TL;DR

Building a family wealth strategy takes coordinated planning across wealth preservation, tax-efficient transfers, and operational infrastructure. This guide covers fundamental family wealth management strategies, from estate planning and business succession to the technology backbone that enables modern wealth management.

Build A Family Wealth Strategy That Endures

A 20-year study by the Williams Group showed that 70% of wealthy families lose their wealth by the second generation, and 90% by the third.

A family wealth strategy is your blueprint for preserving assets, minimizing tax liability, and successfully transferring assets to the family's financial future. This means coordinating estate planning, investment management, family governance, and the operational systems that tie everything together.

The families that maintain wealth across generations share common traits:

- Open communication about finances

- Clearly documented family's values

- Financial education programs for younger family members

- Robust infrastructure to track finances and investments

Below, we’ll walk you through proven strategies for family wealth preservation, growth, and transfer (along with the operational foundation that makes it all possible).

Why A Family Wealth Strategy Is Needed

The next decade brings challenges that manual spreadsheets and quarterly PDF reports struggle to handle.

First, there's the shift toward private equity, venture capital, and alternative assets. High-net-worth individuals are allocating more to illiquid investments with complex cash flows. Capital calls arrive with tight deadlines, distributions come unpredictably, and valuations are typically updated quarterly (often with a reporting lag), and some direct holdings require periodic appraisal. Tracking this in Excel can create version-control risk, manual errors, and slower response times unless you have strong controls and a disciplined workflow.

Second, for many larger or internationally connected families, cross-border holdings are becoming increasingly common. International markets offer diversification, but they add currency exposure, different tax treatment, and regulatory complexity. Your family wealth management strategies need to account for family assets across multiple jurisdictions.

Third, reporting expectations are rising. The next generation expects timely data, mobile access, and precise answers to "What do we own?" and "How are we performing?" Static quarterly reports don't cut it anymore.

Fourth, younger family members want to be involved. They're asking informed questions about asset allocation, environmental impact, and alignment with the family's values. You need systems that let you give them appropriate access without compromising security or overwhelming them with detail.

Ultimately, families need a standard rhythm where data updates flow in automatically, saved views answer common questions in seconds, and documents sit next to the numbers so a five-minute decision is possible.

That's not aspirational, either. Whether you run an SFO, use an MFO, or outsource to advisors, the same principles apply, but implementation will vary by operating model.

Without this foundation, you're constantly playing catch-up. With it, you're making proactive decisions based on current information.

12 Strategies For Family Wealth That Build Lasting Prosperity

Use this list to prioritise by impact and complexity. Each strategy pairs what to do with the operational deliverable so your team can make good decisions.

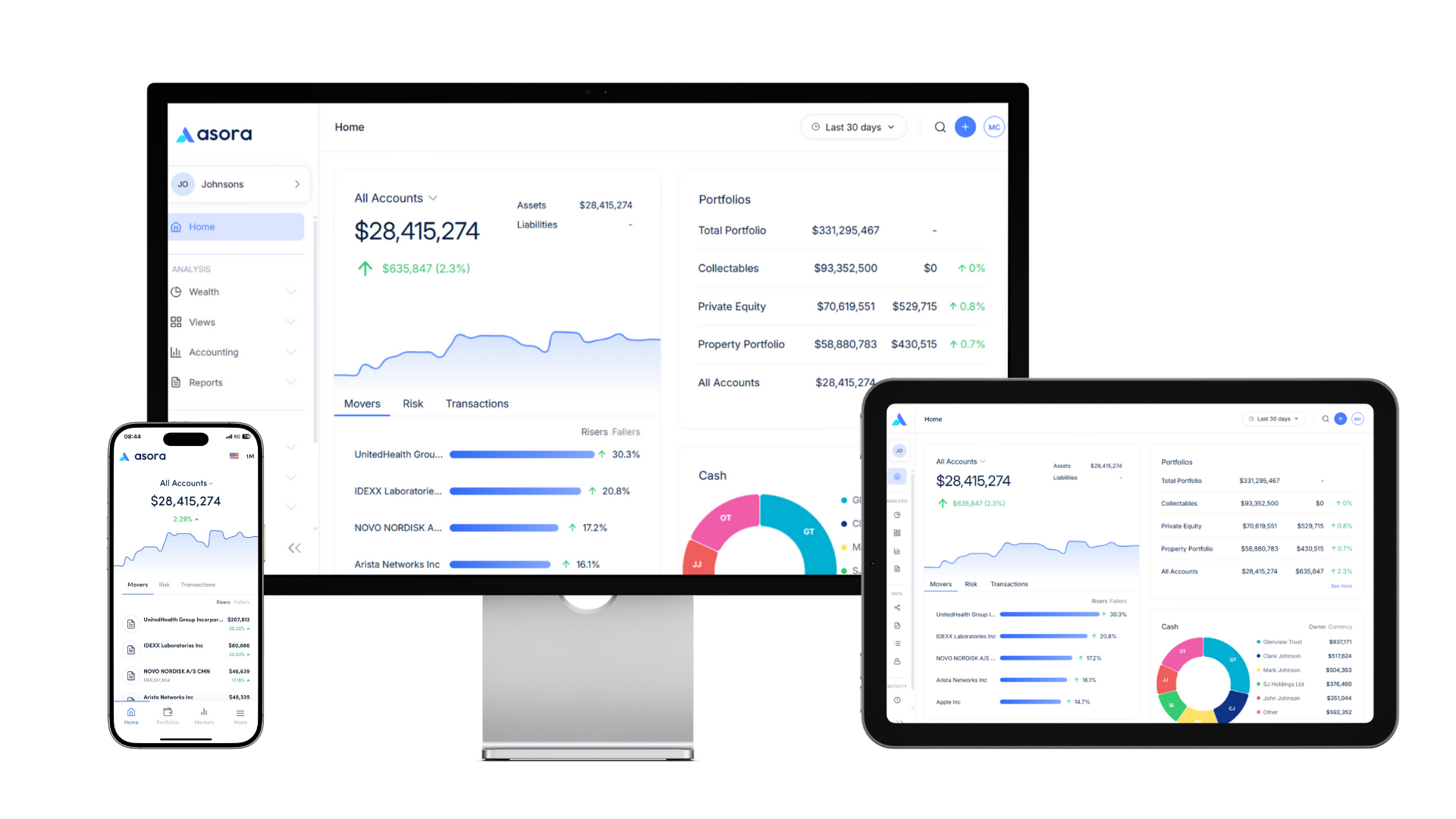

1. One View of Wealth

Most high-net-worth families have assets scattered across multiple banks, broker/custodial platforms, fund managers/administrators, and operating business interests. Each sends separate statements in different formats. You're pulling PDFs from portals, copying numbers into spreadsheets, and hoping you didn't miss anything.

This fragmentation makes it impossible to answer simple questions:

- What's our total net worth?

- How much is in alternatives versus traditional investments?

- Which entity owns what?

The Strategy

Build a single consolidated view by aggregating custodian and bank feeds with timely updates. Data aggregation can automate transaction and balance feeds with precise dates and currencies.

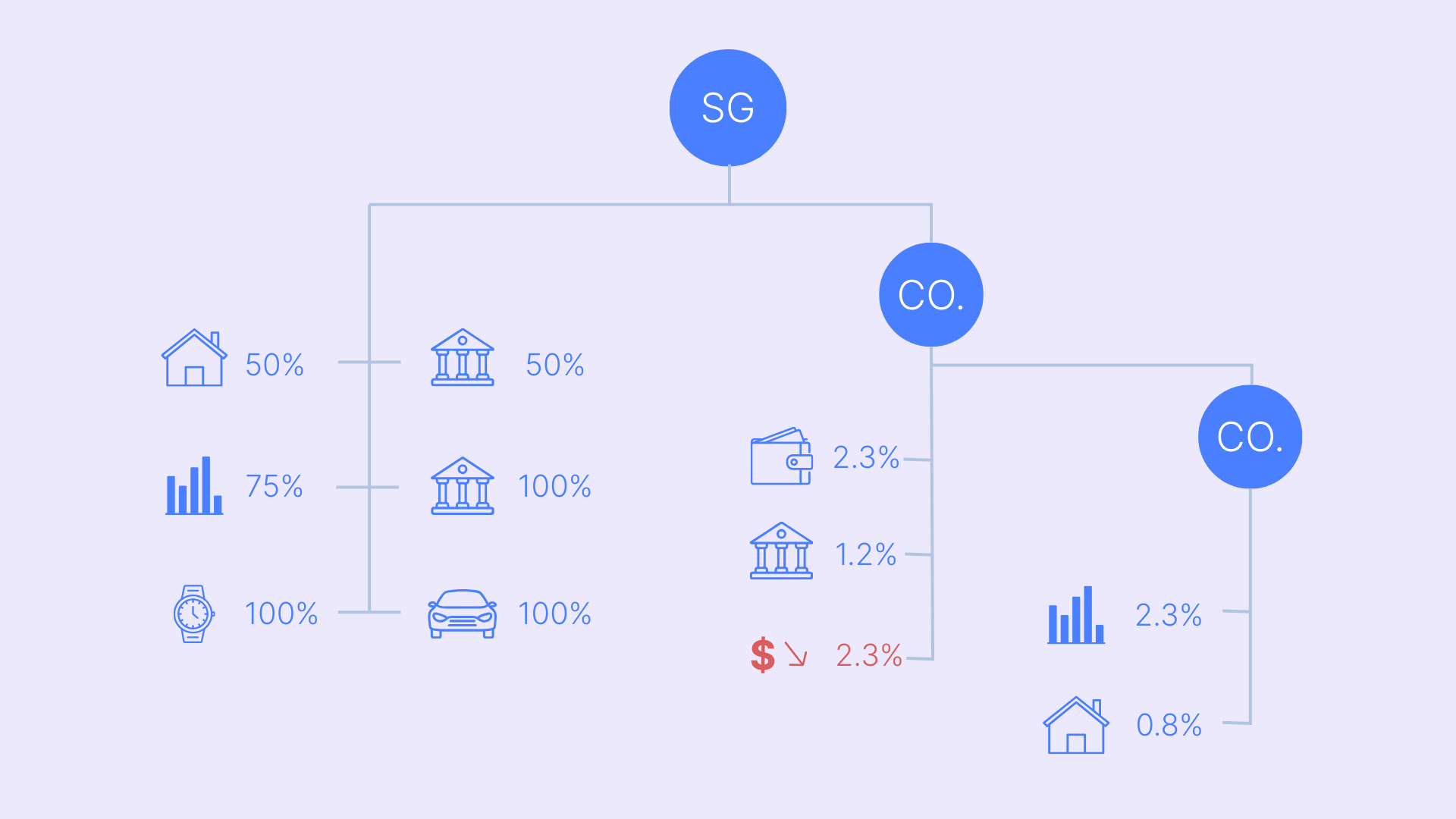

Then map the ownership structure. Use an entity/ownership map to chart trusts, special purpose vehicles (SPVs), and holding companies back to the ultimate owner. This visualization shows who owns what through which entities.

The Deliverable

A single owner-level view that shows positions, cash, liabilities, and key obligations. When a family member asks about net worth or a specific asset, you pull up one screen. That’s all.

This is foundational for every other family wealth planning strategy. You can't plan wealth transfer, calculate performance, or make asset allocation decisions without knowing what you actually have.

2. Liquidity Ladders and Buffers

Private equity and venture capital commitments can create uncertain cash timing and sizing. A capital call arrives with a two-week deadline, and you're scrambling to identify funding sources. Or worse, you risk default interest, penalties, or even forfeiture provisions under the LPA, and may harm future allocation opportunities.

Meanwhile, grown children are receiving distributions from trusts, insurance policies need premium payments, and estate taxes might come due. Without a forward view of cash needs, you're either holding too much idle cash (drag on returns) or too little (forced asset sales at bad times).

The Strategy

Register all commitments, including unfunded commitments, in one place. Build a liquidity ladder that shows cash requirements for the next 6, 12, 18, and 24+ months. Flag upcoming capital calls early. Track distribution expectations from mature funds.

Export a short liquidity snapshot that principals and the investment committee can review monthly. This makes cash management strategic instead of reactive.

The Deliverable

A rolling liquidity view tied to commitments and near-term needs. You know what's coming, what buffers you're maintaining, and when you might need to adjust public market positions or credit lines.

This supports both family wealth preservation strategies (avoiding forced sales) and family wealth growth strategies (deploying capital efficiently to private markets).

3. Performance Clarity the IC Will Read

You get quarterly performance numbers from your wealth advisors and investment managers, but they don't tell you why performance changed.

- Was it market movement?

- New contributions?

- Currency swings?

- Fees?

The investment committee needs to understand what's driving returns across different asset classes to make allocation decisions. But stitching together custodian reports, private equity valuations, and business appraisals takes days.

And by then, the numbers are outdated.

The Strategy

Calculate Time-Weighted Return (TWR) to evaluate portfolio/manager performance. Use IRR (money-weighted) to assess private investments and owner-level outcomes where cash flows materially affect results.

Show month-to-month changes, break down by market/income return, fees, FX, and cash flows, with valuation lag disclosed for private assets.

This attribution explains what happened in clear terms.

Save a "review-flags" view that highlights movements worth attention—positions that dropped significantly, sectors with outsized gains, or funds approaching exit windows.

The Deliverable

Performance reports your investment committee (or family council) actually reads. These are focused views that answer: What changed? Why? What needs discussion?

This enables informed investment decisions and supports family wealth management strategies that adapt to market conditions.

4. Mandate, Limits, and Cadence

Many families operate without written investment policies. The principal has general guidelines in mind, but they're not documented or consistently applied.

This creates problems when involving family members or working with multiple advisors. Different people interpret conservative differently. Concentration limits exist in someone's head but not in writing.

The Strategy

Write the investment mandate clearly: return objectives, risk tolerance, time horizon, and any values-based exclusions (tobacco, weapons, whatever matters to your family). Define concentration limits by asset class, individual position, manager, and geography. Set cash thresholds for liquidity buffers.

Store this policy document and link it to your dashboards and reports. When the investment committee reviews performance, they see the policy alongside actual positions.

The Deliverable

A concise policy summary backed by a full IPS, with review dates and version control. Everyone (family members, investment managers, financial advisors) refers to the same written standard.

This supports family wealth plan strategies by providing a governance structure and clear accountability.

5. Private Assets Register and Valuation Cadence

Alternative investments are notoriously hard to track. You've got commitments across 25 private equity funds, each with its own partnership agreement, capital call schedule, and valuation methodology. Documents arrive by email or are available on portals, valuations update quarterly (or not), and calculating total exposure requires rebuilding spreadsheets.

You can't answer basic questions: What's our total committed versus contributed capital? Which funds are calling soon? What's our overall private markets performance using pooled IRR (defined), TVPI/DPI, and PME versus a public benchmark?

The Strategy

Store all private asset data in one register:

- Commitments

- Calls

- Distributions

- Valuation dates

- Reported net asset value (NAV) or fair value

Link the Limited Partnership Agreements (LPAs), side letters, and capital account statements to each holding.

Track interim valuations with clear provenance: date received, source, methodology. This prevents confusion about which number is current. For co-investments and follow-on tranches, maintain separate records with their own performance tracking.

The Deliverable

An alternatives register that keeps numbers and documents together. When discussing a private equity position, you see the reported NAV or fair value (with valuation date and reporting lag clearly shown), historical IRR, unfunded commitment, and can pull up the LPA with one click.

This is essential for family wealth growth strategies focused on private markets. You need visibility to make follow-on investment decisions and monitor manager performance.

6. Centralized Documents and Approvals

Critical documents live in lawyers' filing cabinets, accountants' folders, and email attachments. When you need a trust document, power of attorney (POA), or operating agreement, you're hunting through shared drives or asking advisors to resend files.

Decision rights are unclear. Can the trustee approve a distribution? Does selling business interests require all family members or just voting shareholders? These questions should have documented answers, but often don't.

The Strategy

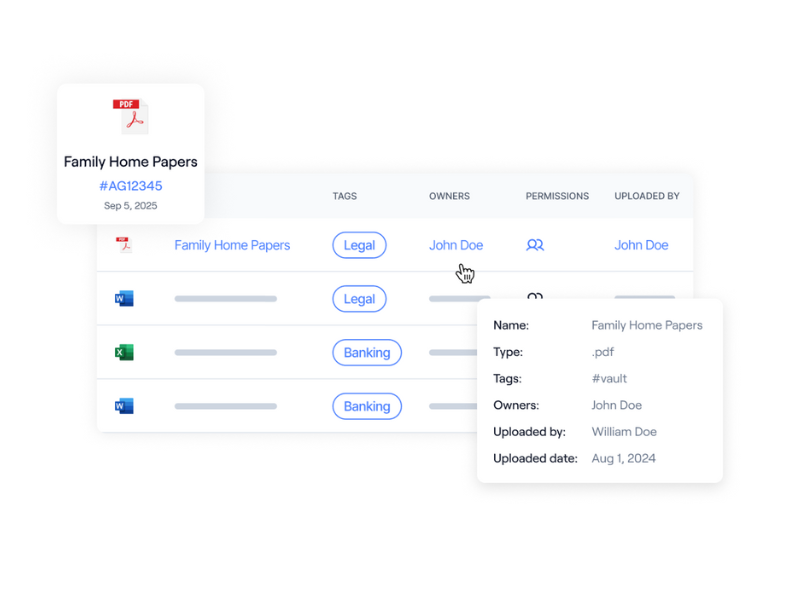

Keep trusts, wills, POAs, and governance charters in one secure digital vault. Link them to the relevant holdings and entities so the context is immediate. Store your family office governance structure alongside operational documents.

Record decision rights clearly:

- Who owns what

- Who can approve transactions

- What thresholds require board consent

Document signatory requirements and escalation paths.

Use workflow templates for recurring needs like annual trust filings, insurance renewals, and valuation updates. This turns ad hoc fire drills into scheduled, trackable processes.

The Deliverable

A clear decision matrix and an always-findable document dossier. Anyone with appropriate access can locate what they need in seconds.

This supports both family office operations and asset protection by ensuring proper documentation, signatory authority, and clear delegations of decision rights.

7. Reporting Rhythm That Sticks

Most families, apart from their regular quarterly/timely reports, generate reports reactively—that’s usually when someone asks for them. This means scrambling to compile data, inconsistent formats across months, and different assumptions that make period-over-period comparisons meaningless.

Quarterly reports arrive weeks after quarter-end, when the information is stale, and opportunities are missed. Different family members get different versions, leading to confusion and family disputes over what's accurate.

The Strategy

Establish a consistent reporting rhythm:

- Monthly owner snapshots for principals

- Quarterly deep dives for the investment committee

- Scheduled exports for wealth managers and advisors who need specific slices

Save these views as templates so reports pull current data automatically. Include a short note on assumptions with each report: valuation dates, FX rates used, anything that affects interpretation.

Following family office reporting best practices means standardizing reports while allowing customization for different audiences.

The Deliverable

A consistent reporting pack with the right level of detail for each audience. Principals get high-level wealth summaries. Investment committees get performance attribution and concentration views. Advisors get the specific asset class or entity data they need.

This supports family wealth transfer strategies by ensuring all stakeholders see consistent information.

8. Risk and Concentration at a Glance

Hidden concentrations create risk. You think you're diversified, but actually 40% of your portfolio is exposed to technology through direct holdings, funds that overweight tech, and business interests in software companies.

Manager concentration is another blind spot. That great emerging markets manager handles your EM equity sleeve, two hedge funds, and advises on a direct deal. Suddenly, one firm represents 15% of assets, more than you'd knowingly accept.

The Strategy

Visualize exposure by sector, manager, issuer, and currency. Create concentration dashboards that aggregate across all holdings, and, where possible, use look-through where transparency exists (public funds/SMAs), and rely on manager exposure reporting or risk models where it doesn’t.

Flag outsized positions automatically based on your policy limits. Drill down to supporting transactions and linked documents when investigating.

The Deliverable

A concentration dashboard that speeds rebalancing discussions. The investment committee can see precisely where risk is accumulating and make adjustments before concentrations become problems.

This supports family wealth preservation strategies by managing downside risk across the portfolio.

9. Accounting Alignment

Performance reporting and accounting often use different numbers for the same holdings. Your wealth manager says the portfolio is up 8%, but your accountant's records show different unrealized gains. Reconciling takes hours and breeds mistrust in the data.

Tax reporting requires cost basis and lot-level detail that performance systems don't track. You're maintaining parallel records that never quite match.

The Strategy

Maintain cost basis, tranche, and lot details, and realized and unrealized gains in one place, linked to source transactions and reconciled to custodian statements for full traceability. Track purchases by lot with acquisition dates to ensure cost basis calculations are defensible.

Keep period consistency across performance and reports. The same valuation date and FX rates flow through to all outputs.

The Deliverable

Accounting-ready positions designed to reconcile to custodians and performance reports via your existing accounting processes. When your CPA asks for cost basis or realized gains, you export clean data.

This is critical for tax-efficient strategies and estate planning. Cybersecurity matters here, too, because your financial data needs proper protection.

10. Education and Next-Gen Engagement

The next generation shows limited interest in family wealth because they lack access to information. By the time they inherit assets, they lack the financial acumen to manage them. This can contribute to the governance and capability gaps that often undermine multi-generational wealth.

Throwing them into investment family meetings without context doesn't work. They need progressive education that builds financial responsibility over time.

The Strategy

Export short learning documents: glossary of terms, dashboard guides, "how to read" notes that explain IRR versus TWR, or how to interpret sector allocation.

Give younger family members mobile access with Multi-Factor Authentication (MFA), role-based access controls, and periodic access reviews so access expands gradually and remains secure. They can check portfolio performance, view high-level allocations, and gradually understand the family's wealth structure without prematurely accessing sensitive details.

The Deliverable

A paced curriculum and secure on-the-go access. Education becomes ongoing, not a one-time conversation. As younger family members demonstrate financial acumen, you grant deeper access to financial information.

This supports family wealth succession strategies and prepares future generations to preserve inherited wealth.

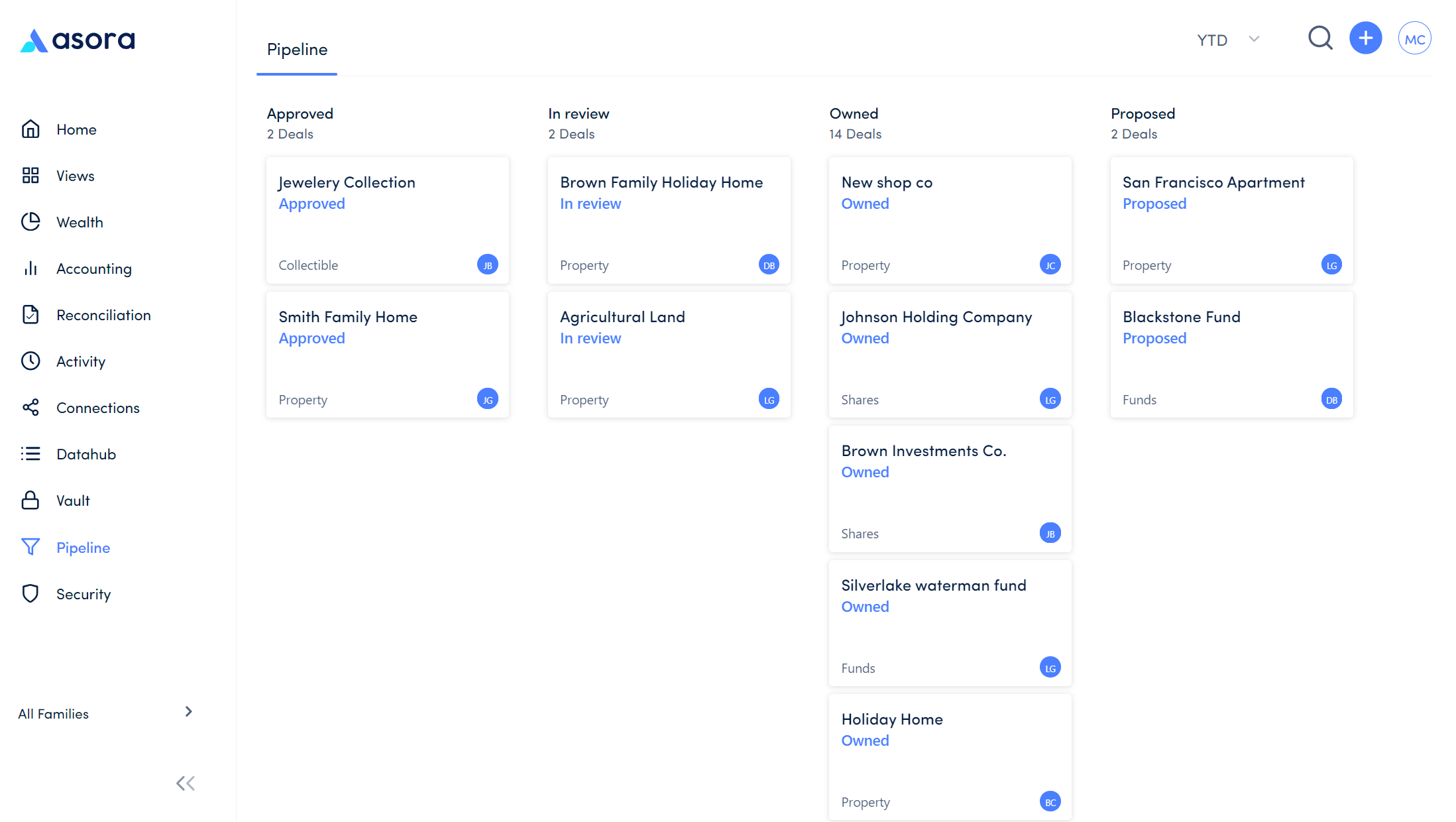

11. Pipeline and Follow-on Discipline

New investment opportunities arrive constantly. Some require quick decisions. Without tracking, you lose sight of what's under review, who's evaluating it, and what follow-on cash might be required.

Follow-on investments in existing holdings get particularly messy. That Series A company is raising a Series B. You want to maintain ownership, but did you reserve capital? Is it in the liquidity ladder? What does the original investment memo say about follow-ons?

The Strategy

Track new commitments and co-invests in a light pipeline. Assign ownership for due diligence, set decision deadlines, and link supporting documents, such as memorandums, management presentations, and reference calls.

Keep tranche IDs for follow-on investments tied to the original position. Note post-close tasks: document collection, account setup,and first capital call timing.

Flag follow-on cash needs early in your liquidity ladder (Strategy 2) so they're incorporated in cash planning.

The Deliverable

A light pipeline tied to cash pacing and documents. You track opportunities through evaluation and closing without drowning in email threads or losing critical files.

This supports family wealth growth strategies by creating disciplined investment processes.

12. Collaboration Without Email Sprawl

Working with multiple advisors creates communication chaos. Your wealth manager sends performance reports by email. The tax advisor requests cost basis via a separate thread. The estate planning attorney needs trust documents. Everything's scattered across inboxes and attachments.

Advisors work from different data sets and assumptions, leading to conflicting advice. You're the hub trying to keep everyone aligned, which doesn't scale as wealth and complexity grow.

The Strategy

Save report views and automatically schedule exports under controlled permissions, with audit logs and clear valuation dates/assumptions to prevent version drift. Your wealth manager gets monthly performance reports. Your accountant receives quarterly transaction details. Everyone sees consistent information on their schedule.

Enable secure external uploads of statements and notices to your centralized storage. Advisors can submit documents directly to your system instead of emailing sensitive information.

When evaluating family office software providers, prioritize platforms that support controlled sharing with appropriate security.

The Deliverable

A controlled intake and sharing loop with clear provenance. You know which advisor has which information, when they received it, and what version they're working from.

This reduces operational burden and improves coordination across your advisory team.

How Family Office Wealth Management Strategies Run in Asora

These twelve strategies require operational infrastructure. Here's how Asora supports each one:

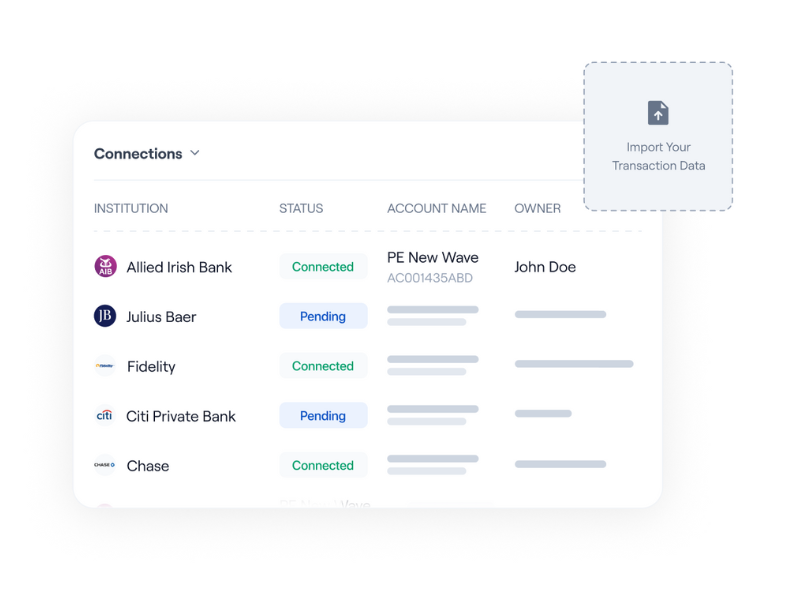

- Data Aggregation: Pull timely feeds from multiple banks and custodians. Standardize transactions such as contributions, distributions, fees, performance allocations, dividends, and interest, with precise dates and currencies.

- Wealth Map: Chart ownership across trusts, SPVs, and holding companies. Link each asset, liability, and cash flow to the correct entity and ultimate owner.

- Private Assets: Track commitments, unfunded amounts, calls, and distributions. Record valuation dates and NAV. Link LPAs and side letters. Track co-invests and follow-on tranches to support family wealth growth strategies.

- Performance Monitoring: Calculate TWR, IRR, and MOIC. Show monthly changes broken out by flows, valuation, FX, and other factors. Flag shifts that affect strategies for preserving and growing family wealth.

- Accounting: Maintain cost basis, lots and tranches, and realized and unrealized gains. Keep period alignment across reports so valuations and performance stay consistent with your accounting records.

- Documents: Secure vault linked to holdings and entities. Store trusts, wills, governance charters, capital account statements, and appraisals. Enable secure external upload for advisor materials to support family wealth strategies.

- Workflows: Create tasks for capital calls, filings, valuations, and governance reviews. Assign owners and due dates. Attach notes tied to the holding to support family wealth plan strategies and cadence.

- Reporting: Filter by entity, manager, or vintage. Support family wealth strategies that principals, investment committees, or boards can scan. Reporting can either be done by up-to-date dashboards (live) or can be exported to PDF/Word

- Mobile with MFA: Quick checks on holdings, upcoming calls, notes, and saved views while traveling. Support timely decisions on preservation, growth, and transfer.

This infrastructure makes the difference between family wealth management strategies that exist on paper and ones that actually work.As complexity grows, automated and standardised reporting in wealth management becomes a major efficiency lever for many modern family offices

Put Your Family Wealth Strategy To Work

Building comprehensive family wealth strategies doesn't happen overnight. But you can make meaningful progress in three straightforward steps:

- Aggregate data and draw the ownership map. Start with the data you already have. Import your spreadsheets/CSVs from banks, custodians and advisers. Then connect live feeds where available. From there, map ownership: show how trusts, entities and holding companies roll up to ultimate owners. Nail this single view of wealth first—it’s the foundation for everything else.

- Stand up the private assets register and liquidity ladder. Input your alternative investments with commitments, calls, distributions, and current valuations. Build your 6-24 month liquidity forecast. Now you've got visibility into your illiquid positions and cash needs.

- Save your monthly snapshot and export the first advisor reports. Create the reporting rhythm that keeps everyone aligned. Principals see high-level wealth. Advisors get their specific data cuts. Investment committees get performance attribution. Make these templates once, then they run on schedule.

From there, layer in the other strategies (concentration monitoring, accounting alignment, next-gen education, pipeline tracking) based on your priorities and complexity.

Some families wonder if this level of infrastructure makes sense for their situation. Consider the alternative: hours spent compiling spreadsheets, delayed decisions from incomplete data, younger family members unprepared for wealth transfer, and missed opportunities because you couldn't see the whole picture quickly enough.

Virtual family offices can work well, but they require tight governance, clear data ownership, and robust security and vendor controls. The key is to have systems that provide visibility and control, regardless of your operating model.

Ready to see how these family wealth management strategies work in practice? Request an Asora demo to see how Asora handles the operational backbone so you can focus on strategic decisions instead of data compilation.

FAQ

What are the most effective family wealth preservation strategies?

Effective preservation strategies include maintaining a consolidated view of all assets, building liquidity ladders to avoid forced sales, monitoring concentration risk across sectors and managers, and establishing transparent governance with documented investment mandates. Platforms like Asora help by linking documents to positions, mapping ownership across entities, and providing timely updates that support timely decisions.

How should families approach wealth transfer planning?

Successful wealth transfer starts with mapping the ownership structure, so you know which trusts, entities, and holding companies own what. Use tax-efficient vehicles such as trusts and strategic gifting while tracking ownership and documentation across these structures. Involve the next generation through education and appropriate access so they build acumen before inheriting.

What role does technology play in family wealth management strategies?

Technology provides the operational backbone: it aggregates data across custodians, calculates performance, tracks private asset commitments, visualizes ownership structures, generates reports, and maintains secure document storage. Asora supports this by storing and linking documents, tracking cost basis and lots, and exporting owner-level snapshots on a scheduled cadence so decisions are based on consolidated data.

How do you balance wealth growth strategies with wealth preservation?

Balance comes from clear investment mandates, liquidity planning, and concentration monitoring. Allocate to growth assets within documented limits, maintain liquidity buffers to fund commitments without forced sales, and use concentration dashboards to ensure growth does not create outsized risks. Strong governance helps align different risk preferences across the family.

.png)