Author

.jpg)

Table of contents

"What used to take hours or days is now done in minutes"

Preparing heirs for wealth management involves building a structure now so they can make informed decisions later. Successful transfer requires clear decision rights, well-organized documentation, systematic training, and a platform that connects numbers to evidence. Asora centralizes accounts, private assets, documents, and workflows, enabling heirs to transition from summary to source quickly with evidence-linked records that support a taxable estate.

Most principals are familiar with the wealth structure in detail. They understand the purposes of entities, investment rationales, and the responsibilities of advisors. Heirs are capable, but they do not live it every day.

The issue is not whether they can learn; it is whether a system exists that enables sound decisions when the principal is unavailable.

Adequate preparation is not about cloning the founder. It is about clear roles, organized information that enables five-minute decisions, and routines that build judgment over time.

Effective transfer goes beyond simply moving assets and understanding the implications of a taxable estate. It aligns estate planning, including estate and gift tax considerations and exemptions, with operational readiness. That means documentation, workflows, and context for why each asset is held.

The framework below provides a practical, effective approach to stewardship in real-life situations.

.webp)

Decisions arrive before confidence. Structure prevents avoidable mistakes.

Before diving into long-term preparation, run these six checks to understand your current readiness:

If you struggled with more than two of these, you're not alone. However, you have work to do before considering long-term estate planning.

Platforms like Asora address these structural needs with:

This lays the foundation for heirs to make informed decisions about family assets and investment strategy.

.webp)

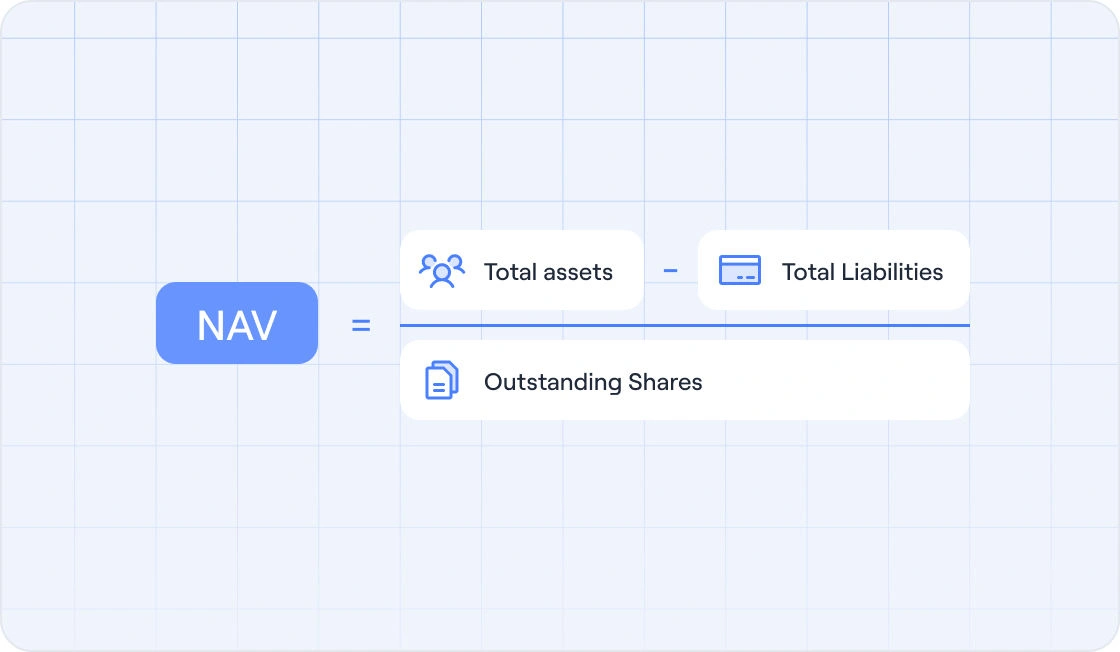

Numbers and evidence belong together. A five-minute decision requires both. The best way to transfer wealth to heirs begins with organizing information so they can quickly find what they need.

Your heirs should be able to answer two questions instantly:

This requires a consolidated view with look-through to ultimate ownership and clean entity rollups. It's a system that automatically reflects current positions.

The entity map shows who owns what through which structures. Entity-level reporting rolls up to family totals. Performance tracking shows returns at both granular and consolidated levels.

Asora's Wealth Map displays ownership look-through across typical entity structures such as trusts, SPVs, and holding companies. It helps heirs understand the structure and allows them to drill down to assets.

Private investments complicate the process of passing wealth to heirs. Heirs need to track:

Unfunded commitment tracking drives cash pacing. When $15M in capital calls arrive next quarter, that affects liquidity management and other investment decisions.

Keep this information structured with linked documentation (LPAs, side letters, capital account statements) so that heirs can review details without having to search through emails.

Asora's Private Asset functionality tracks commitments, calls, and distributions with linked documents, and calculates IRR and Multiple.

Heirs need visibility into:

This informs decisions: Can we commit to this new fund? Do we need to sell something to meet upcoming calls? Are we too concentrated in a single manager or sector?

Understanding the market value of assets and the cost basis of positions enables heirs to make tax-efficient decisions when liquidating holdings to meet obligations or rebalance their portfolio.

Dashboards should clearly surface this information, with the ability to export it for advisor discussions or investment committee packs.

Beyond financial data, heirs need access to governing documents tied to specific decisions:

Don't just file LPAs alphabetically. Link them to the specific investments they govern so heirs can reference the right agreement when making decisions.

Request documents from outside parties through your usual channel (email or portal). They send the file securely without Asora access, and your team uploads it to Documents, tags it, and links it to the right asset or entity, so the evidence sits one click from the numbers.

Clarity beats charisma: capture decision rights, approval thresholds, key contacts, and plain-language summaries in one searchable source of truth, with checklists for routine actions. Repetition builds judgment: run monthly mini-reviews, quarterly scenario drills, and advisor shadowing until playbooks run themselves, then add measured autonomy with quick debriefs.

Start with explicit decision frameworks:

Establish "no approval without the reports". Decisions require supporting documentation, and meeting minutes cite specific files.

This isn't bureaucracy for its own sake. It ensures that decisions are made with proper information and creates an institutional memory of the reasons for those choices. This becomes especially important when managing a family business or trust assets where multiple family members have interests.

Workflows in Asora help assign tasks with specific dates and keep evidence linked to documents, ensuring the approval process remains organized and efficient.

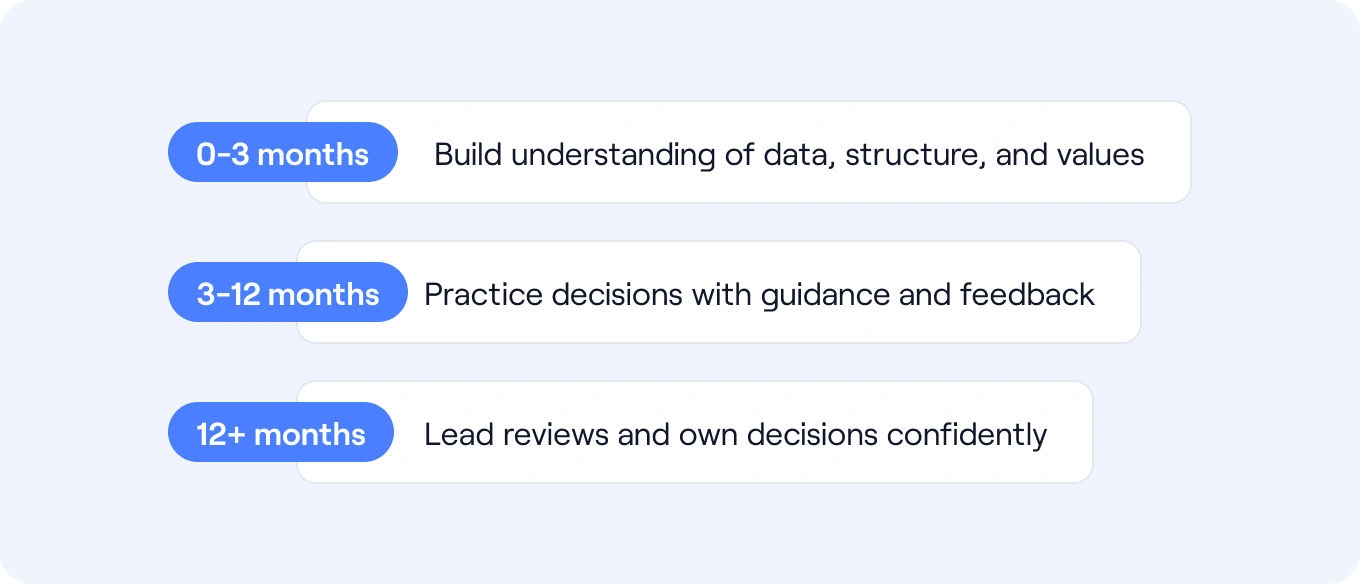

Don't thrust heirs into leadership roles without proper preparation. Build competence gradually:

Months 0-3 (Literacy phase):

Months 3-12 (Participation phase):

Months 12+ (Leadership phase):

This paced approach builds confidence through repeated exposure, rather than relying on them to figure it out under pressure. The goal is to prepare the next generation to handle money matters and understand the financial situation without panic.

Asora's mobile dashboards allow heirs to review information conveniently between formal training sessions.

Make heir preparation part of your regular rhythm:

This brings heirs into processes that should already exist and makes training part of the operating rhythm. The structure serves your current needs while preparing you for future responsibilities.

Use annual exclusion amounts strategically during training years so heirs can learn about lifetime gifts and federal gift tax rules while you're still available to explain the strategy. Understanding lifetime exemption amounts and how to transfer assets tax efficiently becomes practical knowledge rather than abstract concepts.

Focus training on practical skills that heirs will actually use:

Take last year's capital call notices and current liquidity positions. Ask your heir to produce a brief approval memo with supporting evidence linked to their recommendation. This reveals gaps in understanding before real decisions are at stake.

Define mentor roles explicitly. Who explains tax strategy and accounting advice? Who walks through private equity mechanics? Who handles questions about specific asset classes? Who provides legal advice? Your advisor, tax pro, and estate planning advisor each contribute to the overall value in preparing your heirs.

Keep a Q&A log. When heirs ask questions, document both the question and the answer. This helps build institutional memory and identifies knowledge gaps that require attention.

Record decisions with links to supporting evidence. Over time, this creates a reference library showing how similar decisions were made in the past. This is particularly valuable for understanding family values and how they've guided investment choices.

Least privilege keeps access tight: define roles and need-to-know, enforce MFA, require approvals in your external process, and document key decisions in meeting notes and packs. Predictable freshness ensures data trustworthiness: establish clear update cadences (e.g., COB, weekly, monthly), assign owners, monitor staleness with alerts, and utilize simple runbooks to resolve gaps promptly.

Structure access based on roles:

Use least privilege principles: people see only what they need for their role, nothing more. Review permissions periodically as roles evolve.

Require MFA for all users. Security isn’t optional when managing significant family wealth and protecting sensitive information.

Establish timely update policies rather than ad hoc data pulls. Knowing when data refreshes creates predictable routines.

Each reporting period, produce a period change reconciliation showing:

Brief reviewer notes explain significant movements. This creates accountability and makes it obvious when something unexpected occurred, whether it's future appreciation in an asset, unexpected estate tax implications, or capital gains that trigger income tax consequences.

Workflows support task assignments, due dates, and reminders; teams attach evidence to tasks as needed.

The Monday inbox looks different when roles are clear, reports are decision-ready, documents live with numbers, and controls keep cadence steady.

Here's how to start:

The goal isn't perfection. It's the building structure that makes good decisions possible and provides heirs with a framework to work within as they develop their judgment.

Technology helps, but it's not the whole answer. You still need transparent governance, deliberate training, and the discipline to maintain routines. Work with qualified professionals: your advisor for strategy, advisors for tax-smart wealth transfer strategies, and an estate planning attorney for minimizing estate tax liability and structuring transfers properly.

Platforms like Asora provide infrastructure that supports those human processes: connecting data, documents, and workflows so heirs can make informed decisions about the family wealth they'll manage for one generation and pass to the next.

Request a demo to see how our tools help you transfer your wealth to heirs with confidence.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

A. Prepare governing documents (trust agreements, including irrevocable trust agreements), side letters, current valuations with methodologies, tax documents (K-1s and partnership returns), insurance summaries, estate planning documents, and powers of attorney. Link documents to specific entities and assets so heirs can easily reference the correct agreement without searching. Asora stores and links documents to each asset or entity, creating a single, searchable source of truth.

A. Train in three phases: literacy (0–3 months learning dashboards and structures), participation (3–12 months co-reviewing decisions and presenting quarterly sections), and leadership (12+ months running agendas and making decisions). Set a routine with monthly sessions, quarterly deep dives with advisors and tax professionals, and annual off-sites on family values and planning. Use simulations to identify gaps. Asora provides consolidated dashboards and reports, allowing trainees to transition from summary to detail during reviews.

A. Technology consolidates data from multiple sources, organizes documents with links to holdings, tracks private and trust assets, enables mobile access, and supports decision workflows. Asora connects numbers with documents and notes, standardizes reporting across entities, and supports tasking inside your operating cadence, helping heirs make informed, timely decisions.

A. Use explicit decision thresholds that expand with competence, a “no approval without the reports” rule, role-based access, and scheduled reviews. Begin with co-review and mock approvals, then transfer responsibility with clear escalation paths. Hold family meetings to align on values and long-term intent. Asora supports role-based permissions, checklist-driven workflows, and linked materials, ensuring oversight remains strong as responsibilities shift.

.png)

.jpg)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.webp)