TL;DR

Liquid wealth management is more than holding cash. Family offices need a policy-driven system that categorises liquidity by time-to-cash, considering settlement, gates, and restrictions, in coordination with illiquid assets and long-term objectives. With Asora, teams can tag liquidity tiers, view consolidated cash and runway alongside commitments and upcoming calls, and align actions with policy. Result: stronger flexibility, a deeper safety net, and steadier cash flow.

Why Liquidity Is a Strategic Lever for Family Offices

Liquidity is more than holding cash. A policy-led system defines which liquid assets to hold, how to calculate liquid net worth, and how to tier liquidity across checking and savings accounts, money market funds, treasury bills, and other cash equivalents, while coordinating with illiquid assets and long-term goals. Done well, the payoff is stronger flexibility, a deeper safety net, and steadier cash flow.

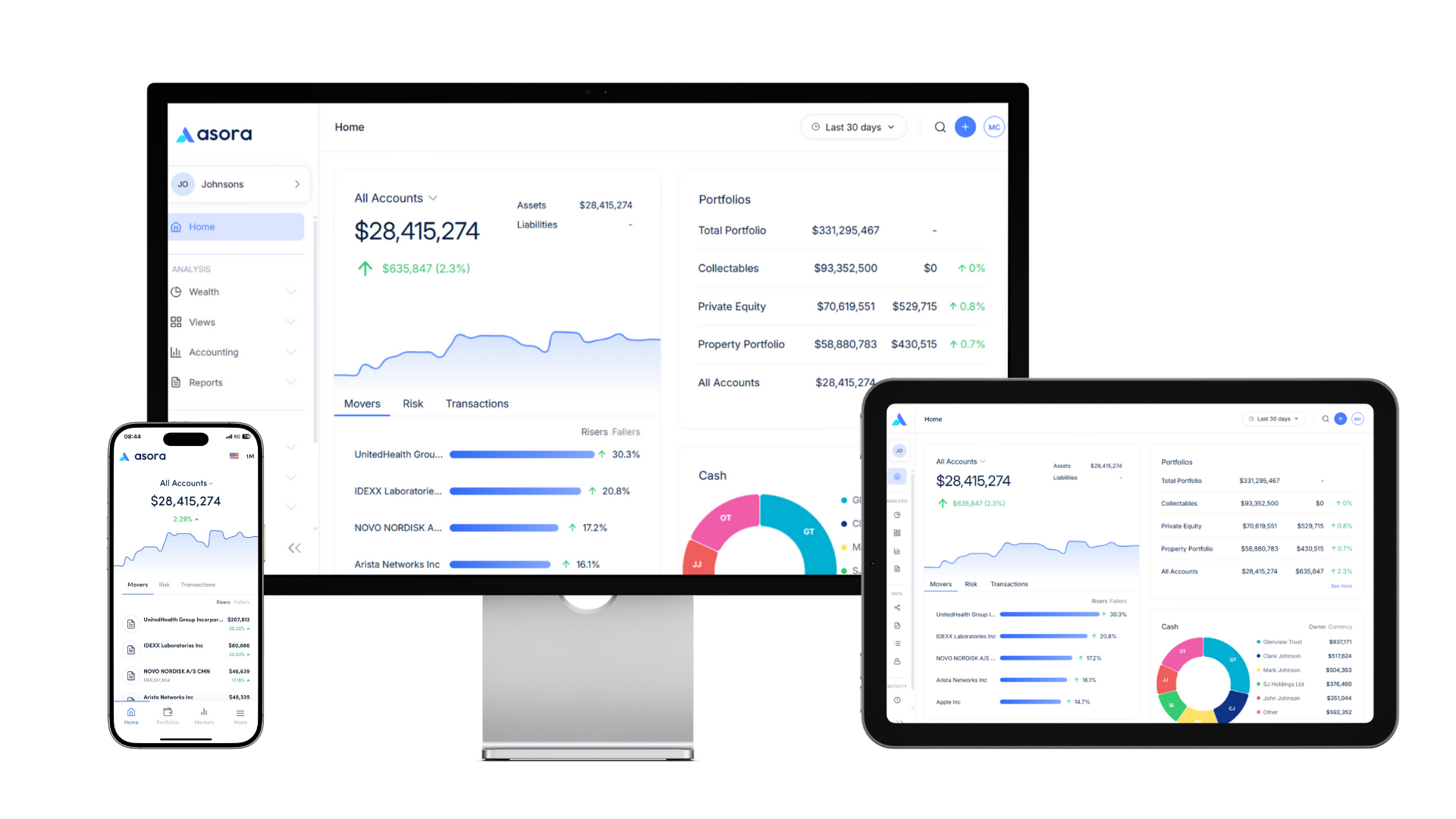

Tools can help, but the process comes first. For context, the liquidity dashboard on Asora provides users with an overview of account, custodian, and portfolio groupings. It keeps policy documents on a single secure platform, and reviews are organized through workflows.

This article explains why liquidity is a strategic lever for family offices and lays out practical steps to build a documented, measurable operating model.

Key Concepts: What Is Liquid Wealth

Liquid wealth management gets easier when everyone uses the same language. Below are crisp liquid wealth definitions you can use in policy documents and board packs.

- Liquid assets / considered liquid assets. Holdings expected to settle quickly at or near market value with minimal cash conversion friction, and can be sold in reasonable size without material price impact, subject to restrictions.

- Typical examples include balances in checking accounts, savings accounts, high-yield savings accounts, money market accounts, institutional money market funds, treasury bills, and settled cash balances in brokerage accounts. Many of these are referred to as cash equivalents in finance (in practice, accounting classification depends on instrument structure, maturity, and risk) because settlement is quick and the value is stable. Money market accounts (bank deposits) differ from money market funds (securities). Exclude margin availability and unsettled proceeds unless explicitly permitted by policy.

- Illiquid assets / non-liquid assets. Positions that require time, fees, or negotiation to sell: private equity, operating companies, real estate, collectibles, funds with gates, or restricted shares. These may generate cash flow, but they cannot reliably be converted to cash quickly without friction, restrictions, or negotiated pricing.

- Liquid net worth. The portion of wealth available quickly after subtracting near-term liabilities. In other words, liquid net worth refers to assets you can actually deploy soon, minus liabilities due in the short run (e.g., credit card balances, tax payments due, upcoming loan amortization. Definitions vary; this should be formalised in policy with included/excluded categories and haircuts). Liquid net worth focuses on spendable resilience, not just paper wealth.

- Total net worth. Total assets minus liabilities across the whole balance sheet, including illiquid assets. When comparing net worth vs liquid net worth, remember: one tells you “how rich on paper,” the other tells you “how ready for action.”

- Calculating liquid net worth (policy choice). Families usually add up their liquid assets and calculate their liquid net worth by subtracting short-term liabilities. Treatment of retirement accounts (e.g., individual retirement accounts) is policy-dependent because early access can trigger penalties and taxes. Some models apply a haircut based on expected tax and penalty impact; others exclude them from the category of “only liquid assets.”

These definitions may feel basic, yet they remove ambiguity in meetings and help a CFO or controller present a consistent dashboard. They also clarify which balances live in the “liquid” column on the family balance sheet, similar to the concept of current assets, though liquidity policies typically apply stricter criteria than accounting current-asset classification.

12 Strategies for Liquid Wealth Management in Family Offices

Before tactics, align on purpose. Liquidity connects today’s obligations with tomorrow’s opportunities. The aim is to protect the financial safety net, fund the investment pipeline, and maintain steady distributions without compromising long-term compounding. The playbook below is designed for lean teams that value clarity over complexity.

1) Size the Emergency Fund to the Real Burn Rate

An emergency fund should be modelled, not guessed. Tally living expenses, recurring distributions, payroll, and known commitments. Many offices hold 6–18 months of cash across checking and savings accounts, money market funds, and treasury bills. Ranges vary widely; some offices rely on committed lines of credit or predictable inflows and hold less, while others hold more due to illiquid exposure and obligations. Larger enterprises often split reserves between “household” and “office” buckets. This buffer prevents forced sales of illiquid assets during shocks.

Policy tip: Put the target range in writing. In Asora, store the policy in Documents, link it to the relevant accounts and entities, and schedule quarterly check-ups with Tasks under Workflows.

2) Segment Liquidity Into Operating, Reserve, and Opportunity Sleeves

Treat cash like a portfolio. An operating sleeve funds the next one to three months in a checking account. A reserve sleeve covers months four to twelve in savings accounts, money market accounts, or short T-bills. An opportunity sleeve captures spread when markets dislocate. Segmenting prevents “cash drift” and improves cash flow discipline.

Visibility matters. Asora’s Data Aggregation pulls balances; sleeves are shown via classification/tagging and reporting views. Performance Monitoring tracks their yield relative to benchmarks.

3) Put Idle Balances to Work With Money Market Funds and T-Bill Ladders

Cash that earns zero loses ground. Money market instruments and treasury bills can provide yield with same-day or short-term access. Ladder maturities to reduce reinvestment risk as interest rates shift. Institutional families often blend T-bills with short-duration bond ETFs to gain additional secondary-market liquidity. This adds mark-to-market risk and is typically used for liquidity-plus sleeves rather than core operating reserves.

Accounting accuracy matters here. Asora Accounting keeps lot/tranche detail for T-bills and funds, and Performance Monitoring tracks results.

4) Decide How Retirement Accounts Fit Your Liquid Net Worth

Retirement accounts and other tax-deferred financial assets bolster long-term security, but they rarely belong in “only liquid assets.” If you include them when calculating your liquid net, apply explicit haircuts for penalties and taxes. Document the rationale so that everyone understands the difference between total net worth and liquid net worth.

Keep the calculation note and the policy version-controlled in Asora Documents; prompt an annual review with a Workflow task.

5) Optimize Brokerage Sweeps, Settlement, and “Cash-Like” Placement

Check brokerage accounts for sweep settings. Directly settle cash into an appropriate money market fund or direct cash sweeps into an appropriate money market fund instead of a zero-yield default. Understand settlement timing for ETFs and bonds; avoid initiating wires relying on unsettled trade proceeds. Minor operational tweaks increase total liquid assets without changing risk.

Keep custodian settings and contacts attached to the entity in Documents for quick reference during transitions.

6) Reduce High-Interest Debt Before Stretching For Yield

Paying down high-interest debt often beats incremental yield on cash equivalents. Prioritize paying off credit card balances and other short-term debts. The result is better financial standing and less volatility in cash needs.

Calculate the impact of high-interest debt and the value gained by early repayment via the Loan Calculator.

7) Diversify Counterparties and Right-Size Bank Relationships

Concentration risk is not just for equities. Spread liquidity across multiple institutions, and ensure the team can move cash quickly within policy. Maintain updated signatories, call-back procedures, and wire templates (where supported); confirm who can act on behalf of principals when they are traveling.

Store mandate letters, signatory lists, and wiring instructions in Documents; schedule “verify signatories” and “wire test” reminders in Workflows to keep the process current.

8) Tie Liquid Planning to the Illiquids Pipeline

Private deals and other investments come with capital calls and distribution schedules. Link your liquidity plan to the illiquid asset pipeline to avoid selling at a loss. Expect distributions to help replenish liquidity, but don’t rely on their timing.

For context, maintain a register of Private Assets in Asora so the liquid side is always viewed alongside the illiquid book.The Wealth Map (ownership chart) clarifies ownership and control across trusts, SPVs, and holding companies.

9) Be Explicit About What Counts As Liquid in Your Policy

Ambiguity causes arguments. Decide in writing whether retirement funds, restricted shares, or funds with notice periods are “liquid,” “quasi-liquid,” or excluded. Clarify how accounts receivable are treated in operating entities when those balances affect family cash. When calculating liquid net worth, use the same policy consistently.

Keep the one-page Liquidity Policy and Liquidity Worksheet in Documents; set Tasks to revisit definitions annually or when structures change; enable viewing/filtering assets by Liquidity on the platform; group Net Worth by Liquidity; create Liquid and Illiquid portfolios (saved views).

10) Build a Reporting Cadence With Stress Tests

Report total net worth and liquid net worth side by side. Show month-over-month changes and drivers. Add simple stress tests, including liquidity-specific shocks such as delayed distributions, clustered capital calls, and reduced credit availability. The point is preparedness, not prediction.

Asora Performance Monitoring provides a timely view of exposures and returns; set a liquidity target, and get in-app alerts if you reach the target. Accounting supports market-value views with lot/tranche detail. Asora provides timely data and supports discrepancy reviews for team-led reconciliation.

11) Keep Cash Governance Simple, Written, and Documented by Process

Good governance is simple: who initiates, who verifies, and when exceptions escalate. Publish it, train on it, and revisit it annually. This protects the financial safety net and reduces friction when roles change.

In practice, teams keep the playbook in Documents and maintain recurring checklists in Workflows (tasks). Approvals and formal records live in your external systems; Asora acts as the organized memory.

12) Teach the Next Generation and Measure Understanding

Liquidity is cultural. Short sessions on examples of liquid assets, the difference between net worth and liquid net worth, and why some holdings are considered liquid while others are not, and how that knowledge pays off during leadership transitions. Tie learning to incentives that reward preserving the liquid cushion instead of depleting it through ad-hoc withdrawals.

Training decks, FAQs, and sign-offs are all live together in Documents

Common Pitfalls (and How to Avoid Them)

Even seasoned teams stumble on the same issues. A few minutes of prevention here protects months of problem-solving later.

- Counting restricted or slow-settlement positions as liquid. If a fund has a notice period or if a bond settles T+1 (or longer, depending on market/instrument, label it correctly. Liquidity definitions should match operational reality.

- Ignoring the debt calendar. Liquidity can look strong until a cluster of repayments arrives. Map the debt obligations calendar, including taxes, balloon payments, and planned debt repayment events.

- Underestimating taxes and fees. Treat tax accruals and expected fees as real short-term liabilities in your calculation of the liquid net worth formula. If liabilities exceed assets, you may show a liquidity deficit (a negative net liquid position), which is an early warning sign.

- Letting definitions drift. Without a written policy, people switch rules mid-stream. Keep a one-pager that defines liquid assets, explains how to treat retirement accounts, and explains exactly how to calculate liquid net worth.

- Over-concentration in one institution. Counterparty diversification is a key component of liquidity risk management. Spread checking, savings, and money market balances intentionally.

- No schedule for review. As interest rates change, revisit money market accounts, T-bill ladders, and sweep options. A quarterly review rhythm keeps yield aligned with policy.

All of these are manageable with simple process discipline. Asora helps by providing a single place to store, link, and retrieve the policy, consolidating views of bank and brokerage accounts, and prompting reviews with Workflows (tasks). The platform supports timely reporting; teams remain responsible for approvals and reconciliation in their external systems.

Conclusion: Liquidity Is the Quiet Edge

For family offices, liquidity is not a passive parking lot; it is an active financial strategy. With clear definitions of liquid assets, a consistent method for calculating liquid net worth, and a twelve-part operating model, families can strengthen their financial security, fund opportunities without drama, and protect their mission when conditions change. The result is reliable distributions, fewer forced sales of illiquid assets, and calmer investment committees.

Asora supports the operational backbone of that strategy. The platform consolidates bank accounts and brokerage accounts through timely Data Aggregation , presents exposures and returns with Performance Monitoring, tracks market values and lots/tranches in Accounting, and maintains registers of Private Assets for context. Policies, wire instructions, and mandate letters reside in Documents, while Workflows (tasks) ensure reviews and maintenance stay on schedule. With everything organized and visible, families can maintain the right blend of more liquid assets and long-term holdings with confidence.

Request a demo to see how Asora helps document, monitor, and manage liquid wealth decisions—so liquidity becomes a dependable advantage rather than a recurring debate.

FAQ

How do you create a comprehensive net worth statement that includes private assets?

Creating a comprehensive net worth statement requires systematic data collection, consistent valuation methodologies, and secure centralization of information. Begin by cataloging all asset classes, from publicly traded securities to private equity investments, property holdings, and alternative assets. Each category requires appropriate valuation: market prices for liquid securities, appraisals for real estate, and fair-value assessments for private holdings. Purpose-built wealth platforms streamline this process by automating data feeds from banks and custodians, as well as providing a secure repository for private asset documentation. Asora aggregates bank and investment data, organizes private asset records and evidence, and produces an on-demand consolidated statement with performance.

How can family offices automate net worth reporting and maintain accuracy?

Family offices can automate net worth reporting by implementing integrated wealth platforms that connect directly to financial institutions and custodians. Automation eliminates manual entry errors and ensures that valuations remain current. Choose platforms that support both bankable assets with automated updates and private assets with workflow tools for periodic valuations. Look for configurable reporting templates and consolidated views across complex entity structures. Security certifications such as ISO 27001 are essential. Asora meets these needs with automated aggregation, workflows, multi-entity consolidation, and ISO 27001-certified security.

What are the common challenges in net worth calculation for complex family wealth?

The primary challenges include data fragmentation across multiple institutions, inconsistent private asset valuations, managing multi-entity structures, ensuring data security, and maintaining current information without excessive manual effort. Illiquid assets, such as private equity and collectibles, are difficult to value due to their infrequent pricing. These challenges are addressed by centralized platforms that aggregate diverse data sources and provide secure document storage and workflow management. Establish clear valuation policies, regular review cycles, and role-based access controls to ensure consistency and security.

.png)

.png)