.jpg)

TL;DR

This guide examines automated reconciliation software, including automated bank reconciliation software for bank and custody cash accounts, and investment-operations reconciliation across custodians, administrators, and portfolio accounting systems. It focuses on how account reconciliation software and automated bank reconciliation tools compare transactions and balances across bank accounts, custody cash accounts, and internal books across systems to reduce manual effort, minimize human error, and improve financial operations and financial planning.

Why Family Offices Are Adopting Automated Reconciliation Software

Reconciling financial records has always been one of the most time-consuming and operationally sensitive processes inside a family office. Between multiple custodians, banks, administrators, and internal systems, teams must constantly confirm that balances, transactions, and positions align. Historically, this work happened in spreadsheets and email threads.

Automation has changed that dynamic.

Modern automated account reconciliation software can ingest large volumes of financial data, match records automatically, and highlight discrepancies as data refreshes (often batch/intraday/daily depending on source). The goal is not to remove human oversight, but to focus staff attention on the exceptions that actually require expertise.

And the demand for this capability is growing. According to recent finance automation research by McKinsey, 98% of CFOs report investing in automation or digitization initiatives, yet many processes, especially reconciliation, remain only partially automated.

For family offices, the pressure is particularly acute. Asset complexity, multi-entity structures, and cross-border operations create reconciliation challenges, especially for offices with multiple entities, multiple custodians, and mixed public/private assets. But before choosing the best accounting reconciliation software for automation, it’s important to understand what these systems actually do, and what’s beyond their capabilities.

Top Automated Reconciliation Software for Family Offices (2026 Shortlist)

The following vendors represent established reconciliation platforms used in financial services and investment operations; suitability for family offices depends on operating model and data sources. The goal here is not to suggest a universal “best” platform, but to outline where each tool tends to fit within family office environments.

Best for core investment-operations auto-reconciliation

SS&C Advent Recon

Best for: Investment operations teams reconciling custodians vs portfolio accounting systems.

What is being reconciled: Custodian vs portfolio cash, positions, and transactions (and where supported, reference/security master attributes).

Strengths:

- Exception-based reconciliation workflows

- Support for positions, transactions, and trial balances

- Designed for investment operations environments

- Strong integration with SS&C investment systems

System of record: Custodian for legal holdings/cash, portfolio accounting/IBOR for investment reporting, GL for financial statements.

Integrations:

- SS&C Advent Geneva

- Custodians such as BNY Mellon or State Street

- Portfolio accounting platforms

- Data warehouse environments

Implementation effort: High - driven largely by portfolio complexity, asset classes, and the quality of security master data.

SS&C GoRec

Best for: Complex high volume reconciliation environments.

What is being reconciled: Cash, transactions, positions, and asset-class-specific records.

Strengths:

- Flexible reconciliation rules by asset class

- Detailed transparency into break status

- Designed for high-volume reconciliation environments

System of record: Portfolio accounting system or custodian.

Integrations:

- Custodians and prime brokers

- SS&C platforms

- Portfolio accounting systems

Implementation effort: High - complexity typically comes from the number of sources and reconciliation scenarios.

Best for market-grade matching engines

Duco

Best for: Multi-source reconciliation across structured and semi-structured data, onboarding varied file formats and transforming them into structured datasets for matching.

What is being reconciled: Transactions and balances across banks, custodians, and internal systems.

Strengths

- Highly flexible matching rules

- Rapid onboarding of new data sources

- Strong exception workflow management

- Handles multi-source reconciliation scenarios

System of record: Depends on implementation (often internal ledger or operational data platform).

Integrations:

- Banks and custodians

- Data warehouses

- ERP systems

Implementation effort: Medium to High - driven by the number of data sources and rule complexity.

AutoRek

Best for: Financial services firms needing structured reconciliation workflows.

What is being reconciled: Cash transactions, positions, and operational records.

Strengths:

- Built-in exception management workflows

- Scalable reconciliation capabilities

- Controls such as RBAC, approvals, change logs, and evidence retention

System of record: Depends on operational model.

Integrations:

- Banking systems

- ERP platforms

- Market data providers

Implementation effort: Medium - primarily dependent on source connectivity and rule configuration.

Trintech ReconNET

Best for: Finance-close transaction matching (payments, bank, ERP/treasury). Not an investment book reconciliation tool unless documented.

What is being reconciled: Bank, payment, and transaction records.

Strengths:

- High-volume matching engine

- Strong financial close workflows

- Mature reconciliation capabilities

System of record: General ledger.

Integrations:

- ERP systems

- Banking platforms

- Treasury systems

Implementation effort: Medium

FIS Data Integrity Manager (IntelliMatch)

Best for: Large, complex reconciliation environments.

What is being reconciled: Multi-source financial transactions and balances.

Strengths:

- Enterprise-grade matching engine

- Scalable exception management

- Used in large financial institutions

System of record: Often, the internal accounting or operational ledger.

Integrations:

- Banks and custodians

- ERP systems

- trading platforms

Implementation effort: High - driven by scale, integration scope, and rule complexity.

Broader reconciliation platforms (verify fit)

ReconArt

Best for: Mid-sized teams looking for flexible reconciliation automation.

What is being reconciled: Cash/transaction/holdings datasets matched across sources (e.g., bank/custodian/internal files).

Scope note: Verify whether this supports investment book workflows (IBOR-style) or is primarily file/dataset matching with exception management.

Strengths:

- Multi-source reconciliation capabilities

- Cloud-based platform

- Flexible matching logic

System of record: Varies by implementation.

Integrations:

- ERP systems

- Banks

- payment processors

Implementation effort: Medium

Gresham Control (formerly Clareti)

.webp)

Best for: Investment management and capital markets reconciliation environments.

What is being reconciled: Custodian, bank, and internal system records.

Strengths:

- Strong exception management workflows

- Scalable reconciliation engine

- Investment management variant available

System of record: Varies depending on implementation.

Integrations

- Custodians

- Banks

- Trading systems

Implementation effort: High

What automated reconciliation software actually does (and what It doesn’t)

The term “reconciliation” means different things depending on which team you ask.

In a family office, it usually refers to two distinct operational processes that often live in different departments.

At a high level, reconciliation exists to answer a simple question: do our records match the records held by custodians/banks/admins and the internal books we use for reporting?

In practice, answering that question requires comparing multiple systems that were never designed to work together. Custodians maintain their own books, portfolio accounting systems maintain another, and the finance team maintains a separate general ledger. Reconciling these records ensures that the organization’s internal view of its financial position is consistent with external institutions and administrators.

Because these reconciliations serve different purposes, they are usually owned by different teams.

Finance close reconciliations

Finance and accounting teams typically own reconciliations tied to the financial close and general ledger accuracy.

These processes ensure that financial statements reflect the correct balances and that internal accounting controls are functioning properly.

These often include:

- Bank-to-GL cash reconciliations

- Subledger-to-GL comparisons (AP, AR, expenses, tax)

- Intercompany balances, such as due-to/due-from accounts

- Clearing accounts and suspense items

In this environment, the general ledger or ERP system is usually the system of record, forming the foundation of the family office’s accounting and financial management infrastructure. Automated bank reconciliation software compares the ledger’s view of transactions and balances against bank statements or subledger activity to confirm that everything aligns. This is distinct from investment ops reconciliations, where the authoritative record is often the custodian/administrator and the internal investment book.

Breaks often occur because of timing differences, incomplete postings, or misclassified transactions. For example, a wire recorded in the bank may not yet appear in the ledger, or a transaction may have been posted to the wrong account during the close process.

While these discrepancies are often operational rather than financial errors, identifying and resolving them is essential for maintaining reliable financial reporting.

Investment reconciliations

Investment operations teams focus on a different kind of reconciliation: ensuring the portfolio records match the records held by custodians and administrators.

This process protects the integrity of the investment book and ensures that portfolio and consolidated reporting reflect actual holdings.

Typical reconciliations include:

- Custodian vs portfolio accounting system positions and transactions

- Corporate actions, income postings, FX movements, fees,withholding tax and accrual conventions, and trade lifecycle/settlement status

- Capital calls, distributions, and statements for alternative investments

In these cases, the system of record may be the custodian, portfolio accounting platform, or investment book, depending on the operating model of the family office.

Investment reconciliations are often more complex than finance close reconciliations because asset data flows through multiple intermediaries. Corporate actions may be interpreted differently across systems, administrators may report capital activity at different times, and valuation data may arrive on different schedules.

For family offices with meaningful allocations to private equity, venture capital, real estate, or hedge funds, the reconciliation process frequently includes comparing administrator reports, custodian cash activity, and internal tracking models to confirm that capital activity is recorded correctly.

Because of these complexities, investment operations teams often rely on specialized automated account reconciliation tools designed for multi-source matching rather than standard accounting reconciliation software.

What “automation” actually means

Despite marketing claims, automated reconciliation software rarely eliminates human oversight.

Instead, automation focuses on removing the repetitive mechanics of comparing records across systems.

Most reconciliation automation tools operate through three core components.

-

Data ingestion and normalization: data arrives from banks, custodians, administrators, and internal systems via APIs or scheduled SFTP feeds (manual file uploads are possible, but they reduce automation unless formats and refresh cadence are standardized).

-

Matching rules: transactions are matched based on deterministic rules such as amount, date, identifier, security, currency, or entity.

-

Exception queues: records that fail to match are placed into workflow queues where humans review, annotate, and resolve discrepancies.

The intention isn’t to remove human judgment, but to surface only the transactions that actually require investigation.

In practice, automated reconciliation tools can automatically resolve the majority of records before human review. According to KPI Depot, many finance teams report automation rates exceeding 80%, with some implementations achieving 90% or higher depending on data quality and rule configuration, leaving a much smaller subset of exceptions for manual investigation.

However, some situations will always require expertise. Non-deterministic cases often include:

- Corporate actions interpretation

- Complex alternative cash flows

- Settlement timing differences between systems

- Multi-currency pricing discrepancies

These situations require subject-matter review because they involve judgment rather than simple record comparison.

What it doesn’t solve

Even the most advanced automated reconciliation platform cannot fix structural data problems.

Reconciliation systems compare records—they do not automatically correct the upstream logic that produced those records.

Common challenges include:

- Inconsistent identifiers for securities, entities, or accounts

- Poor ownership mapping across holding companies and trusts

- Valuation timing differences between systems

- Multiple “books” of record (tax vs management vs custody)

For example, if two systems use different security identifiers for the same investment, automated reconciliation tools cannot reliably match those records without a properly maintained security master.

Similarly, if ownership structures are unclear, such as when beneficial ownership differs from legal ownership, the reconciliation system may correctly identify discrepancies without being able to determine which record is actually correct.

In those situations, reconciliation automation surfaces the operational complexity that already exists. Automation improves matching. It does not automatically create data integrity.

Who benefits most (and who gets burned)

In the right operating environment, bank reconciliation automation software can dramatically improve efficiency and control. In the wrong environment, it can become another layer of operational complexity.

The difference usually has less to do with the software itself and more to do with the operational foundations already in place. Reconciliation automation works best when the organization has consistent data pipelines, well-defined ownership of operational processes, and a clear understanding of which system serves as the authoritative record.

Without those foundations, automation tends to expose existing data and governance issues rather than resolve them.

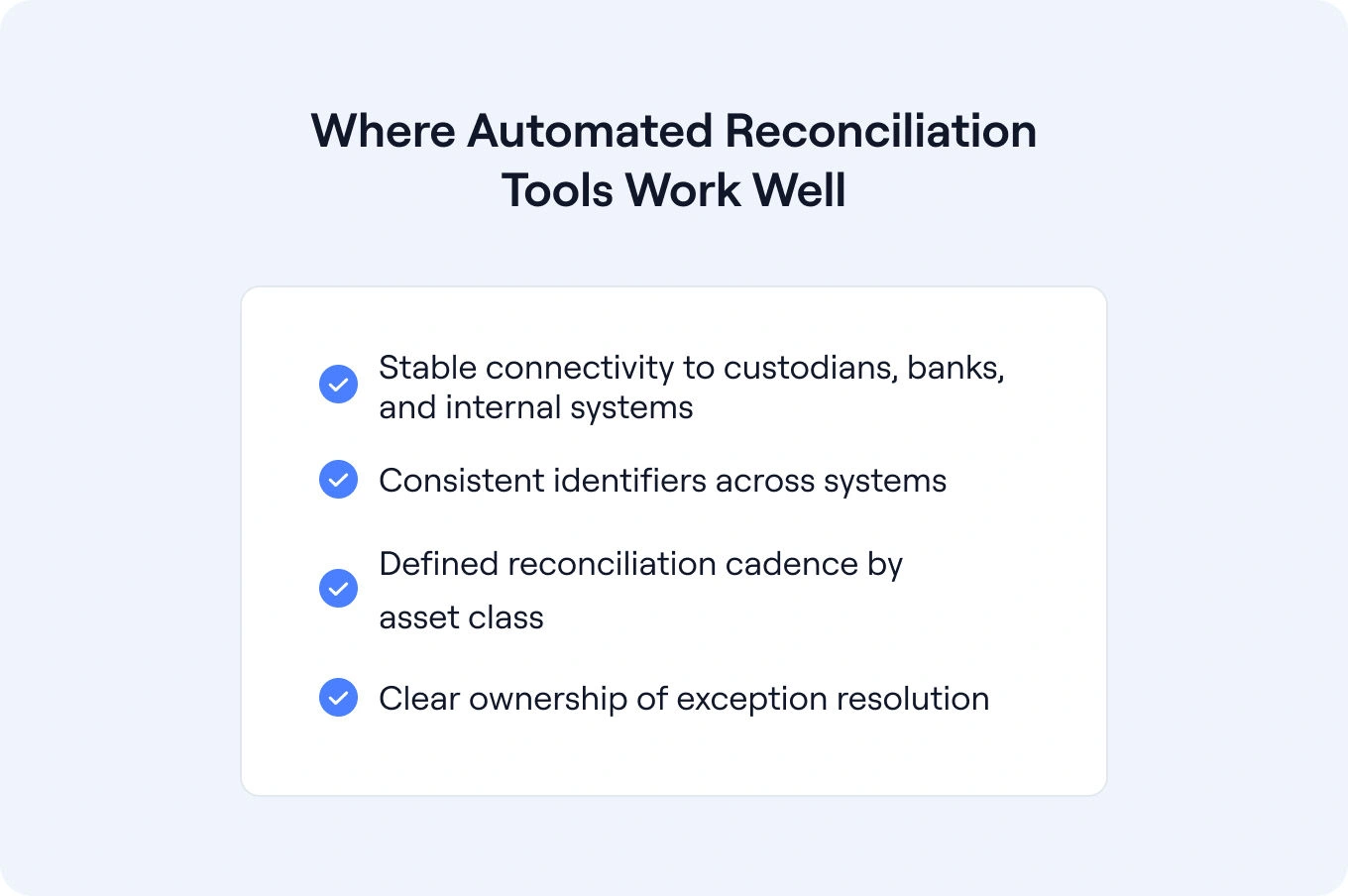

Where automated reconciliation tools work well

Automation tends to perform best when organizations already have structured data pipelines and clear operational ownership.

Successful implementations usually include:

- Stable connectivity to custodians, banks, and internal systems

Automated reconciliation tools rely on predictable, repeatable data feeds. When transaction and position data arrives through consistent APIs, file feeds, or administrator reports, matching rules can operate reliably.

- Consistent identifiers across systems

Accounts, securities, entities, and counterparties need standardized identifiers. A well-maintained security master or account mapping layer allows reconciliation rules to match records without constant manual intervention.

-

Defined reconciliation cadence by asset class Different asset classes naturally follow different reporting cycles. For example, daily cash reconciliation may occur alongside monthly financial closes and quarterly updates for private investments. Automation performs best when these cadences are clearly defined and predictable.

-

Clear ownership of exception resolution Automated reconciliation platforms surface breaks, but they do not decide how those breaks are resolved. Successful organizations define which team investigates discrepancies, how issues are escalated, and who ultimately signs off on adjustments.

When these operational foundations exist, automated bank reconciliation tools can eliminate a significant portion of manual comparison work. Teams spend less time verifying routine matches and more time focusing on the relatively small set of transactions that require investigation.

Over time, this shift can also strengthen governance. Exception workflows create clearer audit trails, and recurring breaks become easier to identify and address at the root cause.

Where organizations get burned

Automation struggles when operational complexity is not mapped clearly.

In many family offices, financial data flows through a mixture of custodians, fund administrators, accounting systems, and internally maintained spreadsheets; a common set of issues is explored in family office data aggregation and reporting challenges. When these systems use different identifiers, reporting conventions, or timing assumptions, reconciliation tools cannot easily determine which records should match.

Some of the most common failure points include:

-

Look-through ownership structures where legal ownership differs from beneficial ownership. For example, a trust may hold an investment through a holding company, while internal reporting tracks exposure at the beneficiary level. Without clear mapping between those layers, automated matching becomes difficult.

-

Inter-entity transfers and internal cash movements that are poorly documented. Family offices frequently move capital between entities for liquidity management, tax planning, or investment allocation. If those movements are not consistently recorded across systems, reconciliation tools will flag persistent breaks.

-

Multiple currencies and accounting bases across systems. Some platforms track transactions in local currency, others in base currency, and still others in tax or management accounting formats. Even small differences in FX treatment can generate recurring reconciliation discrepancies.

-

Parallel valuations and timing mismatches, such as daily market pricing versus month-end valuations for private assets. These timing differences are common in mixed portfolios that include both public and private investments.

-

Unstructured alternative investment data often arrives in PDFs or email statements rather than structured feeds. Capital calls, distributions, and fee allocations may need to be manually interpreted before they can be reconciled.

-

Lack of ownership for exception resolution. When breaks are passed between accounting teams, investment operations, and external administrators without a clear decision-maker, reconciliation issues can persist for multiple reporting cycles.

In these situations, reconciliation automation does not eliminate complexity; it surfaces it more clearly.

Transactions that previously sat unnoticed in spreadsheets now appear in exception queues with explicit discrepancies. This visibility is valuable because it highlights where operational processes need improvement.

However, it can also feel uncomfortable for organizations that have historically relied on informal reconciliation processes.

In practice, many family offices find that implementing automated reconciliation tools is not just a technology project. It often becomes an operational governance exercise, forcing teams to clarify data ownership, reporting standards, and escalation procedures across finance and investment operations.

Feature checklist: what to demand

When evaluating the best accounting software with reconciliation automation features, buyers should look beyond matching algorithms. Operational governance and data transparency matter just as much as automation.

The real value of reconciliation automation software comes from how well it supports governance, investigation workflows, and operational transparency. In family office environments, where multiple entities, custodians, and administrators interact, these features often matter more than the matching engine itself.

Below are the core capabilities worth validating during vendor evaluation.

| Feature | Why it matters | | --- | --- | | Multi-entity support | Family offices often manage dozens of legal entities and investment vehicles. | | Controls and evidence | Audit trails, approvals, and documentation are critical for governance and audits/internal reviews (and regulatory exams where applicable, e.g., regulated advisory entities). | | Exception workflow | Breaks must have owners, notes, attachments, and aging visibility. Decision + write-back: who approves and who posts adjustments to GL/IBOR/admin records. | | RACI structure | Clear assignment of investigation, approval, and adjustment responsibilities. | | Role-based access | Limits who can change rules or approve reconciliations. | | Identifier mapping | Ensures securities, accounts, and entities match across systems. | | Reporting and analytics | Identifies recurring breaks and operational trends. |

Multi-entity support

Family offices rarely operate through a single legal entity. Trust structures, holding companies, operating entities, and investment vehicles can all appear within the same reporting environment.

A strong automated reconciliation platform should support hierarchical entity structures and allow reconciliation rules to operate across multiple entities, accounts, and custodians. Without this capability, teams often end up running separate reconciliations for each entity, which defeats much of the efficiency automation is meant to deliver.

Controls, approvals, and evidence

Reconciliation is not just about confirming balances; it is also a key internal control.

Platforms should provide configurable approvals, detailed change logs, and clear sign-off workflows. Ideally, the system should also allow teams to attach supporting documents or commentary explaining how a break was resolved.

These records become particularly important during audits or internal reviews, when organizations need to demonstrate not only that reconciliations were performed, but also how discrepancies were investigated and resolved.

Exception management workflows

Even the most advanced automated account reconciliation tools will generate exceptions. The difference between useful automation and operational frustration often comes down to how those exceptions are handled.

Effective reconciliation automation tools provide structured exception queues where breaks can be assigned, annotated, escalated, and tracked over time. Teams should be able to see which discrepancies remain unresolved, how long they have been open, and who is responsible for resolving them.

Without this level of workflow management, reconciliation exceptions often drift back into email chains or spreadsheet trackers.

Clear operational roles (RACI)

Automation works best when operational responsibilities are clearly defined.

A reconciliation system should support a simple RACI model, identifying who investigates discrepancies, who approves resolutions, who posts adjustments, and how issues escalate if they remain unresolved.

In many family offices, reconciliation breaks involve multiple stakeholders including accounting teams, investment operations, and external administrators. Explicit role definitions help prevent issues from bouncing between teams without resolution.

Role-based access controls

Because reconciliation platforms interact with financial records and operational rules, access control is critical. Handling sensitive financial data across systems also raises broader operational security considerations for family offices.

The system should allow administrators to define which users can modify matching rules, approve reconciliations, or adjust records. Role-based permissions help maintain segregation of duties where the team size allows, and reduce the risk of unauthorized changes to reconciliation logic.

For organizations with external service providers or administrators, access controls also ensure that each party sees only the data relevant to their responsibilities.

Identifier and mapping management

One of the most common causes of reconciliation breaks is inconsistent identifiers across systems.

Custodians, portfolio accounting platforms, and internal ledgers may use different identifiers for the same security, account, or entity. A robust reconciliation automation platform should provide tools for maintaining these mappings and normalizing identifiers across sources.

This capability is especially important in family offices that manage a mix of public securities, private investments, and direct holdings.

Reporting and break analytics

Finally, reconciliation automation software should provide meaningful reporting on reconciliation outcomes.

Operational teams should be able to track metrics such as break frequency, unresolved exceptions, and reconciliation completion status across entities, custodians, and accounts.

Over time, these insights help organizations identify recurring operational issues, such as data feed inconsistencies or pricing source mismatches, and address them at the root cause.

A reconciliation automation platform should not only match transactions. It should provide visibility into where discrepancies occur, how they are resolved, and how operational processes can improve over time.

Implementation realities (timeline, internal owner, testing)

Even the best automated reconciliation platform requires operational discipline to implement successfully. Simple use cases can be deployed relatively quickly.

- 30–90 days for a single-entity finance-close scenario with clean data feeds

- 3–6+ months for multi-entity environments with multiple custodians and alternative investments. Alts-heavy environments with statement-based processes can extend beyond 6 months unless upstream data capture is addressed.

Implementation complexity is driven less by the software itself and more by the surrounding operational environment. Typical implementation phases include:

- Discovery and data source inventory

- Identifier mapping and normalization

- Matching rule configuration

- User acceptance testing using real close periods

- Parallel runs over multiple reporting cycles

- Cutover and governance setup

Organizations should also designate several internal roles before implementation begins:

- Internal owner (Controller, Head of Finance, or Investment Operations lead)

- Data source owners

- Rule approval authority

Without clear ownership, even the most sophisticated automated reconciliation tools will struggle to deliver reliable outcomes.

When you don’t actually need auto-recon yet

Automation is not always the right first step. In many family offices, reconciliation problems stem less from the absence of automated reconciliation software and more from fragmented data sources, inconsistent identifiers, or unclear ownership of operational processes. When those issues exist, reconciliation automation tools often surface more discrepancies rather than reducing them.

Before implementing an automated reconciliation platform, it helps to evaluate whether your operating environment is actually ready for rule-based matching. A simple readiness scorecard can help determine whether automation will reduce manual work, or simply generate more exception queues.

A quick readiness framework

Start by evaluating five operational factors:

-

Volume (transactions and positions): automation delivers the most value when reconciliation involves large transaction volumes or many securities across multiple accounts. If your environment includes only a few accounts with relatively low activity, manual reconciliation may still be manageable.

-

Complexity (entities, intercompany activity, alternatives cadence): multi-entity structures, internal capital movements, and alternative investments add significant reconciliation complexity. Automation works best when entity hierarchies and ownership structures are clearly mapped across systems.

-

Fragmentation of incoming data: if most financial data arrives through APIs, SFTP feeds, or standardized files, reconciliation automation tools can apply matching rules effectively. But when key inputs still arrive through PDFs, spreadsheets, or ad hoc administrator reports, automated matching becomes much harder.

-

Number of banks and custodians: automation becomes more valuable as the number of external financial institutions grows. Multiple custodians and private banks increase the number of data feeds and reconciliation points across the organization.

-

Break frequency and repeatability: automation is most effective when reconciliation discrepancies follow predictable patterns, such as timing differences or small FX variations. If every reporting cycle produces entirely new breaks, the underlying issue is often inconsistent data rather than a lack of matching technology.

Interpreting the results

There are no universal thresholds for when automation becomes necessary. The right timing depends on your environment: how many entities you manage, the number of custodians involved, the asset mix, and the cadence of financial reporting.

As a general guideline, automation becomes more compelling when reconciliation involves multiple entities, several custodians, structured data feeds, and recurring reconciliation breaks that follow consistent patterns.

If your environment falls below those thresholds, or if most data still arrives through manual formats, the better investment may be fixing upstream data processes first.

Once data sources are centralized, identifiers are standardized, and ownership of reconciliation breaks is clearly defined, automated reconciliation software can deliver far greater efficiency and reliability.

If your upstream problem is fragmented data and unclear ownership

Many reconciliation problems originate long before matching rules are applied. When data arrives from multiple sources with inconsistent identifiers and unclear ownership structures, automated reconciliation platforms struggle to produce reliable matches.

Before implementing reconciliation automation software, family offices often need to address three upstream challenges:

- Centralizing financial data sources

- Standardizing identifiers and entity mappings

- Establishing clear ownership for exception resolution

This is where operational platforms such as Asora play a role. Asora helps family offices:

- Create a single source of truth for financial data aggregation

- Centralize documents and structured data via supported ingestion methods (APIs/SFTP/files)

- Maintain consistent identifiers and entity mappings

- Assign ownership for follow-ups and operational workflows

Asora is not an automated reconciliation software solution. Asora does not perform matching-based reconciliation; it supports upstream data organization and operational workflows that can reduce preventable breaks.

By improving data quality and operational visibility, family offices can dramatically reduce reconciliation complexity before implementing reconciliation automation tools.

Final thoughts: Buyer’s next steps

For teams evaluating the best software for automated account reconciliation, vendor demos should focus on real operational scenarios rather than polished sales examples. During vendor evaluation, include questions such as:

- How does the system ingest and refresh data from custodians and banks?

- How are matching rules configured and governed?

- What exception management workflows exist?

- Can users trace a transaction from source data to final resolution?

- How are pricing sources, FX handling, and corporate actions managed?

- What security standards are supported (SOC 2 Type II, ISO 27001, SSO, RBAC)?

When running a pilot, always test with real entities and real messy data, not sanitized demo files. Red flags during evaluation include:

- Black-box matching logic

- Weak exception workflows

- Limited audit trails

- Unclear implementation methodology

A strong automated reconciliation platform should be able to demonstrate, within minutes, how it ingests multiple sources, matches records, surfaces breaks, and documents resolution.

If your priority is reducing reconciliation breaks by improving upstream data organization first, Asora can help. Request a demo to see how Asora supports data aggregation, standardized identifiers, and operational workflows that make reconciliation processes more reliable.

FAQ

What should be the system of record for reconciliation software (custodian vs GL vs portfolio accounting)?

The system of record depends on the specific financial processes being reconciled. For bank reconciliations, the GL is authoritative for financial statements; the bank is the external statement of record for cash accounts (and the custodian/prime broker is the external record for custody cash accounts). Portfolio accounting systems typically act as the investment book for positions and performance, so reconciliation software must support transaction matching across all three to maintain accurate financial records and ensure financial oversight.

How do alternative investments and delayed NAVs affect automated reconciliation?

Alternative investments introduce timing challenges that can complicate the account reconciliation process. Capital calls, distributions, and fees may appear in bank transactions before administrators publish updated valuations, meaning reconciliation software must reconcile bank statements, financial records, and internal investment tracking while waiting for official NAV updates. This often increases the number of reconciliation breaks temporarily, which is why modern reconciliation tools focus on strong exception workflows, audit trails, and structured reconciliation reports to help finance teams manage complex financial processes.

What is a realistic implementation timeline for automated reconciliation software?

For a simple environment, such as one entity reconciling a few bank accounts and balance sheet accounts, modern bank reconciliation software can often be implemented in 30–90 days once existing financial data and bank statements are available. However, environments with multiple entities, high transaction volumes, credit card accounts, and several custodians typically require more configuration of transaction matching rules, integrations with financial systems, and testing of reconciliation tasks, which can extend implementation timelines. The right reconciliation software should provide strong automation capabilities, audit trails, and a clear implementation plan so finance teams can reduce manual effort, improve financial accuracy, and streamline reconciliation.

What data do I need to provide to get value from automated reconciliation software in the first 30 days?

To see early value from account reconciliation software, organizations typically need access to bank statements, bank transactions, and core financial records from their general ledger or accounting platform. Providing structured feeds for multiple bank accounts, accounts payable, accounts receivable, and credit card accounts allows bank reconciliation software to begin automated transaction matching and generate initial reconciliation reports quickly. When finance teams can connect these sources with minimal manual data entry, the reconciliation solution can reduce time-consuming manual reconciliations, improve financial health, and deliver timely financial insights with strong audit trails.

.png)