TL;DR

Learn how to calculate NAV for private assets. This guide walks through the 10-step process family offices use for private equity, venture capital, real estate, and other illiquid investments, and shows how Asora centralizes valuations, source documents, and capital activity for audit-ready reporting.

The Challenge of Valuing Private Investments

If you manage a family office with private investments, calculating NAV isn't as simple as pulling a quote from Bloomberg. Private equity, venture capital, real estate, private credit, and direct investments don't have daily market prices. You need to construct the NAV from various sources, including fund manager reports, appraisals, capital account statements, loan schedules, and your own records.

Most mutual funds calculate NAV daily using market prices for liquid securities. The NAV formula for a mutual fund is straightforward: take the fund's assets (stocks, bonds, and cash equivalents) at their current market value, subtract the total liabilities (expenses, borrowed capital, and accrued fees), and divide by the number of outstanding shares. Exchange-traded funds and closed-end funds follow similar approaches, though their share price may trade at premiums or discounts to NAV.

But how do you calculate NAV when your assets don't have readily available market prices? When your private equity fund reports quarterly, but you need a monthly NAV? When real estate appraisals are annual, but you want current valuations?

This guide provides a 10-step framework for how to calculate the NAV of your private asset portfolio, plus checklists for data requirements and quality controls.

Why Calculating Net Asset Value (NAV) Is Different for Family Offices

The calculation of NAV for family offices differs from calculating the NAV of mutual fund portfolios in several key ways.

Working definition: Net asset value (NAV) represents the fair value of all assets owned by a fund, entity, or portfolio minus all liabilities and accrued expenses. For family offices, this encompasses not only liquid holdings but also private equity, venture capital, real estate, private credit, collectibles, and direct investments across multiple entities and structures.

NAV reflects the current economic value of what you own, providing a snapshot for performance measurement, decision-making, and reporting to stakeholders. How NAV is calculated matters because it drives reported wealth, informs allocation decisions, and supports the evaluation of investment performance.

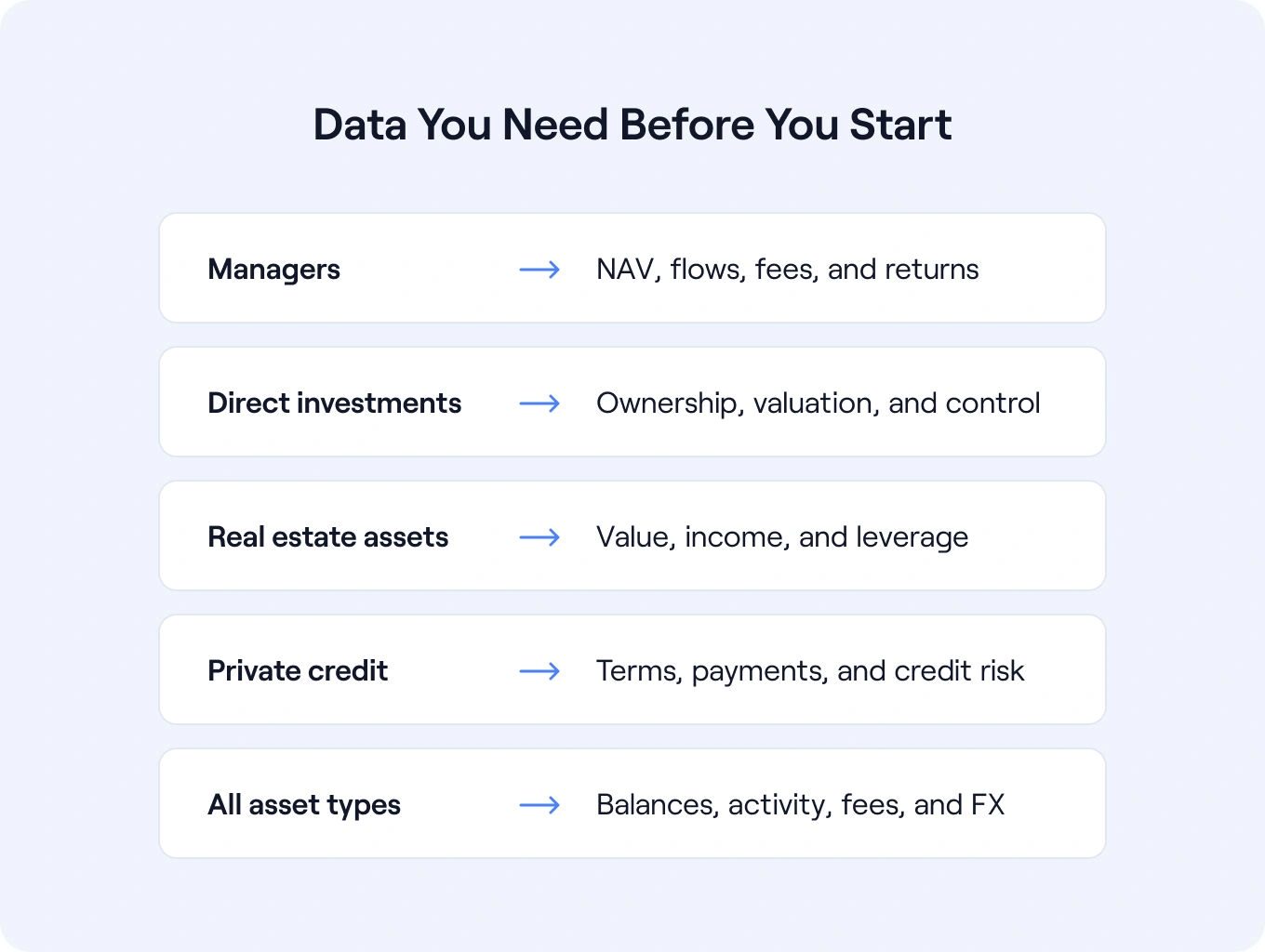

Data You Need Before You Start

Before calculating NAV, gather the following for each investment and entity:

From managers (private equity, venture capital, hedge funds):

- Latest capital account statements showing opening NAV, contributions, distributions, income, expenses, fees, and closing NAV

- Quarterly or annual fund financial statements

- Side letters documenting fee terms if different from standard

- K-1s or equivalent tax documents

For direct investments:

- Cap tables showing ownership percentages

- Latest financial statements or management reports

- Board-approved valuations, if available

- Supporting analysis for valuation (comps, DCF models, transaction multiples)

For real estate:

- Current appraisals (or most recent with documented roll-forward methodology)

- Rent rolls and operating statements

- Debt schedules showing loan balances, rates, and maturity dates

- Property tax assessments

For private credit:

- Loan agreements documenting terms, rates, and covenants

- Borrower financial statements

- Payment history and any restructuring details

- Credit risk assessment or rating

For all asset types:

- Opening balance from prior period NAV calculation

- All transactions during the period (capital calls, contributions, distributions, purchases, sales)

- Management fee terms and accrual calculations

- Performance fee structures (preferred returns, catch-up, carry percentages)

- Unfunded commitment amounts

- FX rates, sources, and timing for foreign currency assets

- Supporting documents (appraisals, financial statements, valuations, agreements)

- Prior approvals for valuation methodologies and significant adjustments

Having this data organized before starting makes the NAV calculation process significantly faster and more accurate.

How to Calculate NAV for Private Assets

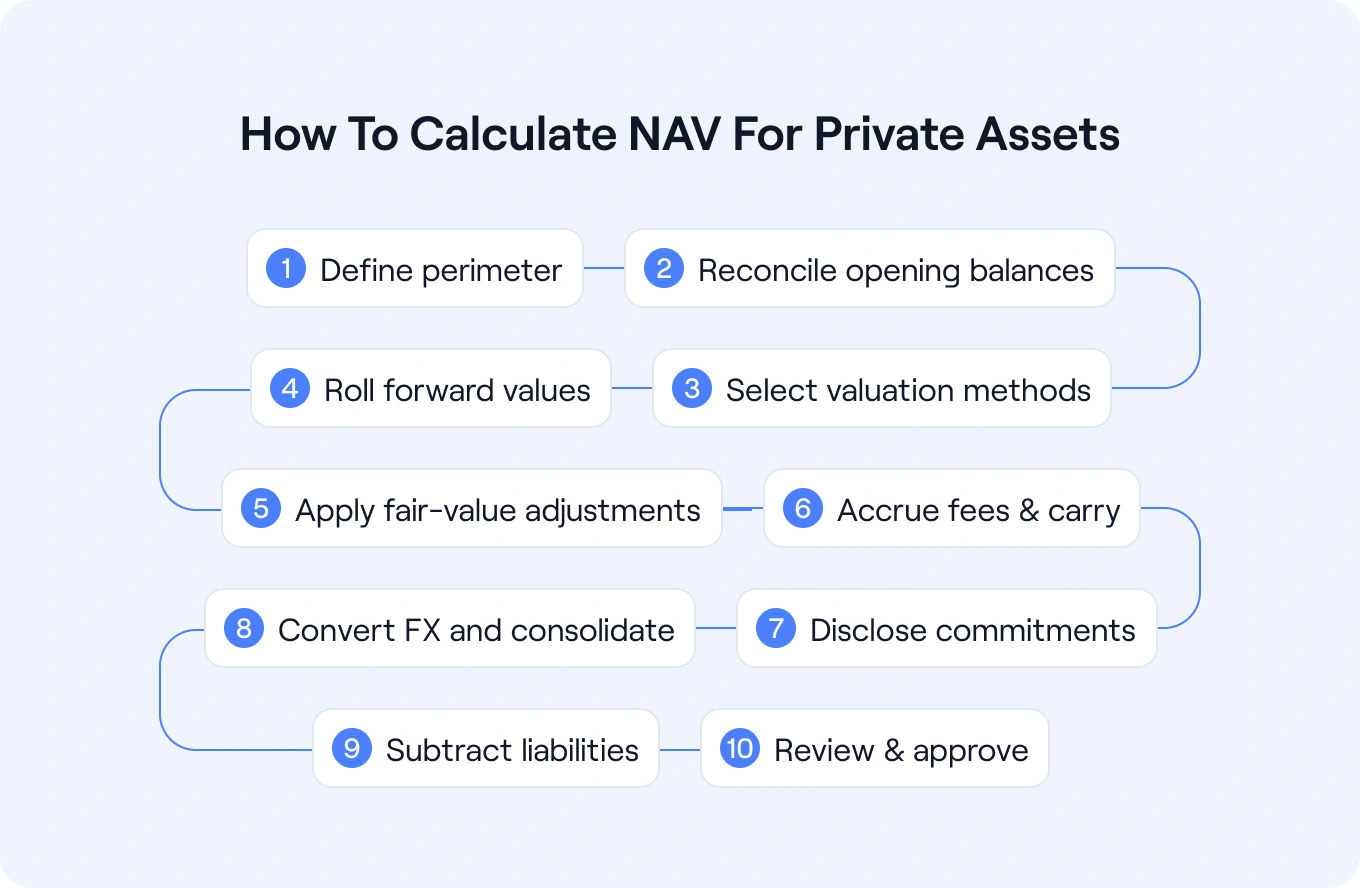

Here's how to calculate a NAV systematically, from defining scope through final approval.

1. Define the Perimeter & Valuation Date

Start by clarifying what the NAV will cover. Identify which entities, SPVs, and trusts are included, and note whether you’re calculating for a single entity, a consolidated family view, or specific portfolios.

Document how these entities connect. Indicate which are consolidated, which follow the equity method, and where look-through applies for beneficial ownership. This helps prevent overlap or missing assets.

Set the valuation date: this is the cut-off for including transactions and applying market values. Most family offices use month-end or quarter-end reporting, with prices, foreign exchange rates, and positions taken as of the close of that day.

A well-defined perimeter and precise valuation date make the NAV consistent, traceable, and easier to explain.

2. Normalize & Reconcile Opening Balances

Start with the closing NAV from your prior calculation period. This becomes your opening balance.

Reconcile to source documents: Verify that your opening balance matches the closing balance of the prior period. If it doesn't, investigate and document the difference before proceeding.

Check book versus fair value: Ensure you're working with fair value (what assets could be sold for), not book value (historical cost). For private assets, fair value requires judgment but should reflect economic reality.

Identify timing gaps: If your last NAV was calculated as of September 30th and you're now calculating October 31st NAV, ensure you've captured all transactions in that gap period.

Tie-outs: Reconcile sub-ledgers (entity-level records) to consolidated totals. The sum of individual entity NAVs should equal the consolidated NAV after eliminating intercompany transactions.

This step prevents errors from propagating through your calculation.

3. Choose Nav Calculation Methods by Asset Type

How nav is calculated depends on the asset type. Document your approach for each category:

Private equity / venture capital:

- Last-round calibration: Use the price of the most recent funding round, adjusted for time and company performance

- Comparable companies: Apply valuation multiples from similar companies to the portfolio company's metrics

- Discounted cash flow: Project future cash flows and discount to present value (requires significant assumptions)

Real estate:

- Income capitalization: Divide net operating income by the appropriate cap rate for the property type and location

- Comparable sales: Use recent sale prices of similar properties, adjusted for differences

- Appraisal: Rely on professional appraisal, updated or rolled forward between appraisal dates

Private credit:

- Discounted cash flow: Model expected payments and discount at an appropriate rate reflecting credit risk

- Expected credit loss: For impaired loans, estimate the collectible amount based on collateral and borrower condition

Collectibles (art, wine, cars, etc.):

- Specialist appraisal: Use experts in the specific collectible category

- Auction results: Reference recent comparable sales at major auction houses

- Insurance valuations: Can provide a floor for replacement value

Document which method you're using for each asset and why. Consistency period-over-period matters unless facts change.

4. Roll Forward Capital Accounts & Cash Flows

Between formal valuations (quarterly fund NAVs and annual appraisals), build roll-forwards to estimate the current value.

Start with last reported NAV: Use the fund manager's reported NAV or appraised value as your baseline.

Add contributions: Capital calls, additional investments, capital improvements (for real estate).

Subtract distributions: Cash distributions, return of capital, property sale proceeds.

Adjust for estimated appreciation/depreciation: Use market indicators to estimate value changes:

- For private equity/VC: Industry benchmark returns, comparable company performance

- For real estate: Property market trends, comparable sales, rent growth

- For credit: Interest accrual minus any credit deterioration

Add income less expenses: Interest income, rental income, less property expenses, management fees, and other fixed costs.

The roll-forward provides an estimated current NAV, even when official reports are outdated.

5. Apply Fair-Value Adjustments for Fair Market Price

Sometimes you need to adjust valuations beyond mechanical roll-forwards.

Calibration since last event: If a venture investment was valued at $10M based on a funding round 18 months ago, but the company has underperformed projections while comparable companies have declined 30%, a downward adjustment may be appropriate.

Impairment indicators: Look for signs that carrying value exceeds fair value:

- Portfolio companies are missing milestones or burning cash faster than planned

- Real estate with declining occupancy or rent concessions

- Credit borrowers with deteriorating financial conditions

Sensitivity analysis: For significant positions, model how NAV changes under different scenarios. What if this property sells for 10% less than its appraised value? What if the subsequent distribution from this fund is delayed by a quarter?

Document the rationale for any fair-value adjustments with supporting analysis. These require reviewer approval before incorporation into NAV.

6. Account for Fees, Carry & Waterfalls

Private investment fees affect NAV and must be appropriately accrued.

Management costs: Typically charged quarterly on committed capital (early years) or invested capital (later years). Accrue pro rata even if not yet billed.

Performance fees (carried interest): Accrue when the investment has exceeded its preferred return threshold and catch-up provisions have been satisfied. Calculate based on current NAV and distribution waterfall terms.

Clawback provisions: Some carry is subject to clawback if later investments underperform. Consider whether the accrued carry is truly realizable or needs a reserve.

Administrative expenses: Accrue fund administration, legal, and other recurring costs even if invoices haven't arrived yet.

Accurate fee accruals prevent NAV inflation from being understated due to liabilities.

7. Recognize Unfunded Commitments & Contingent Items

How do you calculate nav when you have unfunded commitments to private funds?

Unfunded commitments are not liabilities for NAV purposes. They're contingent obligations disclosed separately. Don't subtract unfunded commitments from NAV.

However, present unfunded commitments clearly in reporting:

- Total committed capital

- Capital called to date (reflected in NAV as an asset)

- Remaining commitment (could be called in the future)

Other contingent items:

- Guarantees provided to portfolio companies

- Letters of credit supporting real estate loans

- Indemnification obligations from prior investments sold

These are disclosed as contingent liabilities and are not deducted from NAV unless a specific claim is probable and estimable.

8. Handle FX Conversion & Consolidation

For assets held in foreign currencies, use a consistent translation methodology.

Use valuation-date rates: Apply the appropriate FX rate as of your NAV valuation date. This ensures the NAV reflects current economic value.

Document sources: Specify your FX rate source (e.g., 4 PM London close from Reuters, daily ECB reference rates) and apply it consistently.

Show FX effect separately: In your roll-forward or movement bridge, break out the impact of FX translation from underlying investment performance. This helps stakeholders understand whether returns came from the investments or currency movements.

Consolidation adjustments: When consolidating multiple entities, eliminate intercompany transactions and balances to ensure accurate consolidation. Don't double-count assets or liabilities that exist within the family structure.

9. Subtract Liabilities & Accruals to Arrive at NAV

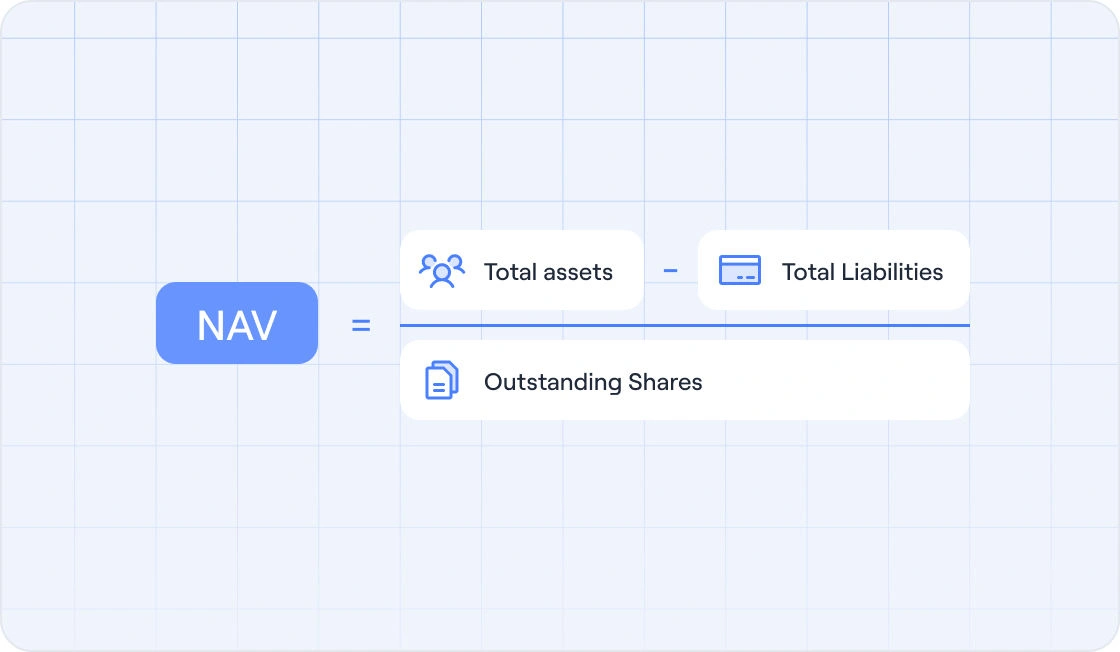

Now, calculate the final net asset value using the core nav formula:

NAV = Total Assets (at Fair Value) - Total Liabilities - Expenses

Total assets include:

- Cash and equivalents at financial institutions

- Liquid securities at market value (from custodian feeds)

- Private equity and venture capital at adjusted NAV

- Real estate at appraised or rolled-forward value

- Private credit at discounted expected value

- Direct investments at fair value

- Other assets (collectibles, personal property at appraised value)

Total liabilities include:

- Bank loans and mortgages (outstanding principal)

- Accrued interest payable

- Accrued management and performance fees

- Tax liabilities ( tax payable on realized and sometimes unrealized gains)

- Trade payables and other obligations

The result is your entity or consolidated NAV as of the valuation date.

Per-share NAV: If multiple investors own interests in a pooled structure, divide the NAV by the number of shares outstanding to determine the NAV per share or unit value. This is similar to how most NAV mutual funds present themselves—total net asset value divided by the number of shares.

10. Quality Checks, Approvals & Evidence Pack

Before finalizing NAV, conduct systematic quality controls.

Variance analysis: Compare the current NAV to the NAV of the prior period. Significant changes should have clear explanations:

- If NAV increased 15%, is that from contributions, investment returns, FX translation, or a combination?

- If a specific lower NAV decreases sharply, what is the driving factor?

Reviewer checklist:

- Are all source documents dated within the acceptable range of the valuation date?

- FX rates documented and from approved sources?

- Accruals calculated and reviewed?

- Unfunded commitments disclosed but not deducted?

- Roll-forwards for stale valuations documented with assumptions?

- Fair value adjustments approved by the designated reviewer?

Sign-offs: Obtain approval from designated personnel (e.g., CFO, CIO, or others as required by your governance) before distributing NAV to stakeholders.

Evidence pack: Assemble supporting documents and link them to specific holdings:

- Fund capital account statements

- Appraisal reports

- Loan schedules

- Fee calculations

- FX rate documentation

- Variance analysis

- Approvals

Workflows help manage this approval process systematically, ensuring that each step is completed before proceeding and that supporting documents are correctly linked to the calculations.

Tooling: Where Automation Reduces Risk

Calculating NAV manually in spreadsheets works until it doesn't. As portfolios grow more complex, automation reduces errors and saves time.

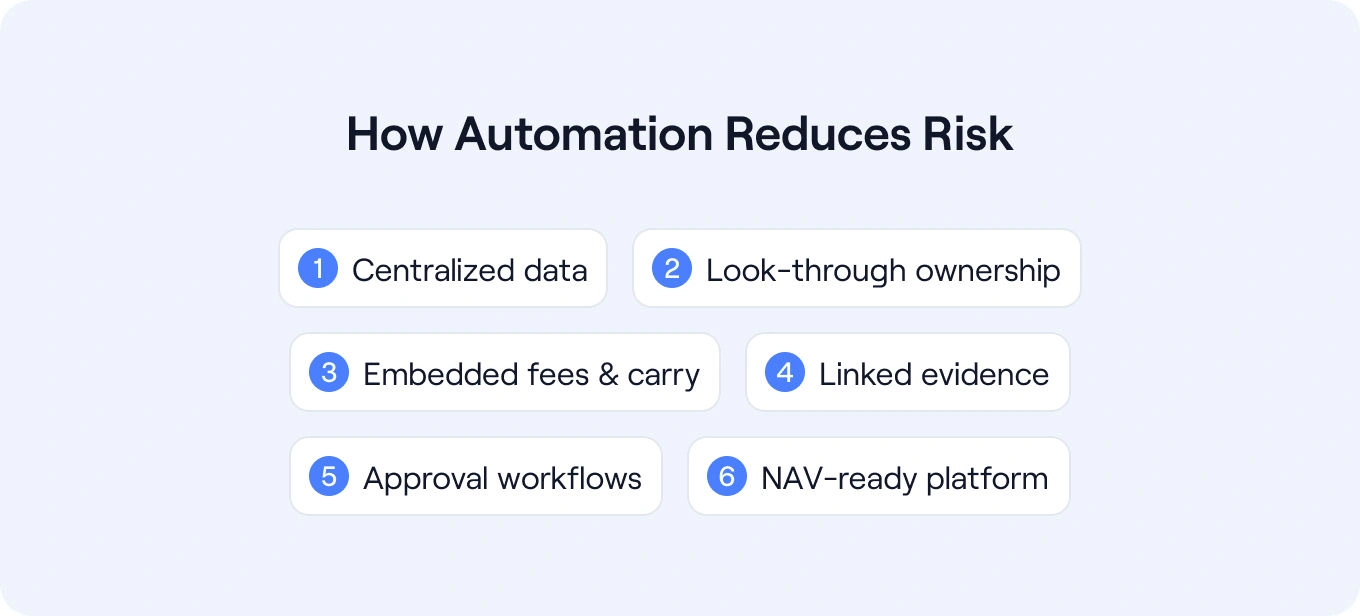

Centralized data for bankable and private assets: Data aggregation platforms connect to custodians for liquid holdings while providing structured templates for private assets. This eliminates manual data entry for the bankable assets, ensuring that all assets are accurately fed into NAV calculations.

Look-through structures: Understanding entity ownership matters when calculating consolidated NAV. Platforms that visualize ownership structures and automate look-through calculations help prevent errors associated with manual consolidation.

Capture fees and carry at holding level: Record fees, performance fee terms, and waterfall structures directly on each private investment. This enables automated accrual calculations, rather than relying on manual spreadsheet formulas that can break when new investments are added.

Evidence linking: Connect source documents (capital account statements, appraisals, loan schedules, fee letters) directly to the holdings they support. This eliminates the need to hunt through folders when reviewers request backup.

Approval workflows: Automate the review process by assigning tasks to specific individuals, tracking deadlines, and recording sign-offs to ensure seamless workflow. This prevents NAV from being distributed until it has undergone proper review and approval.

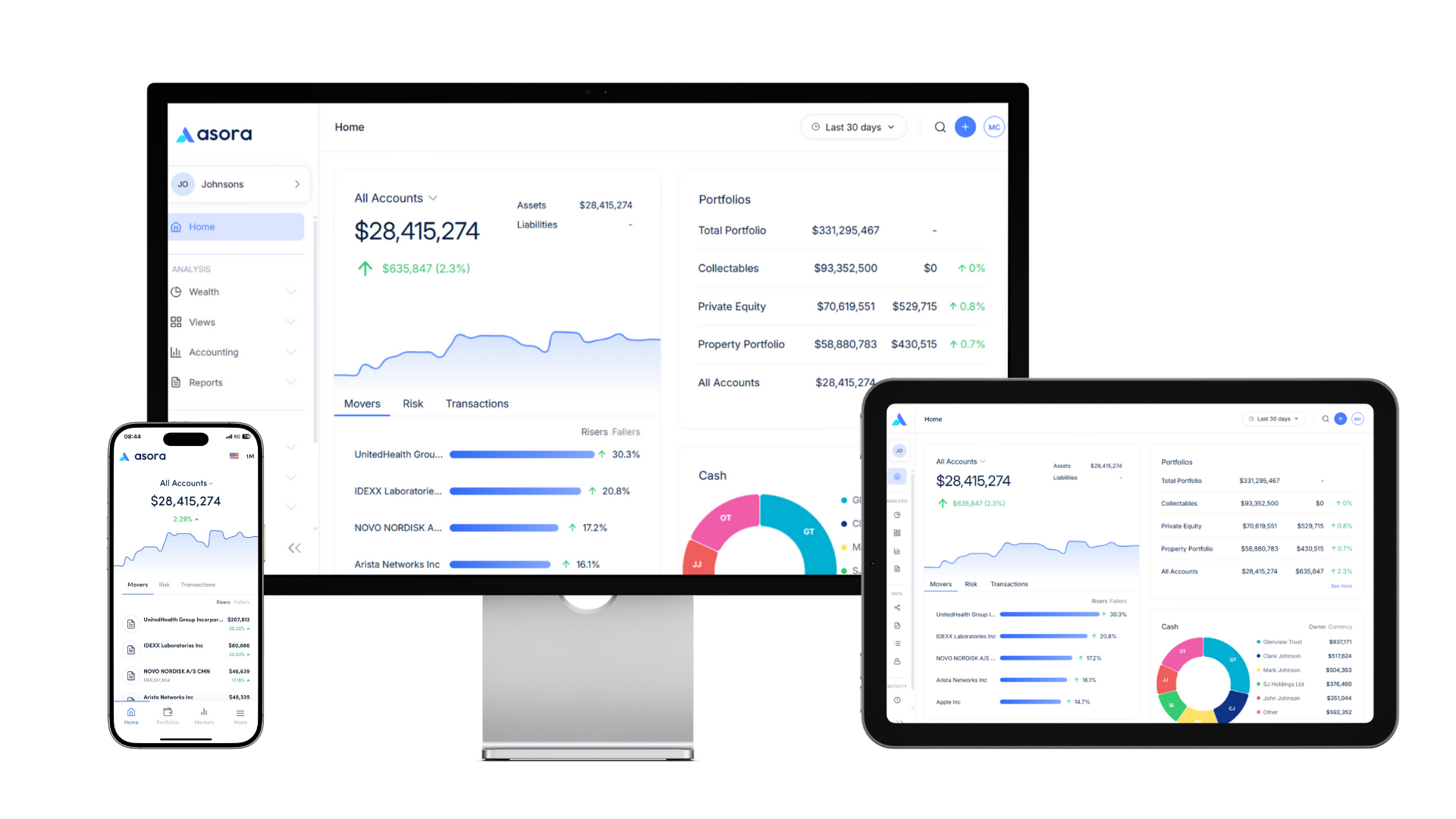

Asora capabilities for NAV calculation:

- Accounting : Track assets and liabilities, as well as income and expenses. Calculate NAV on demand for any entity or consolidated view.

- Private Assets : Maintain registers for PE/VC/credit/real estate with capital account roll-forwards, unfunded commitment tracking, and valuation methodology documentation. Link appraisals and fund statements directly to holdings.

- Documents : Store evidence packs with automatic linking to relevant holdings. Version control ensures a single source of truth that everyone is working from.

- Workflows : Assign NAV calculation tasks, set review deadlines, and track approvals.

- Mobile : Access current NAV from anywhere with secure, MFA-protected mobile access, allowing principals to check portfolio value without waiting for formal reports.

Make Better Investment Decisions with Asora

Calculating NAV for private assets requires a systematic process: gathering complete data, selecting appropriate valuation methods, rolling forward between formal valuations, accurately accruing fees and liabilities, consistently handling foreign exchange, and conducting quality checks before approval.

What matters: Consistency in methodology from period to period, complete data from every source, documented assumptions for roll-forwards and adjustments, and accurate accruals for all expenses. Keep these tight, and your NAV stays clean, defensible, and repeatable.

Why it matters: Accurate NAV drives portfolio decisions, performance measurement, and stakeholder reporting. Errors compound through downstream analysis. Inconsistent methodology prevents meaningful period-over-period comparison.

The outcome: Defensible NAV calculations that stakeholders trust. Faster monthly or quarterly closes are achieved because processes are well-documented and streamlined. Reduced risk of errors from manual calculations. Improved ability to answer questions about valuation because supporting evidence is organized and accessible.

The 10-step framework above works whether you're calculating NAV in spreadsheets or using dedicated software. As complexity grows, purpose-built platforms for family offices reduce manual effort while improving accuracy and controls.

See how Asora helps operationalize NAV calculation workflows: from data aggregation through private assets tracking to accounting and workflow management. Request a demo to explore how your structure could work in Asora.

FAQ

How is NAV calculated differently for mutual funds versus private investments?

Mutual funds use daily market prices for underlying securities. NAV equals assets at market value minus liabilities, divided by the number of shares outstanding, typically calculated once a day. Private investments lack daily pricing, so NAV relies on manager reports, appraisals, and roll-forwards between valuations. Exchange funds and closed-end funds follow approaches similar to those of mutual funds, while private equity, venture capital, and real estate investments require more judgment on methods and timing. Asora keeps mutual fund data current via aggregation and maintains private-asset records and documents for periodic updates.

What is the NAV formula?

The formula is: NAV = Total Assets at Fair Value − (Total Liabilities + Accrued Expenses). For per-share figures, divide by the number of shares outstanding. Assets include investments at current market value or fair value for private holdings, plus cash. Liabilities include debt, expenses, management costs payable, and taxes. Asora calculates performance and preserves a transaction history, along with documents that support each input to the formula.

How do you calculate NAV when valuations are stale?

Build a roll-forward from the last reported figure: start with the prior NAV or appraisal, add contributions and capital calls, subtract distributions, apply an estimated return using appropriate indicators, add income, subtract expenses, and document assumptions. For example, if a fund reported $10 million on September 30, you need an update for October cash flows by October 31, and you apply an estimated monthly return, then record the evidence. Asora captures the cash flows, links the benchmarks in not or document form, and produces an auditable roll-forward.

What is the difference between NAV and market price for investment funds?

NAV represents the intrinsic value of a fund’s holdings. Open-end mutual funds transact at NAV once per business day. ETFs and closed-end funds trade on exchanges, so the market price can be above or below NAV. Premiums and discounts create gaps between market price and intrinsic value. Managers control holdings that drive NAV, not the market price. Asora reports both portfolio values and position-level details, allowing you to compare intrinsic value, market movements, and realized performance in one place.

.png)