TL;DR

Many traditional wealth managers still default to quarterly reporting rhythms, especially for formal reviews and illiquid holdings, which can feel too slow for families managing complex portfolios. Modern family offices need wealth management strategies built for 2026: timely data aggregation across custodians, forward-looking liquidity planning for private assets, performance clarity that explains what changed, and mobile access for principals.

Why Wealth Management Must Change in 2026

Wealth management in 2026 looks different from what it did five years ago. Higher allocations to private markets strain traditional portfolio-management workflows and reporting methods, particularly around liquidity planning, valuations, and performance measurement.

Family offices managing $100M–$1B face challenges that traditional wealth management setups struggle with:

- Tracking commitments across multiple private funds and direct deals

- Managing liquidity against unpredictable capital calls

- Consolidating data from multiple custodians

- Making faster decisions with better information

The wealth management strategies that work today combine financial planning with operational infrastructure. You need more than a wealth manager giving investment advice. What you need are systems that aggregate data, accurately calculate performance, track private assets, and give principals mobile access to saved views.

This guide focuses on practical wealth management strategies that high-net-worth individuals and family offices use to manage complex portfolios.

Why Your Private Wealth Management Strategy Needs to Evolve in 2026

Three shifts are forcing family offices to rethink their wealth management plan:

- Higher allocations to private markets. Ultra-high-net-worth families now hold much of their assets in private equity, venture capital, real estate funds, and direct deals. These illiquid investments create cash flow complexity that traditional wealth management services can struggle with. Capital calls arrive with two-week deadlines. Distributions come unpredictably. Valuations update quarterly at best.

- Multiple custodians and banks. Modern portfolios are spread across multiple banks, custodians, and platforms, and each has different reporting formats and update schedules. Aggregating this data manually wastes time and introduces errors.

- Faster decision requirements. Market conditions change quickly. Co-investment opportunities require answers in days, not weeks. Rebalancing decisions need current concentration views, not month-old snapshots. Principals expect mobile access to check portfolio performance and upcoming obligations while traveling.

Family offices need automated data aggregation, liquidity foresight built on actual commitments and calls, documented decisions with linked supporting files, saved views that answer common questions instantly, and regular reconciliation reviews to catch discrepancies early.

10 Strategies For Wealth Management That Family Offices Actually Use

Use this list to prioritise by impact and complexity. Each strategy pairs what to do with the operational deliverable so your team can act on a scheduled cadence and make easier decisions.

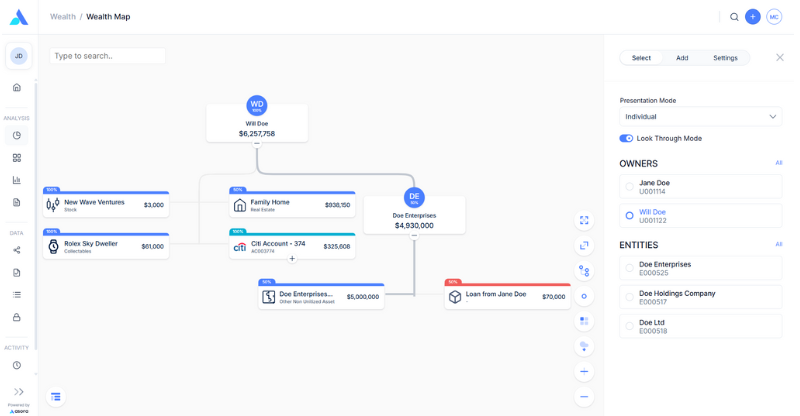

1. Total-Wealth Baseline with Entity Look-Through

Most families can't answer basic questions:

- What's our total worth today?

- How much changed this month?

- What do we owe in the next 90 days?

Information sits across bank portals, investment statements, and spreadsheets.

How to Implement

Aggregate all bank and custodian feeds into one platform. Automated data aggregation pulls transactions automatically with precise dates and currencies.

Map your entity structure. Chart how trusts, special purpose vehicles (SPVs), and holding companies connect to ultimate owners. Use look-through views to see what each family member actually owns through multiple entity layers.

Pick two owner-level headline metrics to review monthly. Everyday choices: change in net worth over the month and total obligations due in 30–90 days. These become your baseline metrics. Frame them alongside a simple view of net worth, liquidity runway, exposure/concentration, and performance vs policy benchmarks; note that headline “net worth change” can be distorted by valuation marks and FX, so use it as context rather than the signal.

The Deliverable

A single consolidated view with owner-level rollups. When a principal asks about the worth of a specific holding, you pull up a single screen.

This baseline enables every other wealth management strategy. You can't plan liquidity, assess concentration, or calculate performance without knowing what you actually own.

2. Liquidity Ladders and Commitment Pacing for Private Assets

Private asset commitments create variable cash demands that require forecasting ranges and buffer planning. A capital call arrives, and you're scrambling to identify funding sources. Or you're holding excess cash earning minimal returns because you can't forecast calls accurately.

How to Implement

Register all private equity, venture capital, and real estate fund commitments in a private assets register. Track commitment terms and build forecast ranges using pacing assumptions, historical call patterns, and GP guidance (updated when capital call notices arrive).

Build a cash ladder showing requirements over the next 6, 9, 12, 18, and 24 months. Include not just private asset calls but also distributions from trusts, insurance premium payments, and any other scheduled obligations.

Surface foreign exchange (FX) exposure where relevant. If you're funding USD calls from EUR holdings, currency movements affect your effective cash position.

The Deliverable

Add an upcoming calls panel that flags commitments most likely to draw in the next quarter, paired with a rolling liquidity view that extends at least 6–9 months (ideally 12–24 months for larger commitment programs). Include a forecast mode that highlights the higher-probability calls for the next quarter, with clearly stated assumptions and confidence ranges.

This supports investment planning by estimating deployable liquidity after reserving for expected calls and near-term obligations.

3. Performance Clarity: TWR for Diversified Portfolios, IRR, and Multiples for Private Assets

Generic performance numbers don't tell you why returns changed. Was it market movement? New contributions? Charitable giving? Currency swings? Fees?

Investment committees need attribution to make asset allocation decisions.

How to Implement

Calculate Time-Weighted Return (TWR) for the liquid/public portfolio at the portfolio level and for aggregated owner or family-branch views. Use it primarily for manager evaluation. TWR removes the impact of cash flows to show pure investment performance. For total-wealth or private-heavy views, pair TWR with money-weighted return (IRR/MWR) to reflect the investor’s experience. Note: “portfolio-level TWR” here refers to the liquid/public portfolio, not the entire family balance sheet.

For private assets, track IRR and multiples (TVPI, DPI, RVPI) at both fund and deal level. These figures rely on GP-reported valuations (and your internal policy for directs). With illiquid investments, cash-flow timing matters more than market timing.

Use a monthly movement bridge that breaks performance into components: flows (contributions, distributions, transfers, fees, taxes), valuation/price changes, FX movements, and other events (gifts, donations, reclassifications). This attribution explains what happened in relation to your financial objectives.

The Deliverable

A reconciliation dashboard that highlights positions or sectors that moved significantly. Principals focus on what changed rather than reviewing static numbers. Performance monitoring becomes strategic instead of backward-looking.

This enables informed investment decisions about rebalancing, manager selection, and new allocations.

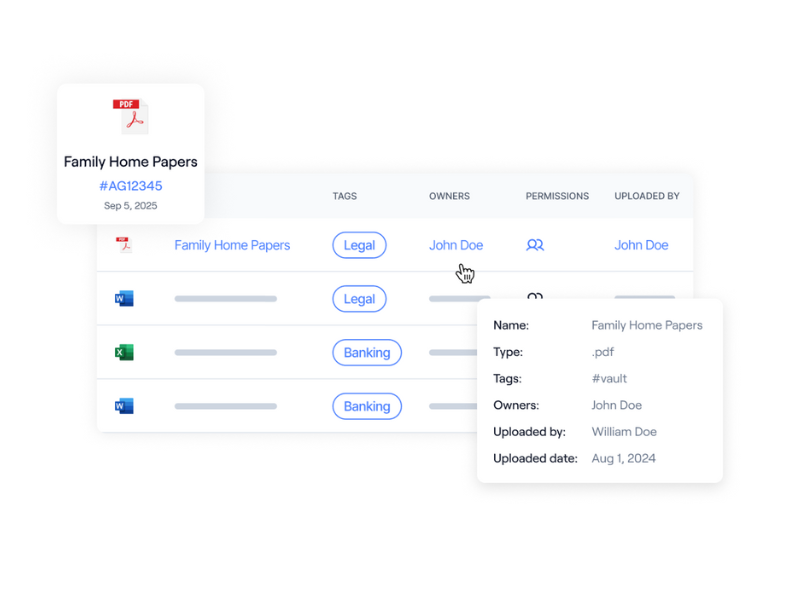

4. Document Discipline: Evidence Beside Every Number

Critical documents live in email attachments, lawyers' folders, and shared drives. When you need a Limited Partnership Agreement (LPA), trust deed, or appraisal, you're hunting through files or asking advisors to resend them.

How to Implement

Store and tag all key documents in one place: trust deeds and related governance documents, LPAs and side letters, valuations and appraisals, tax documentation, and capital account statements.

Link documents directly to entities, holdings, and specific reports. When reviewing a private equity position, the LPA should be one click away. When discussing trust distributions, the trust deed should be immediately accessible.

The Deliverable

A documentation-ready panel reachable from each holding and report. This supports estate planning reviews, tax planning discussions, and operational decisions by giving everyone access to source documents without delays.

Document discipline reduces back-and-forth and helps advisors give guidance faster because the underlying agreements and evidence are readily accessible.

5. Decision Rights and Recurring Task Orchestration

Decision authority is unclear. Can the trustee approve that distribution? Does selling require the trustee, the manager/director, the GP, or the investment committee approval under the entity’s governing documents? Critical tasks like capital call responses, valuation updates, and filings slip through the cracks.

How to Implement

Define signatory thresholds and escalation paths clearly. Document who can approve transactions under what conditions and what amounts require board or family consent.

Template recurring tasks like capital call workflows, quarterly fund valuation updates, entity compliance filings, tax prep deliverables, and annual valuation cycles for direct/private holdings, where applicable. Assign owners, set due dates, and add reminders. Capture reviewer notes next to the task and the relevant asset or holding, so context doesn't get lost.

The Deliverable

A light decision matrix that everyone references and a predictable task cadence that prevents fire drills. This improves operational efficiency and reduces risk from missed deadlines or unauthorized transactions.

6. Reporting Rhythm That Principals Will Actually Read

Most families generate reports reactively when someone requests them. Formats vary, assumptions differ, and period-over-period comparisons become meaningless. Quarterly reports arrive weeks late when the information is stale.

How to Implement

Establish a standard reporting rhythm: typically a monthly snapshot for principals and quarterly deep dives for investment committees. The exact cadence should match your family's preferences and complexity.

Save owner-level views as templates so reports refresh on a scheduled cadence. Provide role-based access or secure exports to advisors, ensuring consent, least-privilege access, and documented distribution controls.

Following automated reporting in wealth management best practices means standardizing reports while allowing customization for different audiences.

The Deliverable

A two-tier reporting cadence that reduces ad hoc data pulls. Principals get consistent monthly updates. Investment committees get quarterly performance attribution and concentration views. Advisors receive scheduled exports without constant requests.

7. Investment Planning Concentration and Risk Snapshots

Hidden concentrations create risk. You think you're diversified, but for example, 45% of investable assets are exposed to technology through direct holdings, funds that overweight tech, and private equity in software companies. Manager concentration is another blind spot. One firm might handle multiple relationships representing 20% of your portfolio.

How to Implement

Visualize concentration across multiple dimensions:

- Sector

- Manager

- Issuer

- Geography

- Currency

Set simple thresholds for outsized exposures based on your investment management plan, financial goals, and risk tolerance.

Estimate liquidation capacity (net of trading constraints, lockups, governance approvals, and tax considerations) over 30/90/180-day horizons. This supports risk management and financial planning for large planned expenditures, distributions, or unexpected cash needs.

Include an FX snapshot where relevant, with drill-downs to positions. Currency exposure matters for international diversified portfolios.

The Deliverable

A concentration dashboard tied to underlying transactions and documents. The investment committee can see exactly where risk is accumulating and make rebalancing calls before concentrations become problems.

This protects long-term financial security by preventing concentration in any single asset class, sector, or manager.

8. Mobile Access For On-the-Go Reviews

Principals travel frequently and need to check portfolio status, review upcoming calls, or verify information during meetings. Waiting until they're back at a desktop slows decisions.

How to Implement

Provide mobile access with Multi-Factor Authentication (MFA) for security. Give principals and operators quick lookups of holdings, upcoming capital calls, saved views, and task lists.

The mobile experience should focus on the most-needed information: current net worth, portfolio performance, obligations in the next 30–90 days, and any flagged items requiring attention.

The Deliverable

A mobile-ready set of saved views and tasks protected with MFA. Principals can check status while traveling, verify information during calls with financial advisors, and approve time-sensitive items without delays.

This supports faster decision-making and keeps principals engaged with their financial situation even during busy periods.

9. Accounting Alignment: Book Values and Lot-Level Fidelity

Performance reports and accounting records show different numbers for the same holdings. Discrepancies often arise because performance reporting uses market values and return methodologies, while accounting records track book values, realised/unrealised gains, and tax or GAAP basis under different timing and valuation rules. Tax situation preparation requires cost basis and lot-level detail that performance systems don't track.

How to Implement

Maintain aligned records (or synchronised systems) for book values and realised/unrealised gains with defined reconciliation between accounting and performance outputs. Track purchases by lot or tranche with acquisition dates to ensure cost-basis calculations for capital gains are defensible.

Keep period consistency across performance and reports. Standardise valuation dates and FX conventions, and ensure they are consistently applied across reporting, performance, and accounting outputs (with exceptions flagged)

The Deliverable

Accounting-ready positions that match performance and reporting views. When your certified public accountant (CPA) asks for cost basis, realized gains for tax planning, or documentation of specific lots, you export clean data.

This is critical for tax-efficient investing strategies and reducing tax liabilities through proper lot identification, tax-aware rebalancing, and loss harvesting where applicable.

10. External Collaboration: Controlled Sharing and Secure Intake

Working with multiple financial advisors, tax providers, and estate planning attorneys creates communication chaos. Your wealth manager wants performance reports. The tax advisor needs the cost basis. The estate planning attorney wants trust documents.

And everything's scattered across email threads.

How to Implement

Schedule reports for external advisors automatically. Your wealth manager receives monthly performance reports. Your accountant gets quarterly transaction details. Everyone sees consistent information on schedule.

Enable secure external upload links for counterparties. Advisors can submit statements, valuations, and notices directly to your system instead of emailing sensitive financial information. Apply tagging rules to route uploads to the correct entity or asset.

The Deliverable

A controlled collaboration loop without email sprawl. You can track what was shared, when, and with whom, and reduce version confusion through controlled distribution.

This improves coordination across your financial advisory team, and that’s non-negotiable when traditional wealth management firms, independent financial advisors, tax services providers, and estate planning attorneys all need access to different data slices.

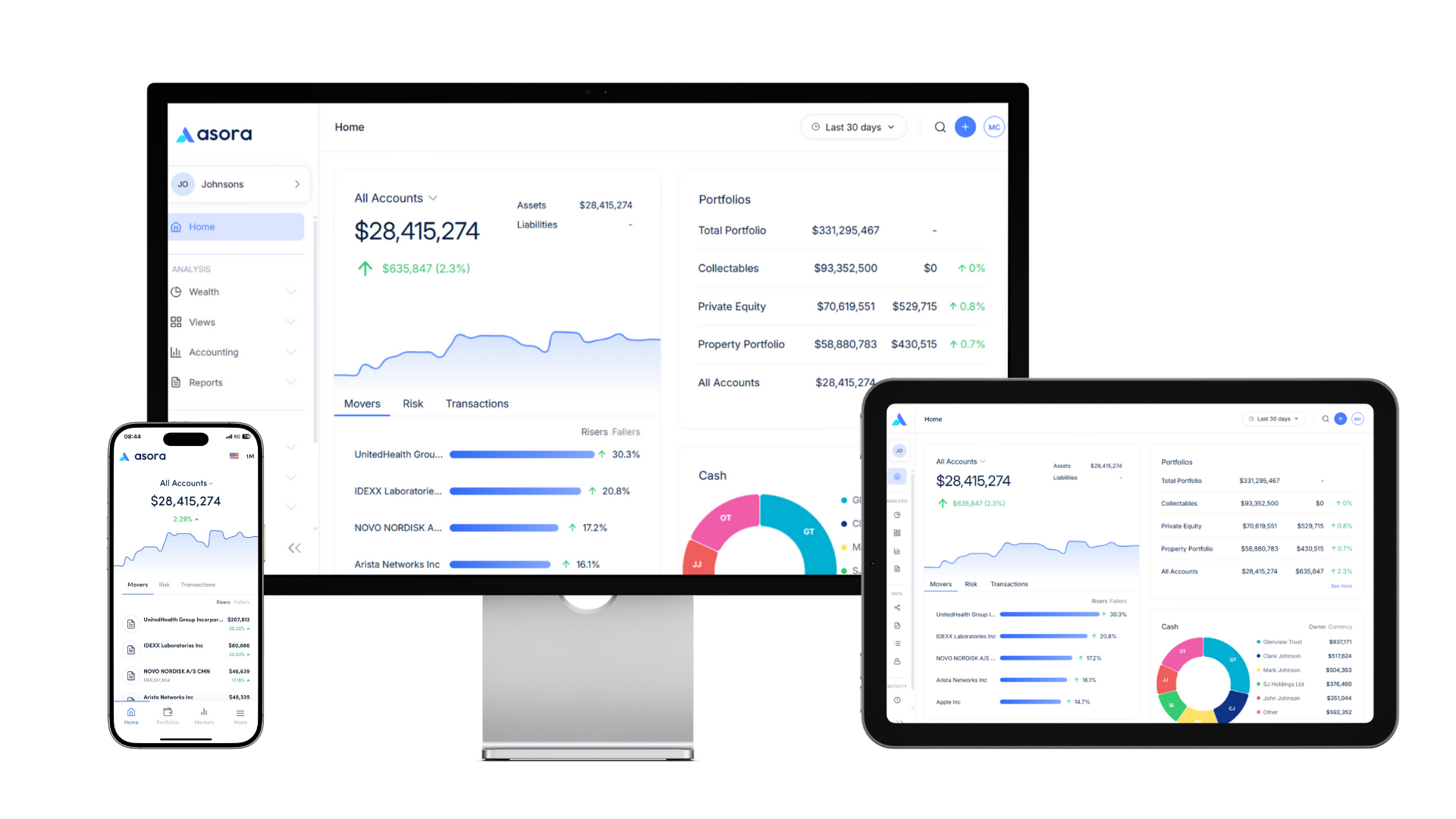

How Asora Powers Your Private Wealth Management Strategy

These ten wealth management strategies require operational infrastructure. Here's how Asora supports your financial future:

- Data Aggregation: Multi-bank and custodian feeds in one centralized platform. Standardize transactions (contributions, distributions, fees, dividends, interest) with precise dates and currencies.

- Wealth Map: Visual entity-to-asset mapping. Chart entity structures and owner look-through views.

- Performance Monitoring: Calculate TWR at the portfolio level and aggregated owner views. Track IRR and Multiples for private assets. Monthly movement bridge and saved review-flags views.

- Private Assets: Track commitments, calls, distributions, and valuations. Monitor unfunded commitments. Link LPAs and side letters to holdings

- Accounting: Realized and unrealized gains, and lot/tranche tracking aligned to reporting periods.

- Documents: Secure vault with tagging. Link files to holdings, entities, and report lines. External upload via secure links.

- Workflows: Assign owners and due dates. Capture reviewer notes at the task level.

- Reporting: Customizable on-demand reporting for different audiences and purposes.

- Mobile with MFA: On-the-go access to worth, upcoming calls, dashboards, and task lists.

Wealth management software supports advisors and internal teams by improving data quality, timeliness, and workflow control. It complements, not replaces, investment advice and professional judgement.

Put These Wealth Management Strategies to Work

Clarity and cadence beat complexity. These ten strategies work because they're focused and repeatable:

Start now with three steps:

- Aggregate data and draw the entity map. Start by pulling data from what you already have: Excel files and CSV exports, plus your custodian and bank feeds. Use that to draw the entity map and show how accounts and entities roll up to each owner. Get this single consolidated view working first; software comes second.

- Stand up the private assets register and liquidity ladder. Input your private equity and venture capital commitments. Build your forward-looking cash forecast for the next 6–24 months. Now you've got visibility into illiquid positions and funding requirements.

- Save your monthly snapshot and schedule the first exports. Create the reporting rhythm: high-level view for principals, detailed performance attribution for investment committees, specific data slices for external advisors. Make these templates run on schedule.

Modern private wealth management strategy combines financial expertise with operational capability. You need both to manage complex portfolios in 2026.

Request a demo to see how these wealth management strategies work in practice. We'll walk through your specific structure (entities, asset classes, custodians, and reporting needs) and show you how Asora supports the operational backbone.

FAQ

How do private wealth management strategies differ from traditional approaches?

Private wealth management strategy focuses on illiquid investments, complex entity structures, and forward-looking liquidity planning. Traditional approaches often struggle when assets are spread across multiple custodians and private vehicles, requiring manual aggregation and reconciliation. Modern strategies require aggregating data from multiple sources, tracking private equity and venture capital commitments, and providing principals with mobile access to current information rather than static quarterly reports.

What role does technology play in modern wealth management strategies?

Technology provides the operational foundation for effective wealth management strategies. Without systems that aggregate data, standardize return calculations, and improve performance accuracy through consistent valuations and reconciled cash flows, even well-designed financial plans fail to execute. Modern family offices need platforms that consolidate information across custodians, provide timely updates, and support mobile access.

How should ultra-high-net-worth individuals approach wealth management differently?

Ultra-high-net-worth individuals typically have higher allocations to private markets, more complex entity structures, and relationships with multiple advisors and custodians. A holistic approach to their wealth management plan should emphasize liquidity forecasting for illiquid commitments, concentration monitoring across holdings and managers, and systems that provide consolidated visibility.

What's the difference between a wealth manager and a wealth management platform?

A wealth manager provides investment advice, portfolio management, and financial planning services. A wealth management platform provides the operational infrastructure: data aggregation, performance calculation, document storage, and reporting tools.

.png)

.png)