TL;DR

A family office net worth statement presents assets minus liabilities on a set date, by entity and by beneficial owner, as a repeatable process rather than a one-off spreadsheet. Net worth can be negative where liabilities exceed assets, typically due to leverage, recourse obligations, or large payable events (for example tax bills or called guarantees). With a fixed perimeter and valuation date, reconciled openings, and standardized valuation, FX, and cash-flow treatment, results stay comparable period to period. Evidence linked to each holding, clear recognition of fees and taxes, and consolidation with an explicit movement bridge keep the reports decision-grade. Asora supports a single source of truth, document linking, and fee/FX templates with workflow tasking; approvals and sign-off remain in the external process.

Why a Net Worth Statement Matters for Family Offices

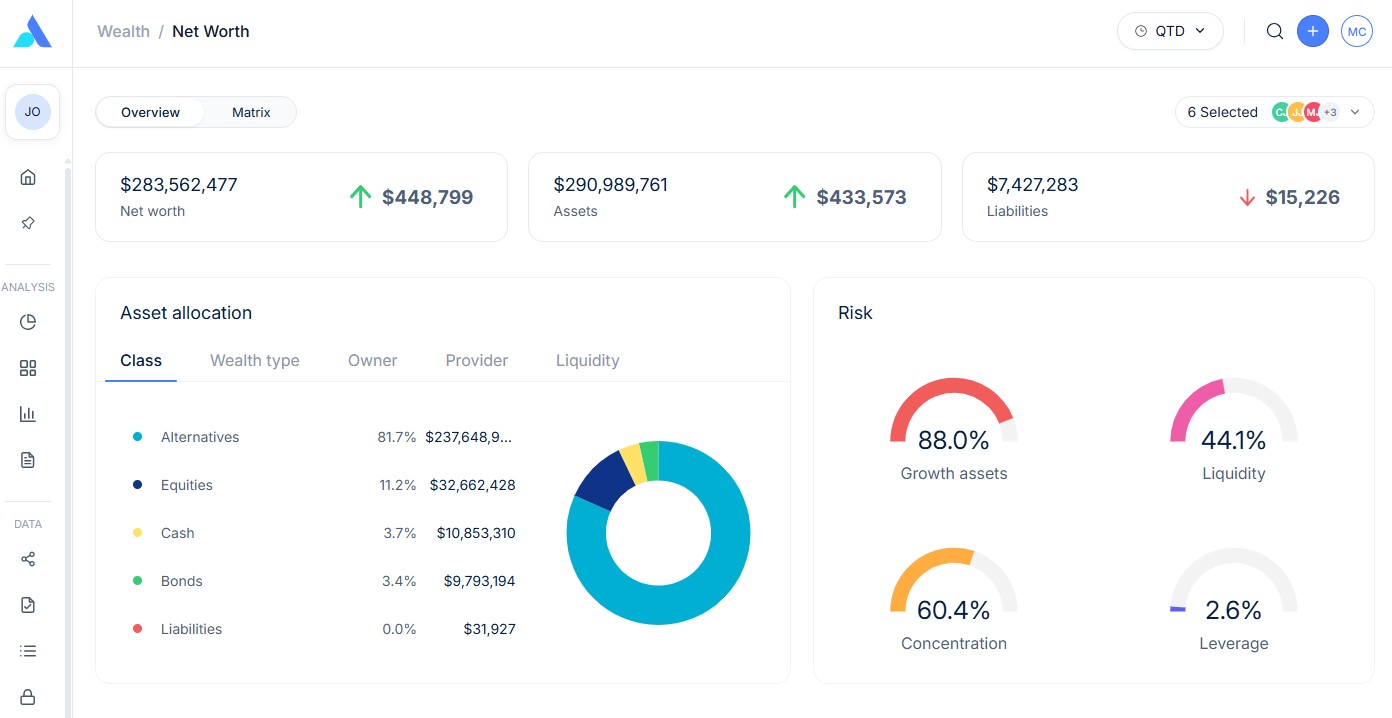

A family office net worth statement combines an entity ledger and an owner roll-up to present a clear financial position at a specific valuation date. The format supports discussions of allocation, liquidity, and risk while preserving traceability from headline numbers to source documents.

Scope discipline prevents overstatement. Unfunded commitments, guarantees, contingent items, and letters of credit are disclosed separately unless an obligation is probable and reasonably estimable, in which case, recognise it as a liability (and disclose assumptions). That treatment keeps market value visible while surfacing exposure. Repeatability delivers confidence, which is crucial for effective wealth building. A central holdings register, fixed FX sources, and a compact evidence file yield the same result each period, thereby strengthening financial literacy across stakeholders.

The guide below outlines how to create net worth in 10 practical steps, with notes on how Asora helps teams keep holdings, documents, and workflows organized.

What a Family Office Net Worth Statement Includes (and Excludes)

A sound statement begins with what is reflected on the balance sheet as of the valuation date. Cash in bank accounts and any money market account balances anchor liquidity. Listed holdings include mutual funds, exchange-traded funds, equities, and fixed income, as per custodian records. Private assets round out the picture, including PE and VC funds, direct equity, private credit, real estate, and SPVs. Loans receivable and other assets complete the asset side of the balance sheet. Liabilities and accruals are recorded in full. The headline figure is straightforward and precise: assets minus liabilities as of that date.

Not everything belongs inside the line. Items that influence cash planning or downside exposure are noted separately, not included in the total. Unfunded commitments to funds and co-investments are tracked for future calls. Guarantees and letters of credit signal potential strain under stress but are not current liabilities. Contingent claims receive the same treatment. Kept in disclosures, these items remain visible without distorting net worth.

Interpretation hinges on the unit of account. An entity view shows each company, trust, LP, or SPV separately, which suits lender tests and local filings. A consolidated view removes intercompany balances to present a single financial position for the group. A look-through view, then looks through wrappers, applies ownership percentages, and shows the investment portfolio as it is actually experienced. Where wrappers matter, use unitized reporting to compare like-for-like changes across tax-advantaged, tax-deferred, and pension accounts, isolating underlying performance and excluding wrapper effects.

Data You Need Before You Start

Preparation runs faster with a standard checklist. The list below supports lean teams without sacrificing control.

- Bank and custody statements for the valuation date

- LP statements and capital account roll-forwards

- Private valuations and appraisals

- Loan schedules and lender statements (mortgages, subscription lines, personal loans)

- Cap tables and shareholder agreements for direct holdings

- FX source files with valuation-date rates

- Fee schedules for management, admin, carry, and minimum payment logic

- Prior period tie-outs and the signed pack for openings

- Approvals document noting preparer, reviewer, and date

Asora stores holdings in a central register and links statements, appraisals, loan confirmations, and fee schedules to each position; view valuation dates, set a valuation frequency, and receive in-app alerts to update valuations on schedule. This structure streamlines reviews, facilitates audit support and review readiness by linking evidence and standardising workflows, and minimises manual risk, allowing the team to focus on building wealth and delivering precise reporting.

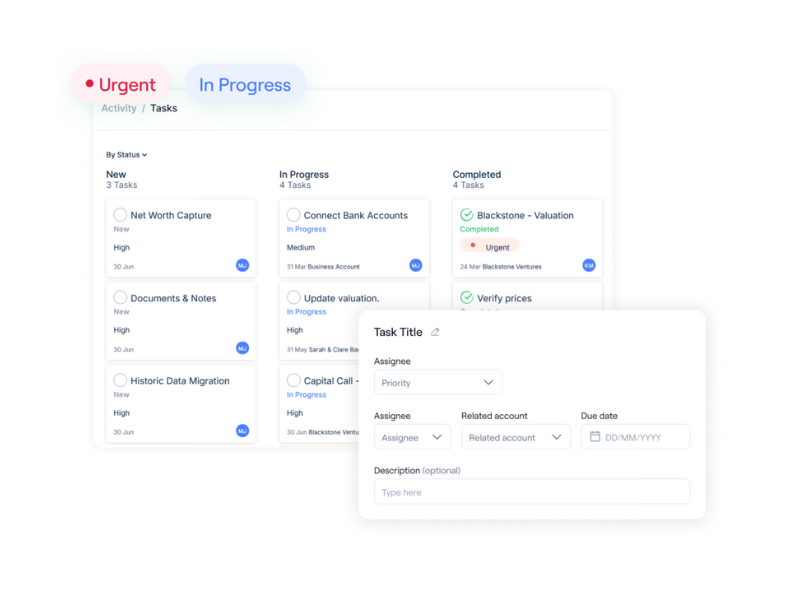

Build Once, Repeat Quarterly: The 10 Steps

This section outlines the 10-step sequence and flags where software reduces operational drag. The flow runs from scope control to reconciled openings, then data capture, valuation, and flows. It finishes with FX and consolidation, liabilities, quality checks, and archiving. Short, consistent steps make the report easy to read and simple to review.

1) Define Perimeter & Valuation Date

List entities, trusts, SPVs, and operating companies with consolidation rules. Set the valuation date and implement a cut-off policy for late statements and post-dated events. A clear scope prevents drift and protects comparability across periods.

2) Normalize & Reconcile Opening Balances

In today’s UI:

- store the prior signed pack in documents (tagged to the entity/period)

- on position → valuations, set the opening balance from that pack and link it

- record book vs fair value on the valuation line

- add a short footnote explaining the difference, and attach the relevant statement/appraisal/fee/loan evidence

- use tasks with a “period close” checklist to resolve timing items and replace estimates with finals before the roll-forward

- update the valuation number/date

- add any final footnotes

- keep all evidence linked so reviewers can trace each adjustment.

Asora stores a central holdings register and supports document linking at the holding level, so that historical data reports and supporting files are associated with each position. This standardizes preparation and speeds review, and eases audit preparation. Workflows provide tasking; approvals and reconciliation occur in the external process.

3) Capture & Validate Data for Each Asset Class

Gather positions, prices, and corporate actions for marketables and confirm against custodians. For PE and VC, collect capital accounts, calls, and distributions. For direct private assets and real estate, collate Discounted Cash Flow (DCF) models, last-round calibrations, appraisals, rent rolls, and market comps in Documents and link them to each position; in Valuations, expand the DCF (drivers, scenarios, sensitivities) and use the last round as an input—adjusting for terms (e.g., prefs/structure), time decay since the round, and current market conditions (growth, margins, cap rates); add a brief disclosure noting assumptions, data gaps, and limits of reliability, and set the valuation date/frequency so Tasks prompt timely updates.

For private credit, capture contractual cash flows, prepayments, and impairment indicators. Run quick reasonableness tests to ensure large movements reconcile to flows, valuation changes, or FX.

4) Select Valuation Basis by Asset Type

Apply methods consistently. Marketables take the valuation-date close. Private assets are typically valued using policy-based methods, including last-round calibration, comparable multiples, or discounted cash flow. For real estate, use an income/capitalisation approach, Net Operating Income (NOI) capitalisation with an implied cap rate, and triangulate results with independent appraisals and comparable sales, documenting any assumptions and cross-checks. Credit instruments often require DCF with expected credit loss indicators. Collectables rely on specialist appraisal and recent sales. Document the method and maintain a stable approach across periods.

5) Process Cash Flows & Corporate Actions

Post contributions, distributions, capital calls, dividends, interest, redemptions, splits, and FX cash. Tie back to notices and bank statements. Cross-custodian checks confirm positions across brokers. Accurate flows anchor the period-over-period bridge and support planning for unexpected, variable, and discretionary expenses at the entity level.

6) Apply Fair-Value Adjustments

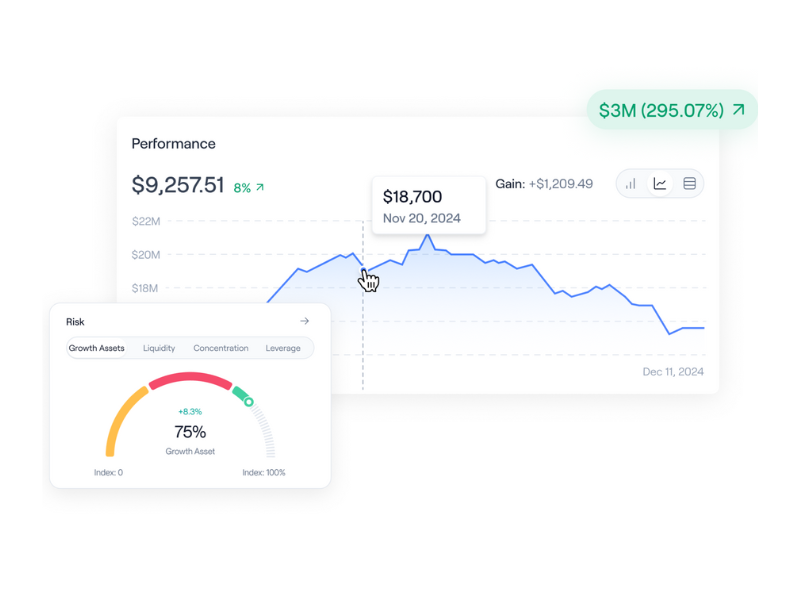

Assess assets without fresh transactions for impairment triggers or material uplifts. Refresh real estate inputs, including occupancy, rent growth, and discount rates. Review credit exposures for stress signals and covenant pressure. Add brief sensitivity notes where small parameter shifts could significantly alter the value. The aim is accuracy, not optimism.

7) Recognize Fees, Carry & Accruals

Accrue management fees, admin charges, and transaction costs. Apply carry/performance fee logic per governing documents; recognise carry/performance fees as liabilities only when crystallised or contractually payable; otherwise disclose an estimate and its basis, and flag any clawback mechanics. Estimate taxes payable with the tax advisor, considering tax advantages and any impact on taxable income. Where software helps in this step, Asora supports stored fee templates in document form, and governing docs at the holding level. Templates reduce spreadsheet drift, protect net worth accuracy (and related accruals), and improve comparability.

8) Handle FX Conversion & Consolidation

Translate to the presentation currency at valuation-date spot rates and show FX effects in the movement bridge; adopt spot-rate translation at the valuation date as the policy for net worth reports, and document any exceptions (e.g., specific non-monetary items or operating-company books). Eliminate intercompany receivables/payables, loans, and cross-holdings. Treat intercompany dividends consistently in the movement bridge (and ensure you are not double-counting).

Asora stores FX source files via document linking, so the same provider file, timestamp and methodology included, can be reused each period for comparability; you can also set custom FX rates, and the platform performs automatic conversions using the valuation-date daily rate from our exchange-rate provider.

9) Subtract Liabilities & Finalize Net Worth

Compile debt balances from mortgages, subscription lines, personal loans, and other borrowings, confirmed to lender statements. Include payables, fee accruals, and taxes payable. Compute the headline number as assets minus liabilities and present entity, consolidated, and owner views. Flag wrappers such as retirement accounts and retirement plans; include life insurance policies with cash value as other assets.

10) Quality Checks, Approvals & Evidence Pack

Start with variance by driver: flows, valuation change, FX, and other items. A concise reviewer checklist then confirms tie-outs, method consistency, and document sufficiency. Asora provides workflow support to track reviewer tasks and links supporting files to each holding, keeping evidence close to the numbers and speeding the next cycle. Approvals and sign-offs occur in the external process to preserve segregation of duties.

Reporting Views That Owners Actually Use

Entity, consolidated, and owner-level perspectives serve different purposes for decision-making. Lenders focus on entity covenants. Investment discussions rely on consolidated figures for allocation and risk assessment. Ownership structures are mapped in an entity/ownership map, while exposure by owner can be presented from the holdings register and look-through settings as part of the reporting pack.

Change matters as much as level. A movement bridge that separates flows, valuation changes, FX, and other drivers is a best practice for the pack. Asora supports this workflow by maintaining a central holdings register and linking valuation support to each position; teams compile the bridge itself as part of their reporting process.. Workflow support (tasks, pipeline tracking) helps track reviewer actions, while approvals and reconciliation occur in the external process.

Governance, Policy & Documentation

Governance sustains quality. Set valuation frequency and thresholds, with triggers for out-of-cycle updates. Separate preparer and reviewer roles. Maintain a change log for method and parameter shifts within the team’s process. Define evidence expectations so that every figure is tied to a statement, appraisal, or memo. Asora supports workflow tasking and document linking to keep work visible and evidence close to the holdings; approvals and reconciliation occur in the external process.

Tooling: Reduce Manual Risk Without Over-Engineering

A central holdings register reduces manual error risk without adding enterprise bloat. Asora’s Wealth Map provides look-through ownership, so exposure by owner can be presented without rebuilding models. FX consistency improves when source files are stored alongside positions; translation and the movement bridge are produced in the team’s reporting process. Linking evidence ensures reviewers can see the source files. Mobile access with MFA keeps stakeholders informed when away from the office.

Asora automatically aggregates bank and investment data into one live dashboard; it tracks private assets (private equity, real estate, trusts, alternatives) with valuations, cash flows, and linked evidence; it manages documents with secure storage, tagging, and links; workflows provide tasking and alerts to keep filings and reviews on schedule; and the mobile app offers secure, MFA-protected access to everything on the go.

Common Pitfalls (and How to Avoid Them)

- Mixing book and fair value in one column undermines clarity.

- Stale FX or prices distort outcomes.

- Unfunded commitments disappear without a dedicated note.

- Performance fee/carry logic drifts without templates.

- Missing a variance bridge weakens the narrative.

- Sparse evidence packs invite rework.

- Single-analyst spreadsheets create key-person risk.

- Vague perimeter definitions reduce comparability.

- A brief preventative checklist, embedded in the workflow and backed by linked documents and fixed FX sources, keeps these issues in check.

Broader Personal Finance Context

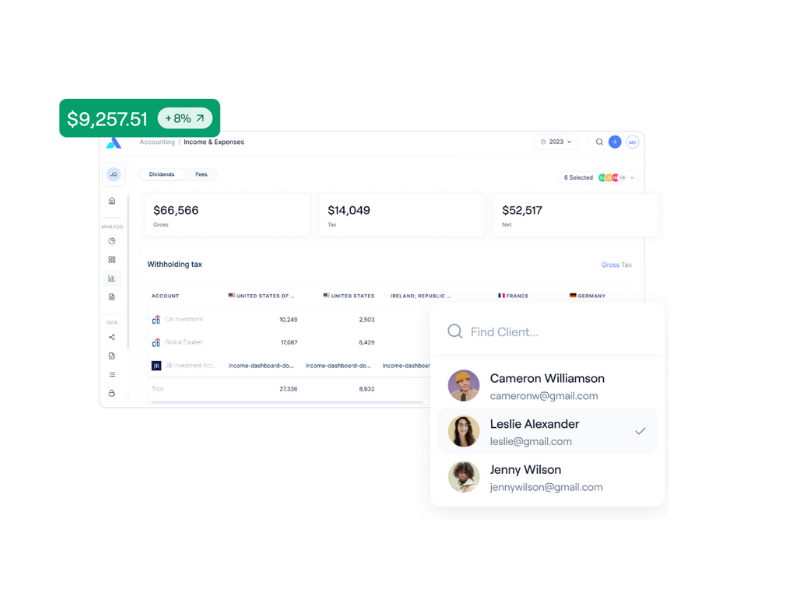

Family offices often field questions from future generations. Some terms intersect directly with a net worth statement. Investment accounts in taxable wrappers may hold mutual funds and exchange-traded funds. Retirement accounts and plans can change asset allocation and cash flow through tax advantages. A savings account, a high-yield savings account, or a money market account can serve as the anchor for an emergency fund.

Credit card debt, credit card balances, student loans, personal loans, and other high-interest debt can negatively affect a wealth-building journey; policies that prioritize paying off expensive balances often free more money for investing. Life insurance policies with cash value can sometimes be included among other assets in trust planning. Transparent reporting supports financial health, fosters stronger financial literacy, and leads to better financial decisions over time, which can be influenced by your spending habits.

Finalize, Evidence, and Sign-Off

Trustworthy reporting rests on four pillars: fixed perimeter and date, reconciled openings, consistent valuation and flow processing, and complete evidence. The result is a defensible net worth statement that informs allocation, liquidity, and risk decisions periodically. Asora helps by storing holdings in a central register, linking source evidence, standardizing fees and FX templates, and supporting workflow tasking. Approvals and sign-off remain in the external process. Asora offers a dedicated net worth dashboard.

Request a demo to see how a consolidated holdings register, linked documents, and consistent workflows reduce the risk of manual errors, help calculate your net worth, and keep the net worth reports decision-grade every quarter.

FAQ

What assets should be included when calculating net worth for wealthy families?

When calculating net worth for high-net-worth families, include all financial assets (equities, bonds, mutual funds, hedge funds, cash equivalents), private investments (private equity, venture capital, direct business interests), real property (primary residences, investment properties, land holdings), and tangible assets (art, jewellery, collectables, vehicles). Do not forget assets held through trusts, foundations, and multi-jurisdictional entities. Equally important is accounting for all liabilities: mortgages, credit facilities, tax obligations, and contingent liabilities. Advanced family office platforms enable comprehensive tracking by supporting asset classification and hierarchical, multi-entity reporting that consolidates individual holdings into a unified family balance sheet. Asora delivers this single, secure view across bankable and private assets, including linked documents and workflows.

How do you create a comprehensive net worth statement that includes private assets?

Creating a comprehensive net worth statement requires systematic data collection, consistent valuation methodologies, and secure centralization of information. Begin by cataloging all asset classes, from publicly traded securities to private equity investments, property holdings, and alternative assets. Each category requires appropriate valuation: market prices for liquid securities, appraisals for real estate, and fair-value assessments for private holdings. Purpose-built wealth platforms streamline this process by automating data feeds from banks and custodians, as well as providing a secure repository for private asset documentation.

How can family offices automate net worth reporting and maintain accuracy?

Family offices can automate net worth reporting by implementing integrated wealth platforms that connect directly to financial institutions and custodians through secure integrations (APIs and/or file-based custodian feeds, depending on institution). Automation eliminates manual entry errors and ensures that valuations remain up-to-date. Choose platforms that automate bankable assets and track private assets with built-in tasking (checklists, reminders, evidence links) for periodic valuations. Look for configurable reporting templates and consolidated views across complex entity structures. Security certifications such as ISO 27001 are essential. Asora meets these needs with automated aggregation, workflows, multi-entity consolidation, and independently audited against ISO 27001-aligned ISMS standards.

What are the common challenges in net worth calculation for complex family wealth?

The primary challenges include data fragmentation across multiple institutions, inconsistent private asset valuations, managing multi-entity structures, ensuring data security, and maintaining current information without excessive manual effort. Illiquid assets such as private equity and collectibles are hard to value due to infrequent pricing. These challenges are addressed by centralized platforms that aggregate diverse data sources and provide secure document storage and workflow management. These challenges are solved by clear valuation policies, scheduled review cycles, and role-based access controls that keep work consistent and secure.

.png)

.png)