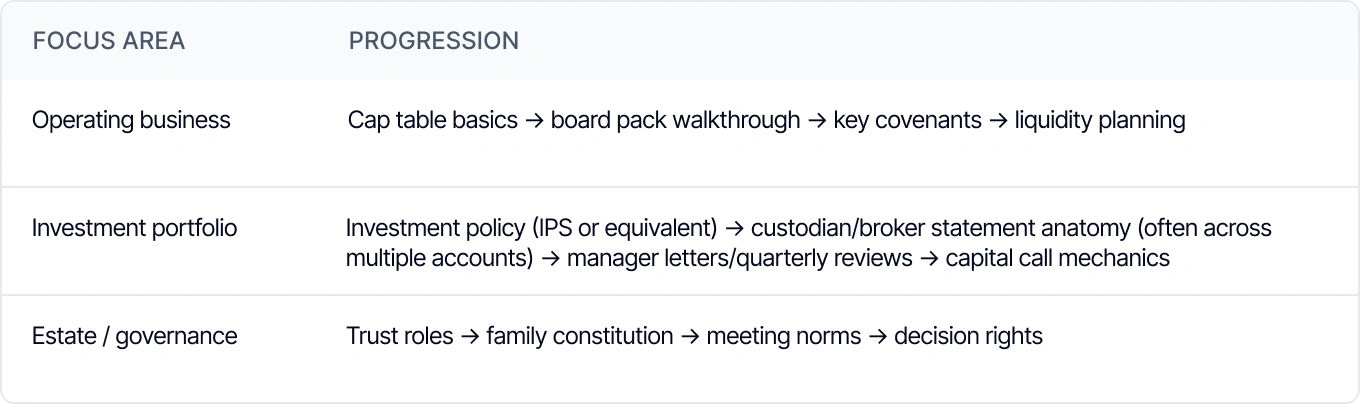

3. Create a Living Learning Plan for Family Wealth Management

Family wealth education works best with a consistent cadence instead of one-time lectures or an overwhelming data dump.

Set quarterly goals that are developmental, not evaluative. Pick 1–3 milestones per quarter: read the cap table, attend part of a board meeting as an approved observer where appropriate (with NDA/permissions), or review a redacted board pack instead , review one loan covenant, and understand how a capital call works. Track completion dates and capture what was learned, along with questions for next time.

Sample learning tracks:

Match the track to your disclosure philosophy and the learner's current role. Keep it scaffolded: vocabulary first, then documents, then decisions.

4. Use Small Decisions to Teach Big Principles

Before asking the next generation to make investment decisions, let them observe how decisions get made. Walk through a recent decision:

- What changed

- Who approved it

- What data supported it

- What trade-offs were considered

Discuss risk across dimensions: market, liquidity, concentration, operational, legal and tax, counterparty and custody, valuation for private assets, and key person for operating businesses. Explain how time horizon changes the calculus, from drawdown sensitivity in the short term to lockups, regime shifts, and succession over longer periods. Use simulations to build financial acumen without risking real money.

5. Build Philanthropy and Impact Modules

Philanthropy offers a natural training ground for governance, budgeting, and stewardship. Whether your family uses a private foundation, donor-advised fund, or direct giving, involve younger generations in the process.

Show how it works in your structure (foundation vs DAF), including any legal requirements (e.g., expenditure responsibility where applicable) and how impact is monitored. Let them explore causes aligned with family values and present grant recommendations, or, where applicable, ideas for mission-related investing (MRI) / program-related investments (PRI) or endowment allocation.

This builds confidence in managing money for impact—skills that transfer well to governance and disciplined decision-making, and can complement investment education.

6. Teach Data Hygiene and Security Basics

High-net-worth families are targets. Part of wealth education is teaching security practices that protect assets and privacy.

Cover the basics:

- Why MFA matters

- How to spot phishing

- How to use password managers

- Ways to improve device security

- Secure sharing practices

Discuss access by role (family members, staff, trustees, advisors), and document what is shared, why, and under what confidentiality/fiduciary constraints. Review how vendors get access and how that access gets revoked. For more details, see our guide on cybersecurity for family offices.

7. Run a Simulation

Nothing builds confidence like practice. Create mock workflows in which the next generation supports the tax process (collecting documents, tracking K-1s, validating source data, and coordinating approvals), coordinates approvals among family members, or validates documentation for a trust distribution, dividend, or owner draw, consistent with the governing documents and approvals.

For distributions specifically, simulate the decision-support and documentation flow without actually moving money. Note fiduciary constraints and who has authority. This lets younger family members experience the process safely before they're doing it for real.

Measuring Financial Literacy Progress Without Overwhelming

Keep measurement light. A simple readiness checklist is more effective than formal assessments. Use reflective prompts rather than tests. Ask learners to explain concepts back to you. Capture questions that come up. Track milestones completed and dates achieved.

Progress should feel encouraging instead of purely evaluative.

Common Pitfalls (and Easy Fixes)

.webp)

Here’s where many families fall short and (more importantly) how they can make it right:

- Teaching only theory: Use real statements, real documents, real decisions.

- Burying learners in jargon: Start with vocabulary, then build to documents, then decisions.

- Keeping documents scattered: Centralize with governance: role-based access, retention policies, version control, and clear ‘system of record’ rules; use secure portals where counterparties require them.

- Unclear roles: Map legal entities and ownership, and separately map decision rights (who initiates, approves, executes) before education begins.

- No cadence: Set quarterly goals with monthly touchpoints.

How Asora Helps with Family Office Wealth Management

.jpg)

Asora supports family wealth education by giving teams a single system to teach with real records (with appropriate access):

- Entity map: Documented look-through view of beneficial interests and control across trusts, SPVs, and holding companies via the Wealth Map

- Documents in context: Secure storage with tags; link files to entities, assets, and transactions

- Private asset depth: Track cost basis/carrying value, manager-reported NAV (for funds), capital accounts, and periodic valuation marks where available

- Learning cadence: Use workflow support for task assignment and tracking; store meeting notes in Documents

- Timely data: Bank/custodian f eeds plus manual upload paths; data freshness depends on source latency

- Reports and exports: Export CSV, XLSX, and PDF with consistency for teaching from the live record

- Security and access: MFA and role-based access controls aligned to your disclosure approach

For more on family office operations and governance structures, see our related guides.

Conclusion

Many families can start without a formal curriculum, but complex situations may benefit from specialist legal, tax, governance, or security support.

Start simple: map ownership, use real documents, set quarterly goals, and track progress in one place. The rising generation learns best by engaging with actual records and observing real decisions.

The families who do this well raise children who become confident stewards, capable of working alongside advisors, participating in governance, and eventually taking on responsibility for the legacy they've inherited.

Request a demo to see how Asora helps families organize entities, documents, and learning plans in one system.

FAQ

How do you teach financial literacy to younger family members?

Start with real documents. Walk through actual statements, reports, and agreements. Use small decisions as teaching moments. Create a quarterly learning plan with 1–3 concrete milestones. Asora can support this by storing documents in context, linking them to entities or assets, and using workflow support to assign and track learning tasks.

How do you balance transparency with privacy in wealth education?

Align on a disclosure philosophy before starting: full transparency, staged disclosure based on age or role, or role-based access where different family members see different information. There's no universal answer, but the choice should be deliberate and consistent.

.png)