Author

.png)

Table of contents

"What used to take hours or days is now done in minutes"

Private asset management for family offices requires more than tracking capital calls. UBS reports family offices’ average allocation to alternative investments was 44% in 2024, indicating structured oversight is essential. An entity-first, statement-based approach supports defensible IRR, commitment pacing, liquidity planning, and board-ready reporting across private markets. In this article, we outline 11 practical ways family offices can strengthen their private asset management and gain complete visibility across entities.

Family offices with allocations to private markets often rely on spreadsheets, shared drives, and manager portals. Statements arrive quarterly, monthly, annually, or semi-annually, while capital call notices sit in inboxes, side letters live in PDFs; this results in fragmented data, delayed reporting, and limited visibility across entities.

Fragmented spreadsheets and scattered portals often create reconciliation challenges, particularly when statements arrive at different cadences. These reporting gaps are common across family offices.

As complexity increases, many families move away from spreadsheets toward structured platforms designed for consolidated reporting. This shift often extends beyond reporting accuracy to broader workflow, control, and governance support (eg, approvals, auditability, policy reporting) within the family office. Platforms such as Asora are designed to support this transition by bringing banking and investment data where integrations/feeds are available, alongside statement-driven private assets into one secure, cloud-based view for ultra-high-net-worth individuals and lean single family offices.

In this article, we use ‘private asset management’ to include private markets operations: the oversight, administration, and performance measurement of non-public investments, supported by controls that enable governance.

This typically includes private equity, venture capital, private credit, real estate, infrastructure, and direct private holdings across multiple entities.

In practice, most professionals would describe this function as private markets operations, private investments administration, or private markets reporting and controls. The objective is not manager selection or deal sourcing, but control, accuracy, and defensible reporting.

Private asset management, in this operational sense, includes:

At scale, this becomes a control and oversight function that supports governance. As alternatives represent a significant share of family office portfolios globally, structured oversight ensures that exposure, liquidity, and performance are transparent across trusts, limited partnerships, and holding structures.

Scope typically includes:

The outcome is a single view for exposure, cash flows, and documents, updated in line with manager reporting cycles.

This matters because alternatives are a material part of many family office portfolios. In its Global Family Office Report 2025, UBS reports a 44% average allocation to alternative asset classes (including private equity, private debt, hedge funds, real estate, infrastructure, etc.) globally, with regional variation across North America and Western Europe. This reinforces the reporting load created by private equity, private debt, real estate, and other non-public holdings.

Private equity exposure in family offices often spans multiple structures and entities. Typical categories include:

Private equity and venture

These drive reporting needs around capital calls, distributions, unfunded commitments, and performance.

Real estate and infrastructure

Entity complexity, debt schedules, capex, operating cash flows, and periodic valuations add complexity.

Private debt and specialty credit

Often income-focused, with varying liquidity terms.

Funds of funds and secondaries

These require layered reporting and look-through where available. Look-through may be partial and lagged; classification methods should be documented.

Tangible assets (register only)

Art, vehicles, wine, aircraft, and other collectibles are typically tracked via a register for ownership, insurance, and estate planning. Valuation is periodic or event-based rather than performance-driven. Insurance values can be directional; appraisal/market comps are preferred for valuation accuracy.

Private asset management is ultimately an operational discipline. It touches reporting, accounting, document control, and oversight, all core elements of modern family office operations.

Complete visibility in private asset management is not achieved through dashboards alone. It comes from building a defensible record of commitments, cash flows, valuations, and contractual terms across entities. For family offices with significant allocations to private markets, this becomes a governance function as much as a reporting task.

Platforms like Asora support this process by helping ultra-high-net-worth individuals and lean single family offices track private assets, store documents, calculate performance, and maintain a consolidated record across entities.

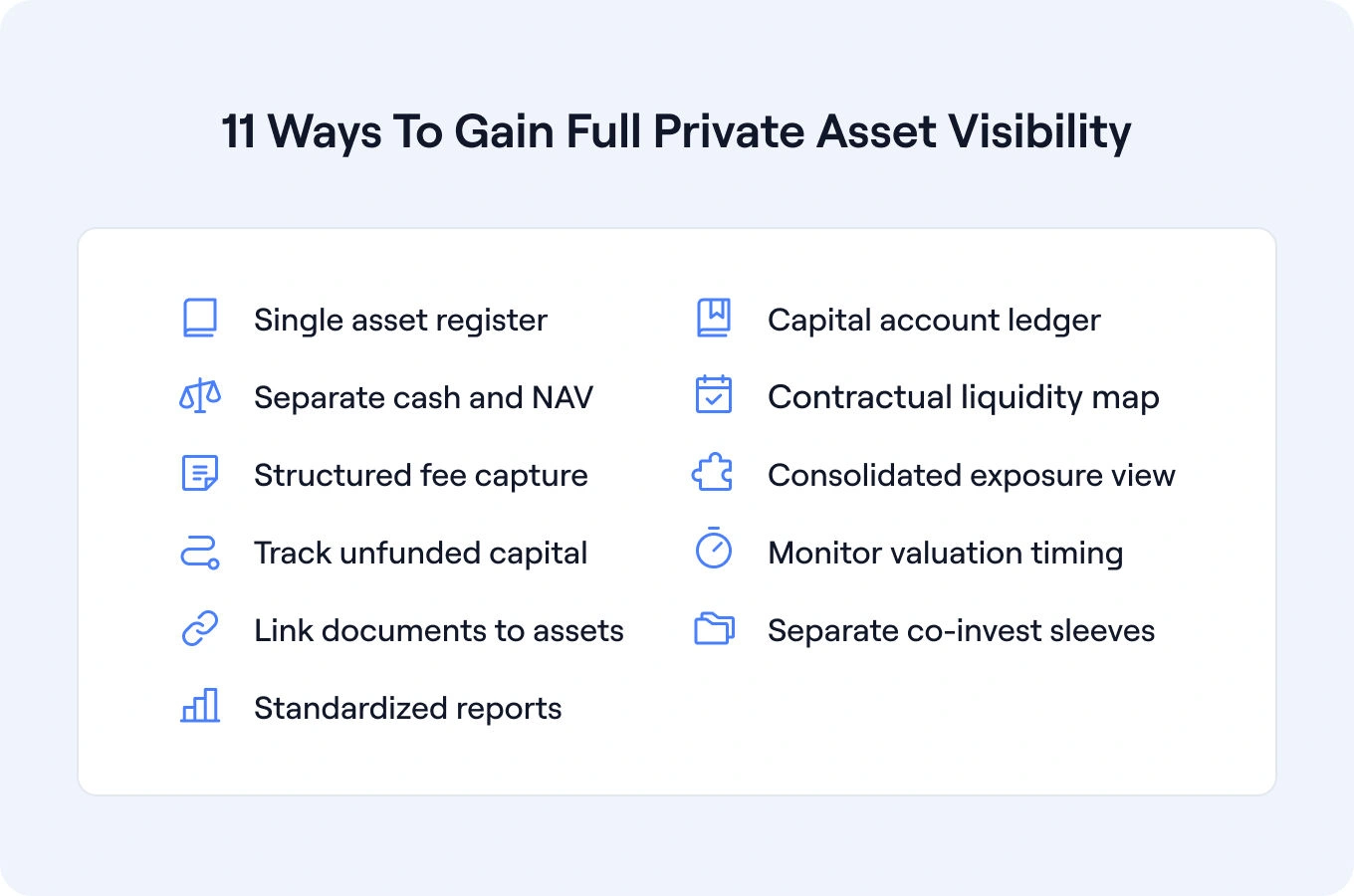

A private asset register is the control point for every private investment. It should define the investment once and assign ownership across the relevant entities (trusts, limited partnerships, holding companies) without duplication.

This register becomes the authoritative source for commitment size, vintage, strategy classification, and status (investing, harvesting, exited). Without it, offices often reconcile multiple spreadsheets that define the same asset differently across entities. Over time, this creates inconsistencies in exposure reporting and performance attribution.

The key question when evaluating software is, does the system treat the investment as a single object with entity-level ownership fields, or does each entity hold a separate, disconnected record?

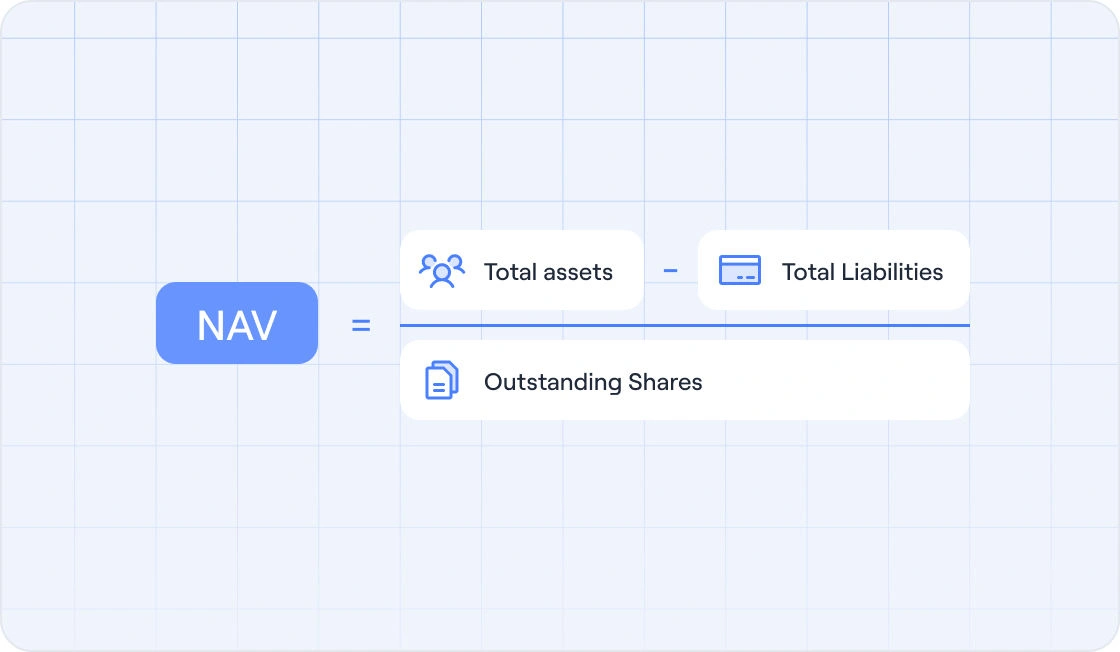

Private markets are statement-driven. For each limited partner position, capital account statements and/or quarterly reports/administrator statements (depending on vehicle) are the main source records of economic activity. They do not replace the family office’s general ledger or trust accounting system. Instead, they serve as the authoritative external record that must be reconciled to internal books and cash movements.

While public assets may rely on custodial feeds, private investments require structured statement capture alongside broader data aggregation processes.

Allocator-grade visibility requires capturing manager-reported NAV from capital account statements, quarterly reports, or audited financial statements. That NAV should feed into a documented period-to-period change-in-NAV (capital account) rollforward.

This rollforward should tie, using manager-provided line items where available and documented reconciling items where not:

Each movement should reconcile to capital activity and align with the office’s general ledger and underlying cash records. The result is not simply performance reporting, but a defensible economic history of the fund position. When a board asks how a number was derived, the office should be able to trace it back to a dated statement and documented cash flow.

Performance in private markets contexts depends on both recorded cash flows and manager-reported valuations. These are distinct inputs.

A structured workflow records cash movements when they occur and stores valuations when statements are issued. IRR and MOIC are then calculated from this record, not from blended estimates.

This distinction becomes critical in volatile periods. If valuation timing differs across funds, offices need clarity on which positions reflect updated data and which do not. Software should support a consistent calculation methodology and exportable cash-flow histories.

Liquidity in private markets is structured, but not scheduled in the same way as public securities. For closed-end private equity and venture capital funds, liquidity is primarily realized through distributions (and, optionally, secondary sales), rather than redemptions. For semi-liquid or evergreen alternative vehicles where redemptions are permitted, liquidity is governed by notice periods, lockups, gates, and other fund terms, and is rarely discretionary.

For closed-end private equity and venture capital funds, capital calls are governed by the Limited Partnership Agreement (LPA), yet their timing remains manager-driven. Distributions are even less schedulable, as they depend on underlying realizations rather than preset payout dates.

Certain alternative vehicles with redemption or repurchase terms, such as hedge funds, evergreen private credit or real asset funds, and interval or tender-offer registered funds that hold less-liquid assets, may include notice periods, redemption or repurchase windows, and gating provisions. These features are contractual, but they do not apply uniformly across all private market strategies.

A mature private markets oversight process stores these relevant contractual elements and aligns them to a forward-looking planning framework. Rather than creating a fixed liquidity schedule, it documents:

Forward projections should therefore be scenario-based, grounded in fund documentation and historical pacing patterns.

For principals, this provides clearer visibility into expected capital call pacing and distribution ranges, with assumptions made explicit. For boards, it frames downside scenarios if realizations slow or exit timelines extend.

Two private equity funds with identical commitments may produce materially different outcomes due to fee/carry terms, expense policies, recycling, and fee offsets.

Visibility requires linking management fees, hurdle rates, carried interest mechanics, and side-letter variations directly to the investment record. These terms can materially affect net IRR and multiples, sometimes as much as differences in gross performance—especially across similar strategies.

When reviewing software, assess whether fee and hurdle information is structured or simply stored as a document attachment. Structured capture supports governance and variance explanation.

Family offices often hold the same strategy through multiple vehicles or structures. Without careful entity mapping, exposure can be overstated or double-counted. Define rules for beneficial/economic ownership (including blockers/parallel vehicles) and document them.

Complete visibility means viewing exposure at two levels:

This becomes increasingly important as private market portfolios diversify and expand over time.

Unfunded commitments represent future obligations. They affect liquidity planning and pacing decisions, even though they are not yet reflected in NAV.

A mature view of private asset management places funded and unfunded capital side by side. This allows offices to assess whether new commitments align with allocation targets or whether pacing adjustments are required.

Software should support commitment tracking against documented allocation policy, not just historical performance reporting.

Private assets update on reporting cycles, commonly quarterly, sometimes monthly (certain credit/evergreen vehicles), and sometimes semi-annual or annual, depending on the manager and asset type. This creates inherent timing gaps.

Visibility improves when each fund’s reporting cadence is stored, and the last statement date is clearly recorded. Late or missing NAVs should be visible rather than discovered at quarter-end.

The goal is transparency around data timing, not artificial smoothing.

Private asset management is document-intensive. Limited Partnership Agreements, capital call notices, side letters, audits, and tax forms are part of the economic history of the investment.

When documents are disconnected from capital records, reporting becomes manual, and audit preparation slows.

Software should support linking each document to its associated investment and entity, so that performance, exposure, and documentation are aligned in a single record.

Co-investments operate differently from pooled funds. They may have different fee structures, different timing profiles, and deal-specific exit events.

Blending them into a generic private equity category reduces clarity. Instead, deal-level tracking should store deal-level cash flows, ownership by entity, and instrument/class details where applicable (eg, multiple rounds, prefs, convertibles).

This enables clearer attribution of performance and concentration.

The final test of private asset management is consistency. Quarter after quarter, the office should be able to export:

Where sector and geography reporting relies on manager-provided look-through, the source and last-updated date should be visible. Definitions may vary by manager, and underlying classifications may be limited or stale.

Consistency builds institutional memory. It also reduces dependency on a single team member to “reconstruct” history each reporting cycle.

For principals, this translates into clarity and comparability. For investment committees and boards, it supports oversight and policy alignment.

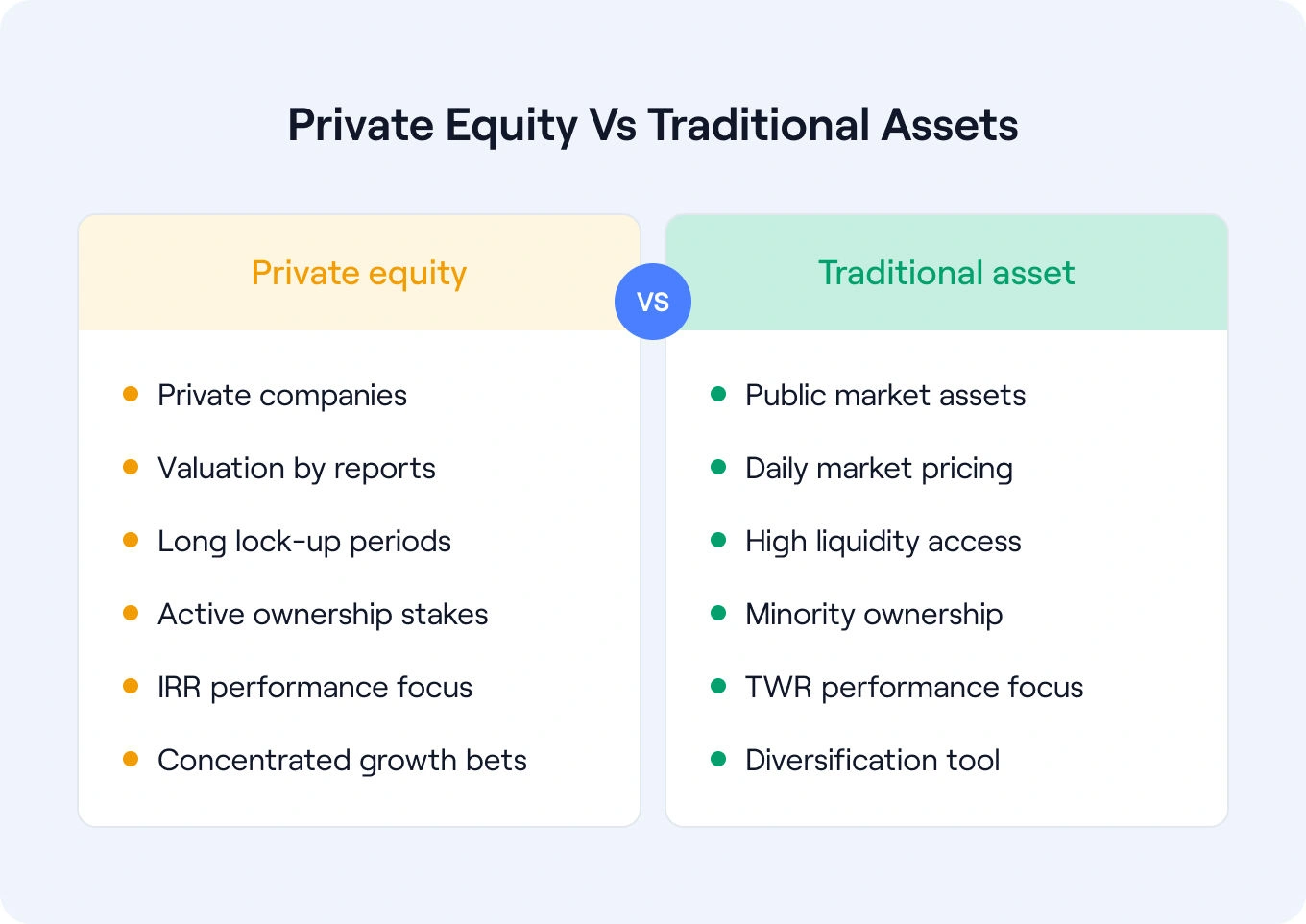

Private asset management often spans both traditional asset management and private equity. While both aim to grow wealth, the underlying mechanics differ significantly.

Traditional asset management focuses on overseeing liquid asset classes such as equities, fixed income, mutual funds, and exchange-traded funds. These investments can typically be bought or sold quickly, and performance is evaluated using observable market pricing. At the strategy or manager level, returns are typically measured using time-weighted return (TWR). At the client or total-portfolio level, where contributions and withdrawals are material, money-weighted return (MWR), often expressed as Internal Rate of Return (IRR), may also be used.

Private equity, by contrast, involves illiquid investments in privately held companies. Investors typically commit capital for ~10+ years (often extendable), with realizations dependent on exit timing..

Buyout firms often acquire controlling stakes in portfolio companies, allowing them to influence strategy, management decisions, and capital structure directly. Venture capital and minority growth equity strategies more commonly take minority positions, though they may still influence governance through board representation, protective provisions, and negotiated shareholder rights. Because private equity depends on long holding periods and negotiated governance structures, outcomes can vary widely across strategies and managers. Industry commentary from McKinsey’s Global Private Markets Report notes that firms are increasingly focusing on sustained operational transformation (versus relying primarily on financial engineering), particularly as the cycle has tightened.

Because private equity depends on long holding periods and active ownership, it carries higher dispersion of outcomes. However, it also offers the potential for differentiated returns compared to traditional liquid asset classes.

Many high-net-worth investors combine both approaches, using traditional asset management for liquidity and diversification, and private equity for growth and portfolio differentiation.

Within this context, private asset management services provide access to alternative investments while also supporting the governance, reporting, and liquidity oversight required to manage them responsibly.

Private asset management becomes difficult when:

Fixing this starts with a standard foundation:

Without this base layer, reporting remains manual and exposed to version-control risk.

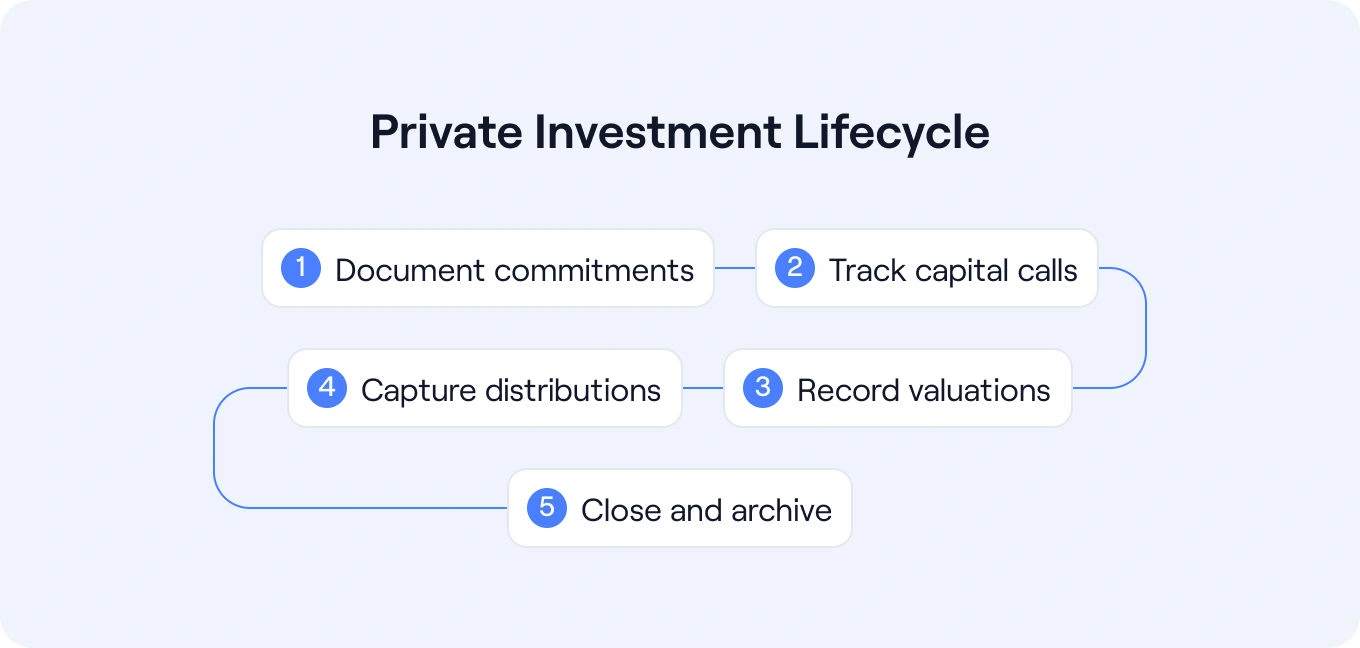

Private investments do not behave like public securities. They move through contractual stages, each with accounting, governance, and liquidity implications. A structured lifecycle framework reduces errors and creates institutional memory.

While individual investments may involve follow-ons, restructurings, or continuation vehicles, a typical lifecycle includes the following control points.

At commitment, the office is not simply recording an amount. It is documenting an obligation. This stage should capture:

This forms the baseline against which pacing, exposure, and future performance will be assessed. Weak documentation here creates downstream reporting distortion.

Capital calls are the operational reality of private asset management. Each call alters liquidity, funded exposure, and IRR.

A mature process:

Over time, this produces a defensible funded-capital history rather than a reconstructed estimate.

Valuation in private markets is periodic and manager-reported. It is not a daily market observation.

At each statement cycle, the office should:

This discipline allows the office to distinguish between updated and stale data across the portfolio, which is particularly important when reporting to boards.

Distributions change both liquidity and performance profile. Each distribution should be:

Where detail is provided, classification should distinguish distribution type, for example, interest versus principal in private credit strategies, or realized proceeds versus recallable capital or return-of-capital indicators in private equity (where disclosed by the manager and consistent with fund documentation/tax reporting). Tax characterisation should align with formal tax reporting to ensure consistency between performance records and tax filings.

This enables accurate IRR calculation and supports reconciliation during audit or tax preparation.

An exit is not simply a final distribution. It is the closure of an economic record. At exit, the office should:

This closes the lifecycle in a way that supports historical analysis and future allocation decisions.

Clear lifecycle tracking supports the transition from asset management to private equity reporting at the investment level to consolidated reporting across the entire structure.

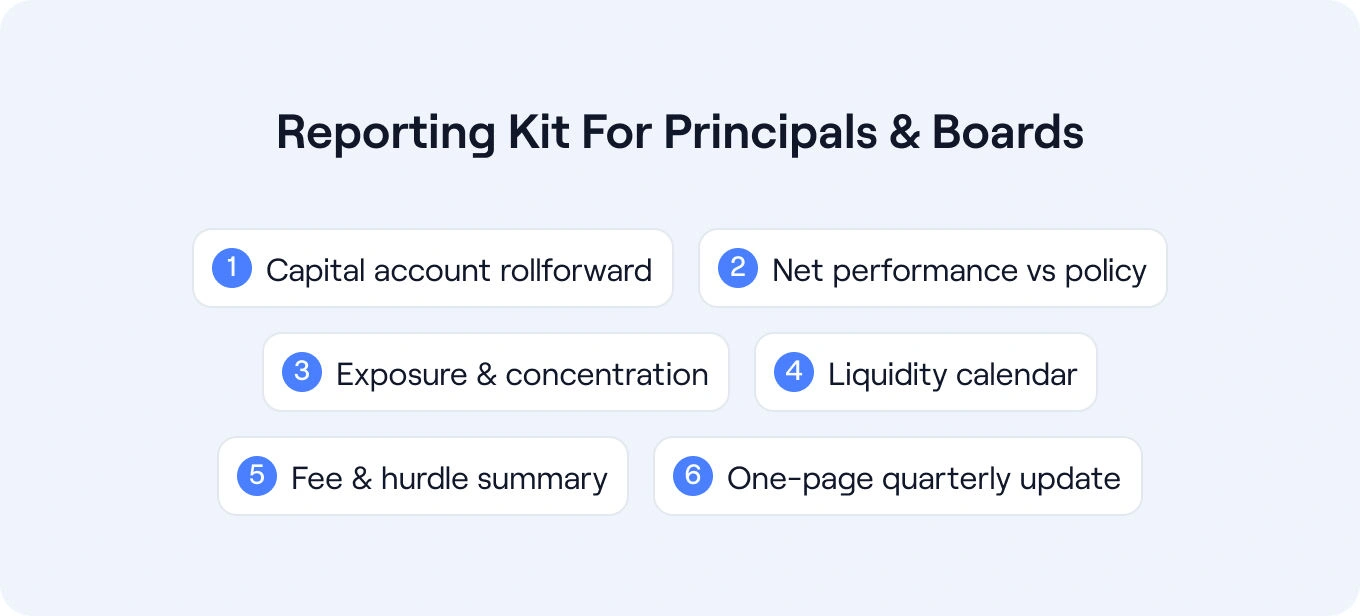

Private asset management reporting should change by audience. The data is the same. The framing is not.

Principals typically seek clarity and decision support. Investment committees and boards require drivers, policy alignment, and documented methodology.

For principals, the rollforward answers: How did my private allocation change this quarter?

The focus is on net change, capital deployed, distributions received, and current value.

For an investment committee or board, the same rollforward becomes an analytical bridge. It should explain the performance by the driver:

Variance versus the prior quarter should be explainable directly from the report, without manually recalculating prior-period figures.

Performance reporting should distinguish between the method used to calculate returns (eg, IRR based on recorded cash flows, net of fees) and the benchmark used to assess those returns (eg, a policy index or target range). The first addresses accuracy, the second addresses evaluation. Both should be explicitly documented. Clear methodology, documented benchmarks, and consistent IRR calculation are core elements of effective performance monitoring.

Principals typically want to know whether private allocations are delivering against long-term objectives.

Boards require:

The benchmark approach should specify whether performance is assessed using public market equivalent (PME) analysis, peer or vintage benchmarks, or predefined target ranges. Methodology should clarify whether IRR, distributed-to-paid-in (DPI), total value to paid-in (TVPI), or other multiples are used, and how valuation timing affects reported results.

This avoids benchmark mismatch and reinforces governance discipline.

Exposure reporting is not a heat map exercise. It is a risk control. For principals, a summary of top exposures by manager, sector, and geography supports intuitive oversight.

For boards, the same data should reference:

Consolidated exposure must avoid double-counting across entities, particularly where multiple vehicles hold overlapping strategies.

Liquidity visibility should translate contractual terms into forward planning.

Principals typically focus on:

Boards require a more conservative framing. Reporting should clarify:

This transforms liquidity from an estimate into a documented risk profile.

Fee transparency is often underreported in private wealth asset management. For principals, the relevant question is: What are the total fees paid to date, and how do they affect net return?

For boards, reporting should break down:

This level of clarity supports better manager comparisons over time.

Every reporting cycle should end with a concise, structured narrative.

For principals, this should highlight:

For boards, this summary should also note:

The goal isn’t volume, it’s clarity with traceable inputs.

Over time, this structured quarterly summary becomes part of the office’s institutional record. It creates continuity across reporting cycles, supports board oversight, and reduces reliance on informal explanations. In private asset management, consistency of narrative is as important as consistency of numbers.

Private asset management failures are rarely dramatic. They are incremental and cumulative. They tend to arise from small inconsistencies, such as a NAV that is not updated on time, a side letter that cannot be surfaced quickly, or an unfunded commitment tracked in one spreadsheet but not another.

Individually, these issues appear manageable. Over several quarters, however, they compound. Exposure reports drift from source statements. Performance comparisons rely on inconsistent benchmarks. Liquidity forecasts reflect assumptions rather than contractual terms. By the time a discrepancy becomes visible, it often requires manual reconciliation across multiple files.

The objective is not perfection, but structural discipline.

The following pitfalls are common in lean family offices and can be addressed with relatively simple control measures.

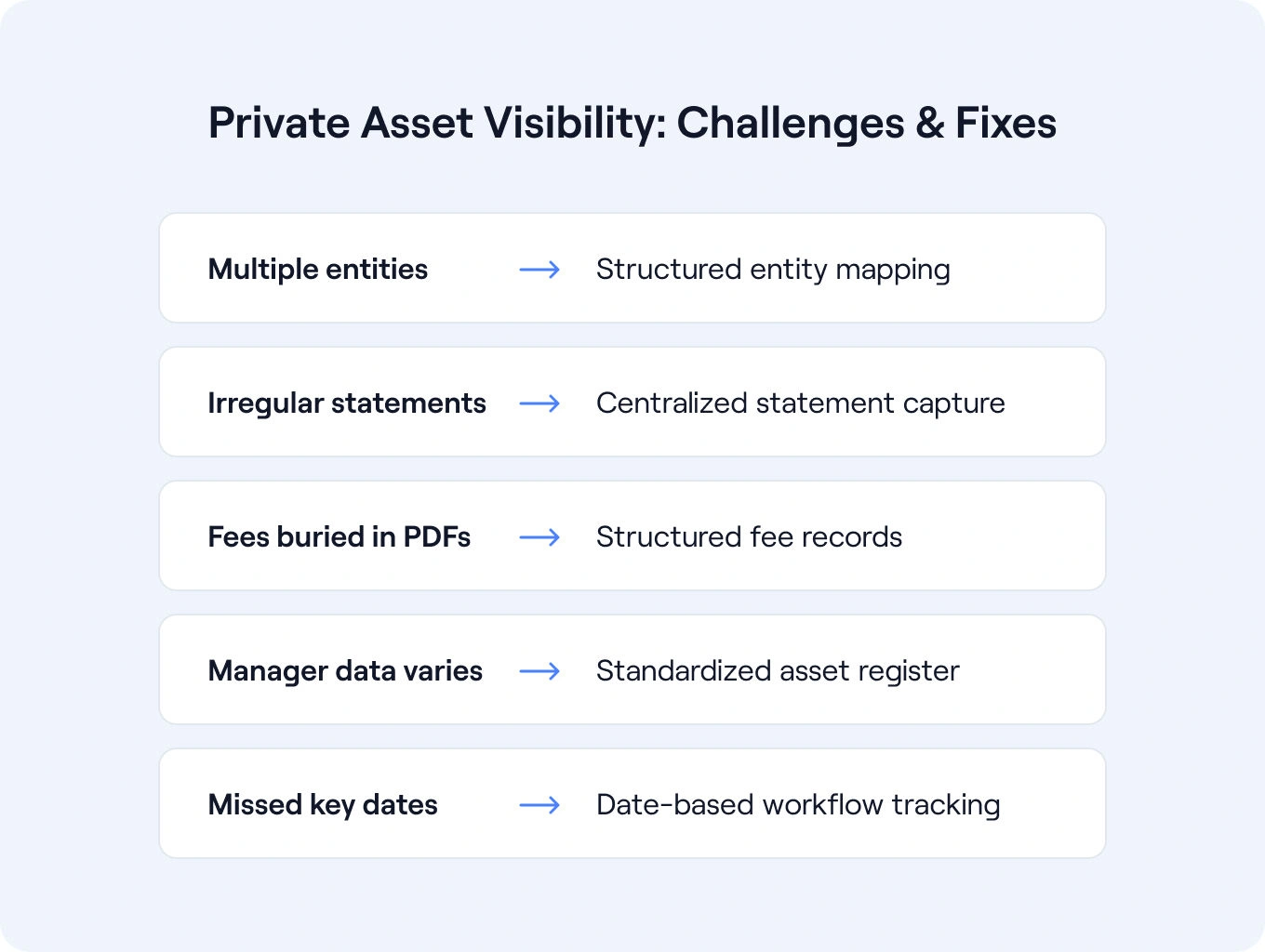

When statement cadence is not tracked, stale valuations blend into consolidated reports unnoticed.

Structural fix: store reporting frequency per fund and make last-updated dates visible in reports.

When economic terms live only in PDFs, variance explanations become manual.

Structural fix: tag and link side-letter provisions directly to the investment record.

Without a single register, the same fund can appear multiple times in consolidated reporting.

Structural fix: define the investment once and allocate ownership across entities using structured fields.

Using inconsistent or undocumented benchmarks across sleeves distorts performance interpretation.

Structural fix: document the policy benchmark per sleeve and reference it consistently in performance exports.

As alternatives represent a significant share of many family office portfolios (44% on average globally in 2024, according to UBS Global Family Office Report 2025), reporting expectations have shifted from informal tracking to structured oversight.

Family offices moving from traditional asset management to private equity-heavy portfolios often discover that spreadsheet-based tracking does not scale. Public-market workflows built around daily pricing and custodial feeds do not translate cleanly to capital-call-driven investments with quarterly valuation cycles.

Private asset management, when treated as an entity-first, statement-based discipline, creates:

As documentation consolidates into digital systems, security standards and access controls become part of the oversight framework, an increasingly important consideration for family offices managing sensitive financial data. Platforms such as Asora support this shift by enabling lean single family offices to track private assets, link documentation, calculate performance, and export consistent reports across entities.

For lean teams, the objective is not enterprise complexity. It’s a durable structure. A private asset register, capital-account discipline, linked documentation, and consistent exports create clarity across entities and over time.

Request a demo to see how structured private asset management supports consolidated visibility across private equity, real estate, private debt, and other alternatives.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Institutions allocate across buyout, growth, venture, secondaries, and private credit (e.g., direct lending, mezzanine, asset-backed), sized within policy ranges and pacing models. Leveraged loans are generally syndicated and often accessed via liquid loan funds/CLOs, though they may also feature in certain private credit mandates. Allocations are sized within broader portfolio management frameworks to balance risk and maximize returns over time.

Private equity managers create value through governance, strategic change, and operational improvements in portfolio companies, alongside disciplined entry and exit execution. Private credit managers create value through origination, structuring (covenants/collateral), monitoring, and active workout or servicing when needed. Because private equity depends on long holding periods and negotiated terms, performance evaluation focuses on cash flows, fees, and exit outcomes.

Within wealth management, private equity should align with a family’s financial plan, liquidity needs, and overall strategy. Since capital is tied up for several years, allocations must balance risk across different asset classes. Structured private asset management supports clearer oversight and alignment with long-term financial goals.

Traditional asset management focuses on daily pricing and market benchmarks. Private equity depends on commitment pacing, statement-based valuations, and capital account tracking. Effective portfolio management requires structured oversight across entities to ensure exposure, performance, and liquidity are accurately reflected. Software platforms such as Asora are designed to support this by linking documentation, maintaining capital account rollforwards, and exporting consistent, board-ready reports across private investments.

.png)

.jpg)

.png)

.png)

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.webp)