.jpg)

TL;DR

Family office portfolio management requires codified policy, disciplined processes, and a single source of truth for data. Successful SFOs establish clear investment policies, translate them into strategic asset allocation, manage liquidity across multiple entities, track private investments systematically, and produce reporting for different audiences.

Managing a Family Office Investment Portfolio

Managing a family office investment portfolio is different from running an institutional portfolio. The role extends beyond tracking returns; it involves stewardship of family wealth across generations, balancing liquidity needs with long-term growth, coordinating across multiple entities, and serving stakeholders with diverse objectives and risk tolerances.

Lean single family offices with 5 to 50 entities face a clear challenge: institutional-grade oversight without institutional-scale resources.

Practices must be rigorous without being bureaucratic and comprehensive without being overwhelming.

Below are 15 best practices for family office portfolio management, from investment policy to reporting, designed to create trustworthy, repeatable oversight that works whether the portfolio is $100 million or $ 1 billion+.

What Family Office Portfolio Management Means

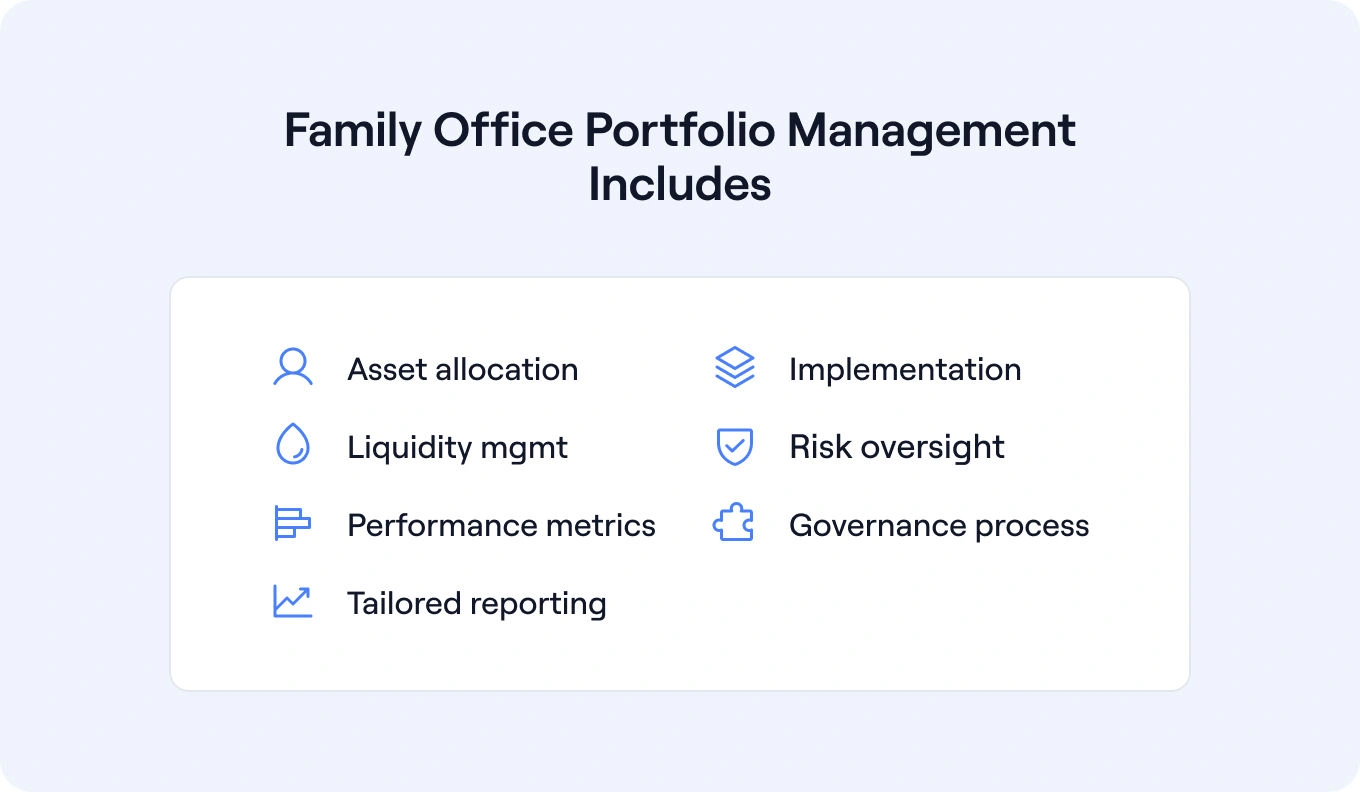

Family office portfolio management encompasses the full cycle of managing family wealth, including setting policy, implementing asset class allocations, monitoring risk and liquidity, measuring performance, maintaining governance, and producing family office portfolio reports that serve various audiences.

This includes:

- Asset allocation: Strategic targets and tactical ranges across public equities, fixed income, alternative investments, private equity, venture capital, real estate, and other holdings.

- Implementation: Manager selection, direct investments, co-investments, and execution across both liquid and illiquid assets.

- Liquidity management: Cash positioning, capital calls pacing, FX exposure, and coordination across banks and currencies.

- Risk oversight: Concentration monitoring, scenario analysis, downside protection, and understanding how market volatility affects the entire portfolio.

- Performance measurement: Time-weighted returns (TWR) for liquid holdings, internal rate of return (IRR) for private investments, and consolidated family office portfolio analytics.

- Governance: Investment committees, decision frameworks, approval processes, and documentation that creates institutional memory.

- Reporting: Family office portfolio reports tailored for principals, beneficiaries, investment committees, and external advisors.

What it's not: Family office portfolio management isn't investment research (that's what managers and advisors provide), tax advice (your tax professionals handle that), or general ledger accounting (though it informs your GL). It's the operational discipline of translating investment decisions into executed positions and trackable outcomes.

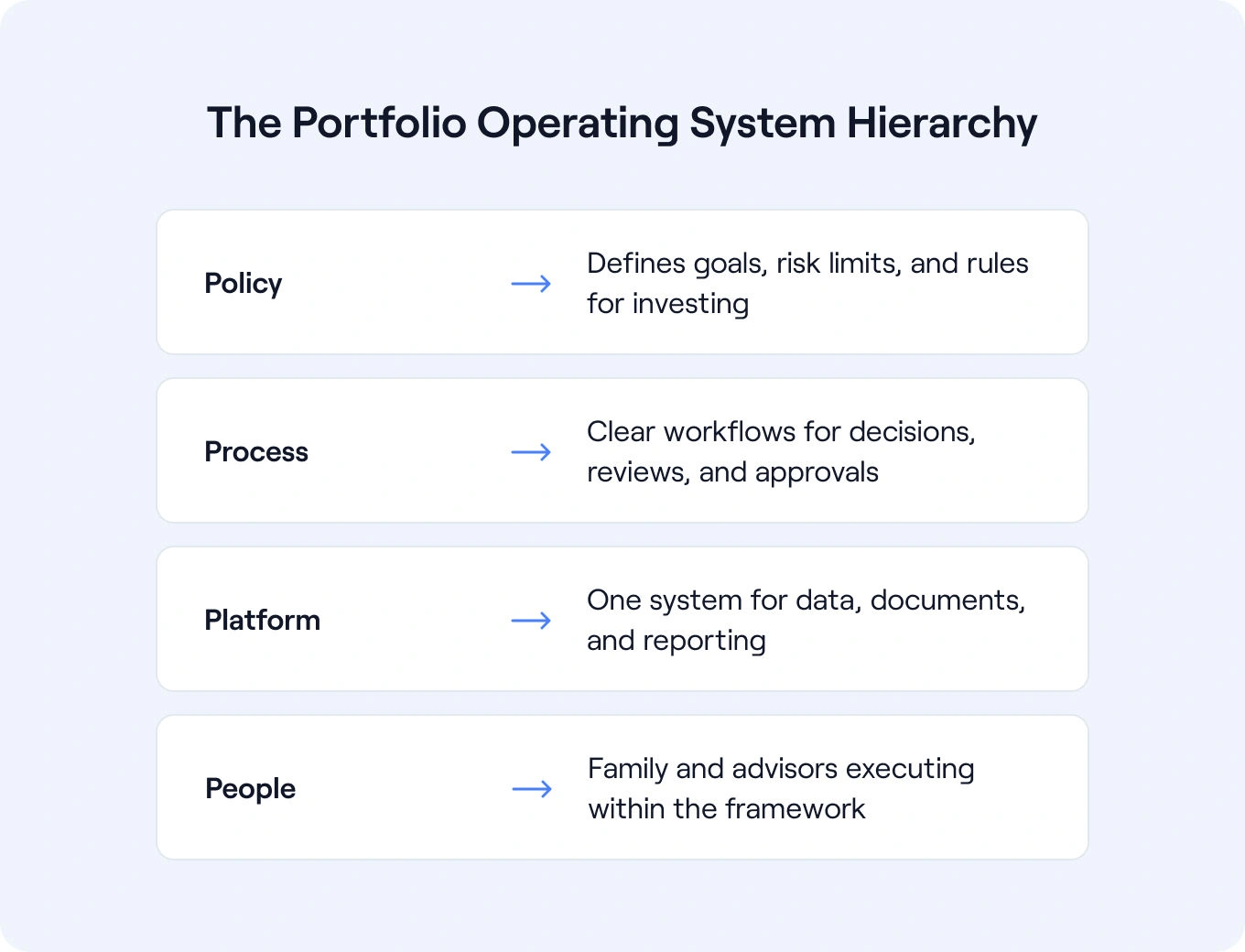

The Portfolio Operating System

Effective wealth management follows a clear hierarchy:

Policy → Process → Platform → People

- Policy: Your Investment Policy Statement (IPS) codifies the family's objectives, risk tolerance, spending needs, and guardrails. It's the constitution for investment decisions.

- Process: Documented workflows for how decisions get made—manager selection, rebalancing triggers, approval thresholds, performance reviews, and reporting cadence.

- Platform: The technology that consolidates portfolio data, links documents to holdings, tracks workflows, and enables reporting. For lean single family offices, this needs to work without a large IT team.

- People: Family members, chief investment officers or investment leads, advisors, venture capital firms, and managers who execute within the framework outlined above.

Problems usually start when families skip steps. They hire great managers (people) without a clear process. They implement sophisticated platforms without a documented policy in place. The result is complexity without clarity.

15 Best Practices for Modern SFOs

Each practice below includes its rationale and instructions for application. Together, they form a complete framework for investment management.

1. Codify an Investment Policy Statement (IPS) That Reflects the Family Enterprise Balance Sheet

The IPS is your decision framework. It defines objectives (capital preservation, capital appreciation, or both), spending requirements, liquidity needs, risk tolerance, concentration limits, and what's permissible versus prohibited. Without a written IPS, every decision becomes a negotiation rather than following established guidelines.

How to apply:

- Document the family's long-term goals and time horizon (often multi-generational)

- Specify spending requirements and cash flow requirements

- Set concentration limits by asset class, manager, geography, and security

- Define currency exposure guidelines if significant wealth is held in multiple currencies

- Establish rebalancing triggers and escalation rules

- Review annually and update when family circumstances change

The IPS should reflect how the family thinks about wealth—whether it's primarily for capital preservation to pass to future generations, growth to fund a family foundation or impact investing initiatives, or a balance of both investment objectives.

2. Translate IPS into a Living Strategic & Tactical Asset Allocation

Your IPS sets direction; asset allocation is the roadmap. Strategic allocation defines long-term targets across asset classes. Tactical allocation sets ranges allowing for market opportunities and drift without triggering rebalancing.

How to apply:

- Establish strategic targets for public equities, fixed income, private foundations, alternatives, private equity, venture capital, real estate, and cash

- Define tactical ranges (drift bands) around each target—typically ±3-5% for liquid assets, wider for illiquid

- Assign responsibility for monitoring drift and proposing rebalances for wealth preservation

- Set escalation rules: who approves rebalances, what documentation is required, and what timeline for remediation when bands are breached

- Review allocation quarterly against targets and annually for strategic changes

Many families struggle with classifying alternative assets. Be explicit about whether hedge funds, private credit, and non-bankable assets are considered alternatives or receive their own allocation buckets.

3. Right-Size Liquidity & Cash Management

Poor liquidity management creates crisis decision-making. When you don't know cash positions across entities and haven't modeled upcoming capital calls, you're forced to sell positions at bad times or pass on good opportunities.

How to apply:

- Maintain visibility into cash balances across all banks, entities, and currencies

- Build a 12-month forward calendar of expected capital calls, distributions, spending, and tax obligations

- Establish minimum liquidity buffers as a percentage of committed but unfunded private investments

- Use cash laddering for near-term liquidity needs

- Set up sweep arrangements or automate transfers between operating and investment accounts where appropriate

- Model scenarios: what if all committed capital gets called simultaneously? What's your stress liquidity position?

For family offices managing substantial wealth across multiple jurisdictions, FX exposure adds another layer. Understand your natural currency exposure and determine whether hedging is sensible given the family's primary spending currency.

4. Build a Private Assets Playbook

Private equity, venture capital, credit, and direct investments significantly contribute to the complexity in family office portfolio management. These illiquid assets require different diligence, pacing, tracking, and reporting than liquid holdings.

How to apply:

- Document your diligence process: what information is required before committing, who reviews, and what approval threshold applies

- Establish pacing models: determine the percentage of private equity in the total portfolio and the annual commitment required to maintain target exposure.

- Track unfunded commitments systematically. These are obligations that affect your actual liquidity.

- Build call forecasting based on fund vintage, strategy, and historical pacing.

- Maintain a look-through exposure analysis: What underlying sectors, geographies, and companies are represented within your fund investments?

- Keep all LP agreements, side letters, K-1s, and capital account statements linked to the specific investment.

Private assets tracking becomes critical infrastructure for families with significant allocations to alternatives, enabling systematic oversight of commitments, calls, and performance.

5. Standardize Manager & Deal Selection

Consistent evaluation frameworks lead to better decisions and foster institutional memory. When every investment gets assessed differently, you can't compare opportunities effectively or learn from past decisions.

How to apply:

- Create scoring frameworks for manager evaluation: track record, process, terms, alignment, operational quality, and cultural fit

- Require standard information from all managers, including strategy documents, fee schedules, track records with attribution, and risk management approaches.

- Document decision rationale in investment committee memos: why this manager, why now, what alternatives were considered

- Maintain a pipeline of evaluated managers so when you're ready to commit, you're not starting from scratch.

- Build relationships with proven managers early, even before you're ready to commit capital.

For direct investments and co-investments, diligence requirements are even more extensive. Establish minimum standards that you won't compromise on, regardless of the opportunity timeline or pressure.

6. Pipeline & Governance for Directs/Co-Invests

Direct investments and co-investments offer better economics but require more oversight and management. Without clear stage gates, family education, and family governance, these can become sources of concentrated risk or distract from core portfolio management.

How to apply:

- Establish stage gates: initial screening, preliminary diligence, full diligence, approval, execution, and post-close monitoring

- Require written investment memos at each gate documenting thesis, risks, valuation, and recommendation

- Define approval thresholds: what size investments require full IC review versus officer approval

- Track post-close obligations: board seats, reporting requirements, follow-on rights, exit timelines

- Maintain a deal flow log showing what was reviewed, why it passed, and lessons learned

Workflows that link tasks to specific investments help ensure nothing falls through the cracks, from diligence deadlines to post-investment monitoring obligations.

7. Consolidated Data with Document Linking

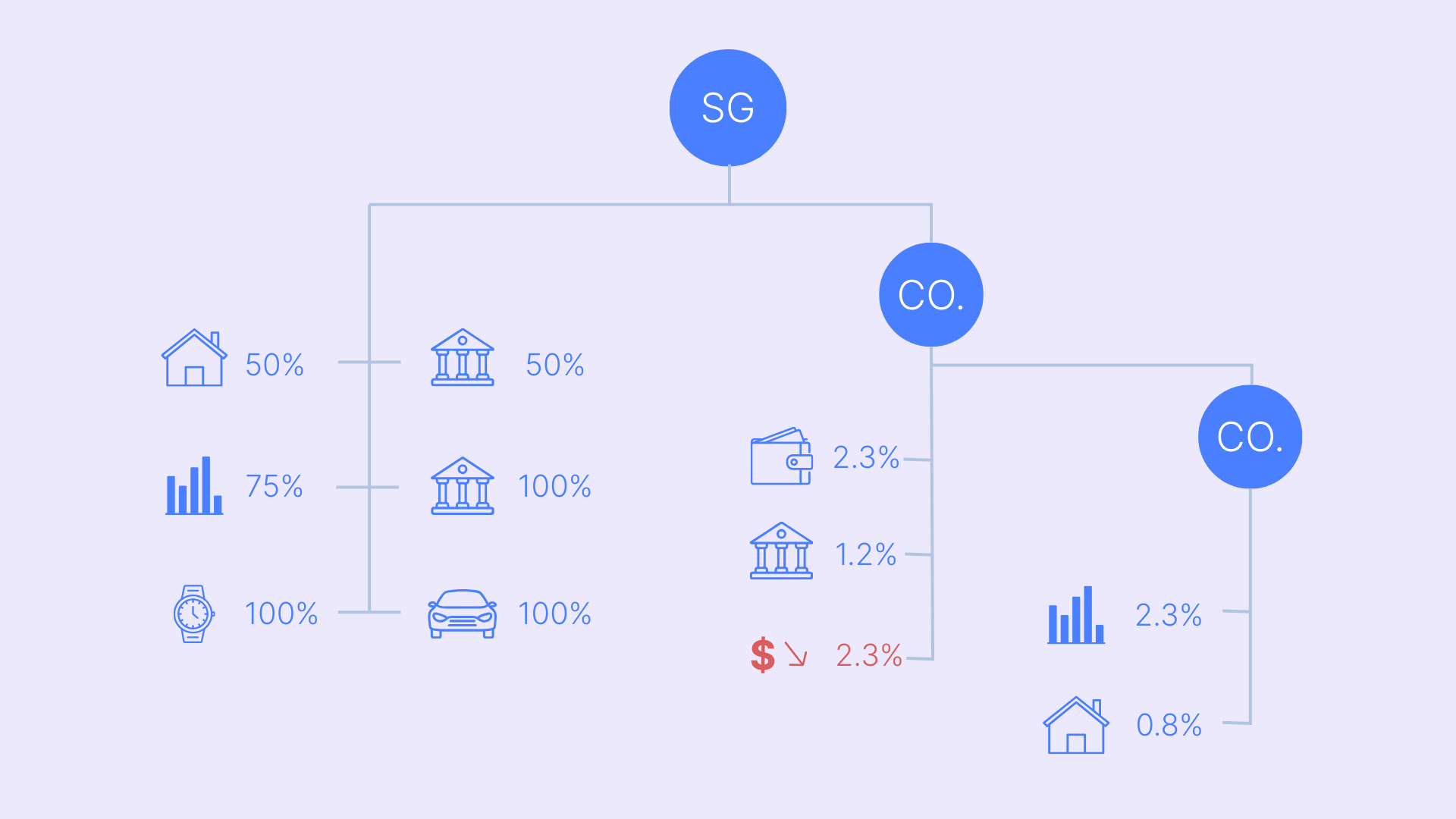

You can't manage what you can't see. Family office investment portfolios encompass dozens of accounts across multiple custodians, as well as private investments tracked outside of custodian systems. Fragmented data creates blind spots and reporting delays.

How to apply:

- Build one deduplicated holdings register with unique identifiers across all entities, accounts, and vehicles-

- Connect to custodians via data aggregation feeds for automated position and transaction updates-

- Manually input private holdings in a standardized format with commitment amounts, funded capital, valuation dates, and performance.

- Link all supporting documents to holdings: LP agreements, subscription documents, side letters, valuations, appraisals, loan documents, and capital account statements.

- Maintain audit trail: who entered data, when, and based on what source document.

- Reconcile custodian data against statements monthly; flag discrepancies for resolutio.n

The goal is a single source of truth where anyone with appropriate permissions can answer: What do we own? What's it worth? Where's the supporting documentation?

Document management that links files directly to holdings eliminates the need to search through folders when the investment committee requests backup details.

8. Performance Measurement That Fits Families (TWR & IRR)

Institutional investors focus on time-weighted returns to evaluate a manager's skill independently of cash flows. Family offices need both TWR and IRR—TWR for liquid family portfolios, IRR for private investments where timing and magnitude of cash flows matter.

How to apply:

- Calculate TWR for liquid holdings using daily or monthly returns

- Calculate IRR for each private investment, incorporating all cash flows: commitments, calls, distributions, and current NAV.

- Close performance periods consistently, monthly for liquidity, quarterly for the whole portfolio

- Reconcile cash flows before finalizing performance: ensure all contributions, withdrawals, fees, and expenses are captured.

- Report performance at multiple levels: total portfolio, by asset class, by investment manager, by entity for families with complex structures

- Unitize where needed: if multiple family members own interests in pooled structures, calculate unit values for transparent allocation of ownership.

Performance monitoring systems purpose-built for family offices handle both methodologies without requiring multiple platforms.

9. NAV & Valuation Hygiene for Private Assets

Private asset valuations drive your reported net worth and inform allocation decisions. Sloppy valuation processes can create the illusion of precision and lead to poor decisions.

How to apply:

- Establish valuation frequency: most LP investments update quarterly based on fund NAV, direct holdings may need independent appraisals annually

- Build roll-forwards between formal valuations: start with last NAV, add calls, subtract distributions, adjust for known value changes.

- Accrue fees and carry them appropriately: preferred return accruals, management fees, and performance allocations impact the actual net value.

- Handle FX consistently: select a base currency, apply rates at regular intervals, and document the methodology.

- Archive all working papers: valuation reports, appraisal letters, board-approved valuations, and roll-forward calculations.

- Clearly disclose valuation dates in reports: a portfolio NAV is only as current as its oldest valuation date.

For families managing substantial investments across multiple private equity firms and venture capital funds, valuation timing mismatches create reporting complications. Standardize your approach and be transparent about staleness.

10. Risk That Families Feel: Concentration, Liquidity, FX, and Covenant Risk

Academic risk models often fail to resonate with family office clients. Families understand concentration risk (too much in one manager or sector), liquidity risk (can we meet obligations?), FX risk (currency moves affecting wealth), and covenant risk (loan agreements we might breach). Focus on these.

How to apply:

- Run concentration analysis across dimensions families care about: by manager, by sector, by geography, by asset class, by entity.

- Model liquidity scenarios: what if all unfunded commitments get called? What if we need to raise cash quickly?

- Track FX exposure explicitly if the family spends in a different currency than the one in which they invest.

- Monitor covenant compliance for any bank loans or credit facilities, including debt-to-equity ratios, liquidity requirements, and concentration limits.

- Use scenario and stress analysis that's explainable to principals: "If public markets drop 30%, here's the impact on total portfolio".

- Prioritize downside protection thinking: what's the risk of permanent capital loss versus volatility?

Sophisticated risk analytics matter less than frameworks that principals understand and can act on. Keep the analysis practical and tied to decisions.

11. Rebalancing & Transition Rules

Without clear rebalancing rules, portfolios tend to drift away from their target allocation, and opportunistic decisions lack a framework for guidance. But mechanical rebalancing without considering taxes and transaction costs can destroy value.

How to apply:

- Set rebalancing triggers: calendar-based (annual), threshold-based (when allocation drifts beyond bands), or event-driven (large distribution or liquidation)

- Establish cash-efficient rebalancing: use incoming cash flows and distributions to adjust allocation before selling appreciated holdings.

- Build tax-aware playbooks: harvest losses to offset gains, prioritize selling positions with the highest cost basis, and consider holding periods for long-term capital gains treatment.

- Define pre-approved levers: which positions can be trimmed without a full IC review, versus those that require approval.

- Document rebalancing decisions: what triggered the rebalance, what actions were taken, and the expected impact on allocation

For family offices managing wealth across multiple generations and entities, tax efficiency often takes precedence over precise allocation targets.

12. Cost & Fee Transparency

Fees compound over time and significantly impact net returns. But many family office portfolios lack clarity on all-in costs across manager fees, administrative expenses, carried interest, and transaction costs.

How to apply:

- Track all manager fees: management fees on committed capital versus deployed capital, administrative fees, and organizational expenses.

- Calculate carried interest accruals for private investments: preferred return thresholds, catch-up provisions, and clawback terms.

- Monitor transaction costs: bid-ask spreads, commissions, custody fees, FX conversion charges.

- Aggregate costs at portfolio level: what's the total annual cost as a percentage of portfolio value?

- Report net-of-fees performance consistently: don't mix gross and net returns in the same analysis.

- Benchmark fee levels: Are you receiving institutional pricing or paying retail rates, considering your portfolio size?

Fee transparency isn't about minimizing costs at all costs. It's about understanding what you're paying and whether the value justifies the expense.

13. Reporting Packs for Different Audiences

Your family office portfolio report needs to serve different audiences with different needs. Principals want high-level NAV and performance. Committees need detailed attribution and risk metrics. Beneficiaries need simplified summaries. Banks want specific formats for lending relationships.

How to apply:

- Build reporting from a single source of truth: one data set, multiple presentation formats

- Create beneficiary reports: simplified snapshots showing total value, asset allocation, and key changes with no overwhelming detail.

- Develop committee packs that include performance attribution, risk metrics, concentration analysis, rebalancing recommendations, and pending decisions.

- Produce banker-ready reports: formats that match loan covenant requirements, often emphasizing liquidity and debt-to-equity ratios.

- Standardize report timing: monthly summaries, quarterly in-depth reviews, and annual comprehensive reviews.

- Include both summary dashboards and detailed supporting schedules for those who want to drill down.

Mobile access enables principals to check portfolio status between formal reporting cycles without waiting for a custom report to be compiled.

14. Automate Workflows & Approvals

Managing family office portfolios involves recurring tasks with deadlines: call responses, quarterly valuations, rebalancing reviews, manager evaluations, and compliance filings. Manual tracking creates errors and delays.

How to apply:

- Document all recurring workflows: what needs to happen, who's responsible, what's the timeline, and what evidence is required.

- Assign tasks with explicit owners and due dates tied to specific holdings or reporting periods.

- Build approval chains: what requires officer approval versus full IC review, what documentation supports each approval.

- Link tasks to underlying data: When reviewing a call, the task should be connected to the LP agreement, fund performance, and current exposure.

- Set automated reminders for approaching deadlines: quarterly valuation reviews, annual IPS updates, and rebalancing assessments.

- Maintain a log of completed approvals, including supporting documents, for an audit trail and institutional memory.

Workflows alongside holdings reduce swivel-chair risk; switching between systems to find information creates errors and inefficiency.

15. Quarterly Operating Review

Committees often focus exclusively on new opportunities. Without a recurring portfolio review, existing holdings don't get systematic attention, rebalancing gets delayed, and decisions lack institutional memory.

How to apply:

- Schedule quarterly operating reviews, distinct from new opportunity discussions.

- Review performance versus benchmarks and targets: what exceeded expectations, what disappointed, and why.

- Assess allocation drift: where are we versus targets, and do we need to rebalance?

- Monitor concentration: have any positions grown too large relative to policy limits?

- Review liquidity: upcoming calls, distribution expectations, spending needs, and buffer adequacy.

- Document all decisions with supporting materials: approval minutes should reference specific files and analysis.

- Track action items with owners and deadlines: prevent decisions from evaporating after the meeting.

Record decisions, approvals, and supporting documents in a systematic manner. This creates institutional memory that persists even when key people change roles.

How to Build Your Family Office Portfolio Management System

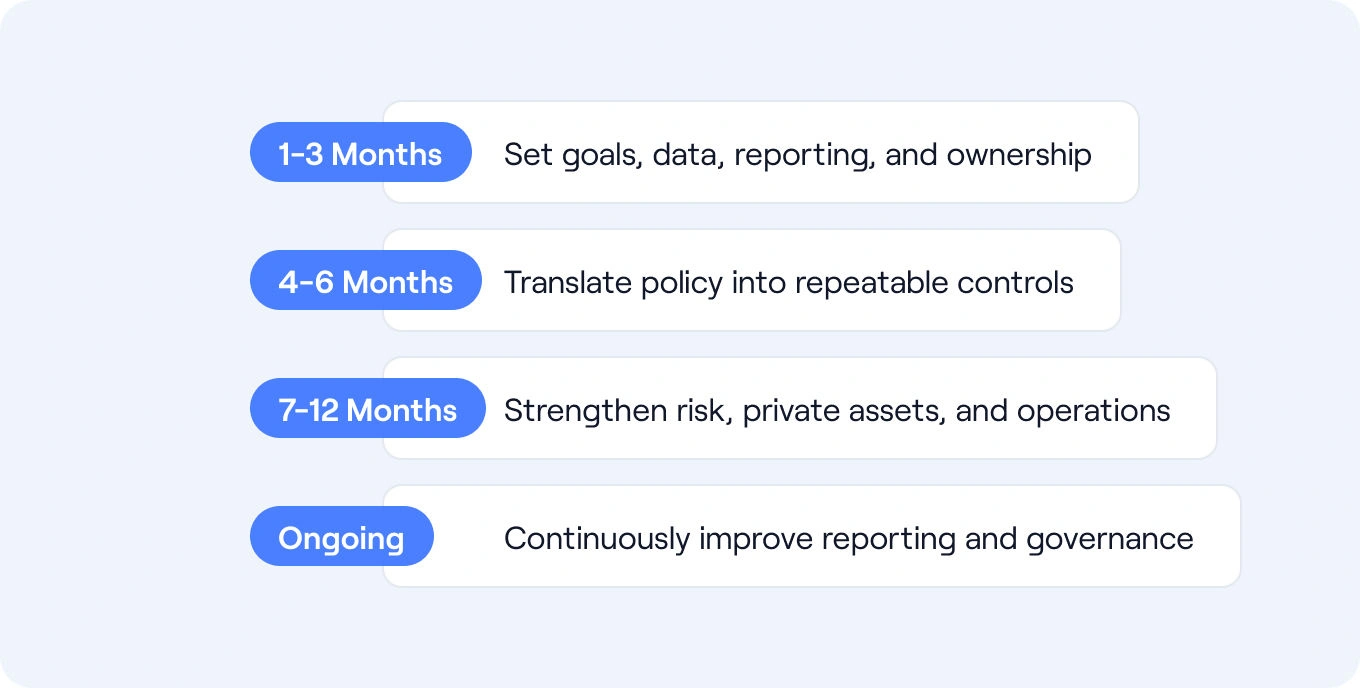

These 15 practices form a complete framework, but you don't need to implement everything simultaneously. Most successful single family offices follow a phased approach:

Phase 1 (Months 1-3): Foundation

- Draft IPS reflecting family objectives and risk tolerance

- Build a consolidated holdings view with basic position and valuation data

- Establish reporting cadence and formats for key stakeholders

- Document current governance: who decides what at which thresholds

Phase 2 (Months 4-6): Process

- Translate IPS into strategic asset allocation with tactical ranges

- Implement systematic performance calculation for both liquid and private holdings

- Establish rebalancing triggers and cash management disciplines

- Create a manager selection framework and pipeline process

Phase 3 (Months 7-12): Refinement

- Build risk monitoring appropriate to family concerns: concentration, liquidity, FX

- Develop a private assets playbook for diligence, pacing, and tracking

- Implement workflow automation for recurring tasks and approvals

- Establish quarterly operating review discipline

Ongoing: Optimization

- Refine reporting based on stakeholder feedback

- Update IPS as family circumstances evolve

- Enhance analytics as portfolio complexity grows

- Build institutional memory through documented decisions

The goal is building repeatable, trustworthy processes that create clarity and enable better decisions.

The Technology That Supports the Framework

Family office portfolio management requires technology that matches how single family offices actually work. It needs to be comprehensive enough to handle multi-entity structures and alternative assets, but not so complex that it requires dedicated IT staff.

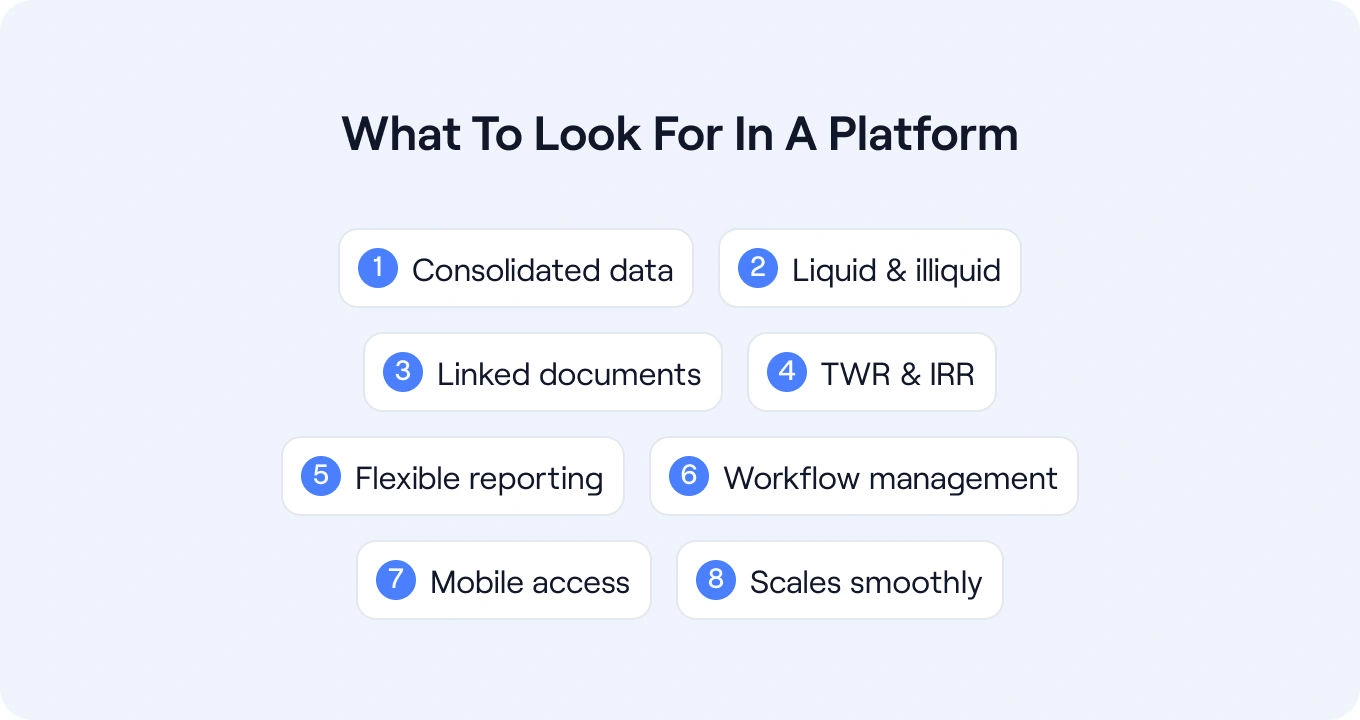

Look for platforms that:

- Consolidate data across custodians and manual inputs into a single holdings register

- Support both liquid and illiquid asset classes without forcing everything into public market paradigms

- Link documents directly to holdings, so supporting detail is always accessible

- Calculate both TWR and IRR performance appropriately for different asset types

- Enable flexible reporting serving different audiences from the same data set

- Provide workflow management for recurring tasks tied to holdings and portfolios

- Offer mobile access so principals can check the status without waiting for compiled reports

- Scale from tens of millions to billions without architectural changes

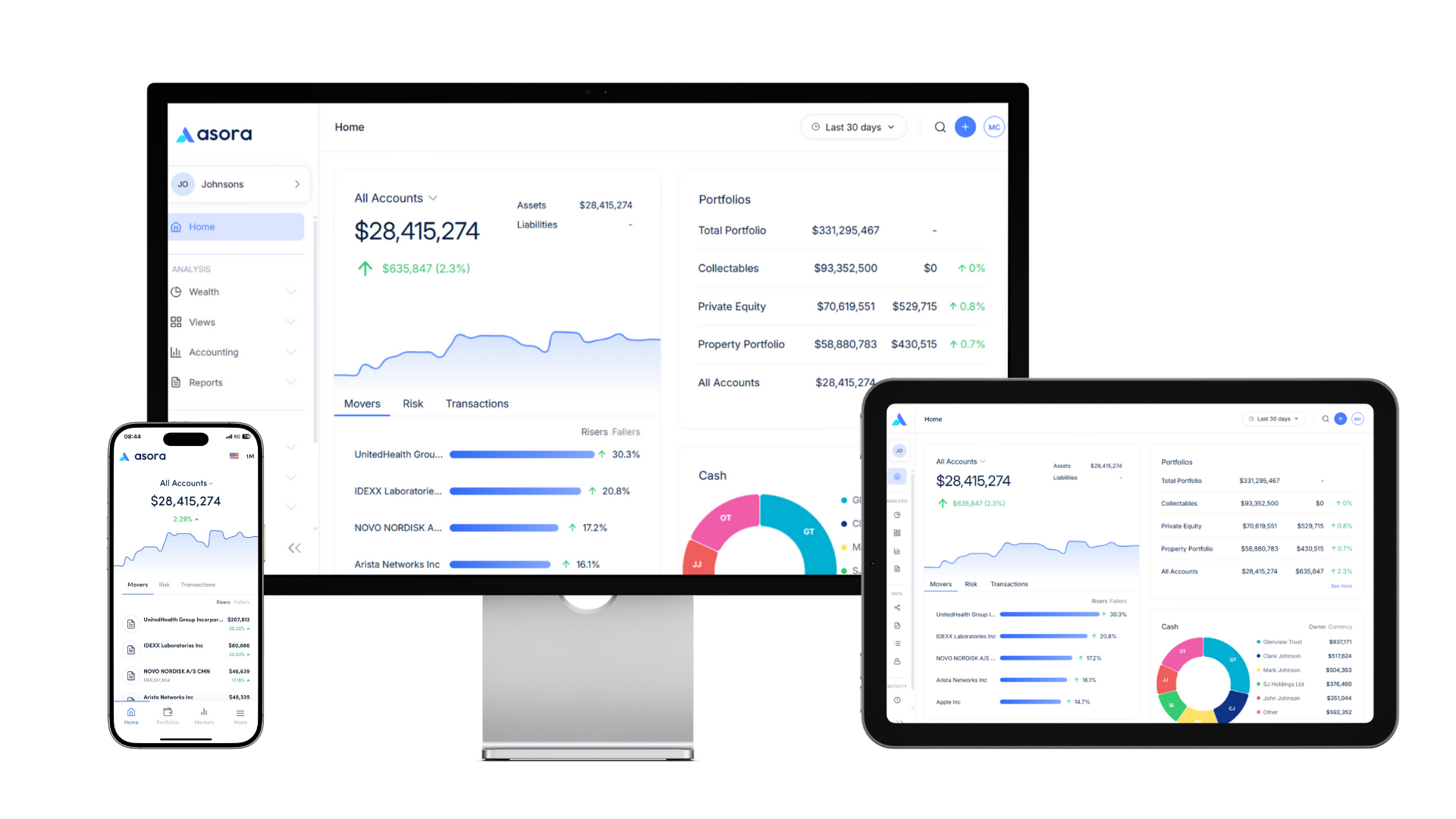

Asora addresses these needs for family office portfolio management by consolidating portfolio data, linking documents to holdings, tracking workflows, and enabling reporting without the complexity typically associated with institutional-grade solutions.

How to Get Started with Better Portfolio Management

If you're currently managing your family office investment portfolio through spreadsheets, disconnected systems, and manual processes, the framework outlined above might feel overwhelming.

Start here:

- This week: Assess your current state against the 15 practices. Score each honestly—where are you strong, where are gaps? Don't try to fix everything at once.

- This month: Pick your most significant pain point (usually data consolidation, private assets tracking, or reporting) and build a plan to address it. Often, the foundation (consolidated data with document linking) enables progress on multiple other practices.

- This quarter: Validate your approach with actual data. Test whether your consolidated view is complete, whether your workflows are actually working, and whether your reports effectively serve stakeholder needs.

The goal is progress, not perfection. Each practice you implement makes your family office portfolio management more systematic and reliable.

Manage Your Family Office (Better) with Asora

Family office portfolio management isn't about implementing the most sophisticated analytics or buying the most expensive platforms. It's about codified policy, disciplined processes, and a single source of truth that enables trustworthy, repeatable oversight.

The 15 practices outlined above give you a framework. The specifics (exact allocation targets, specific risk thresholds, particular reporting formats) will be unique to your family's objectives, risk tolerance, and circumstances.

See how Asora operationalizes multi-asset class portfolio management family office infrastructure:

It’s an all-in-one platform built for how family offices actually work.

Request a demo to see your structure mapped and explore whether Asora is a good fit for your family office portfolio management needs.

FAQ

How do family offices manage multi-asset class portfolios?

Effective management requires consolidated data, differentiated treatment for liquid and illiquid assets, and governance that is fit for purpose. Liquid holdings connect via custodian feeds for automated updates. Private investments require tracking of commitments, capital calls, distributions, and valuations. Systems should calculate TWR for liquid portfolios and IRR for private investments and produce unified analytics. Asora aggregates bank and investment feeds, tracks private asset activity, and standardises reporting across entities.

What is the difference between single-family office and multi-family office portfolio management?

Single-family offices tailor their policies to one family’s goals, risk tolerance, spending, and values, often accommodating concentrated positions and operating businesses. Multi-family offices serve multiple families, which calls for more standardised strategies, greater liquidity, and vehicles that fit varied tax profiles. Both need disciplined processes and consistent reporting. Asora provides a single source of truth that scales from one-family structures to multi-client environments.

How should family offices track private equity and venture capital investments?

Use systematic processes: maintain commitment registers, model capital call pacing by vintage and strategy, link LPAs and side letters to each position, track distributions and cash flows to calculate IRR, and maintain valuation roll-forwards between quarterly NAVs. Many families use platforms with private-asset modules to manage illiquid investments alongside liquid holdings. Asora captures commitments and capital calls, links documents to each fund, and consolidates performance for on-demand review and analysis.

What should be included in a family office portfolio report?

Include current NAV with period changes, allocation versus target with drift analysis, performance by asset using the right metric, concentration by manager or sector, and a liquidity view that includes commitments and upcoming obligations, with supporting detail via linked documents. Tailor depth to the audience while sourcing every view from a single, consistent dataset. Asora produces consolidated reports with drill-through capabilities to documents and evidence, allowing teams to quickly transition from summary to detail.

.png)