Author

.png)

Table of contents

"What used to take hours or days is now done in minutes"

Private equity valuation methods help family offices estimate fair market value across private equity investments, where pricing is infrequent and reliant on models like the market approach, comparable company analysis, and discounted cash flow (DCF). These valuation methods for private companies (including private company valuation methods and asset-based valuation methodology) depend on assumptions around cash flow, market conditions, and comparable companies, so the most effective valuation process triangulates multiple approaches rather than relying on a single model. Ultimately, accurate and decision-useful equity valuation comes from consistent inputs, clear documentation, and strong governance, not just the choice of private equity valuation methodology.

Before diving into private equity valuation methods, it’s important to clarify what “valuation” actually means in a family-office context. The definition shifts depending on how the office participates in private markets and structures its family office operations.

As family offices adopt platforms like Asora to centralize private asset data and reporting, the importance of consistent and well-documented private equity valuation methods continues to grow.

Family offices approach valuation differently depending on their structure and how they engage with private equity:

This distinction matters because it determines how deeply an office engages with valuation methodologies for private equity, including broader valuation methods for private companies and private equity company valuation methods.

At the core of all valuation methodologies for private equity is the concept of fair value: the price that would be received in an orderly transaction. However, in practice:

This layered approach reflects a broader industry reality. Industry research from Deloitte highlights that many institutional investors supplement manager-reported valuations with internal review processes to improve timeliness and confidence in decision-making.

There is also a practical constraint: private markets are not real-time.

“Timely” in private equity does not mean frequent; it means decision-relevant.

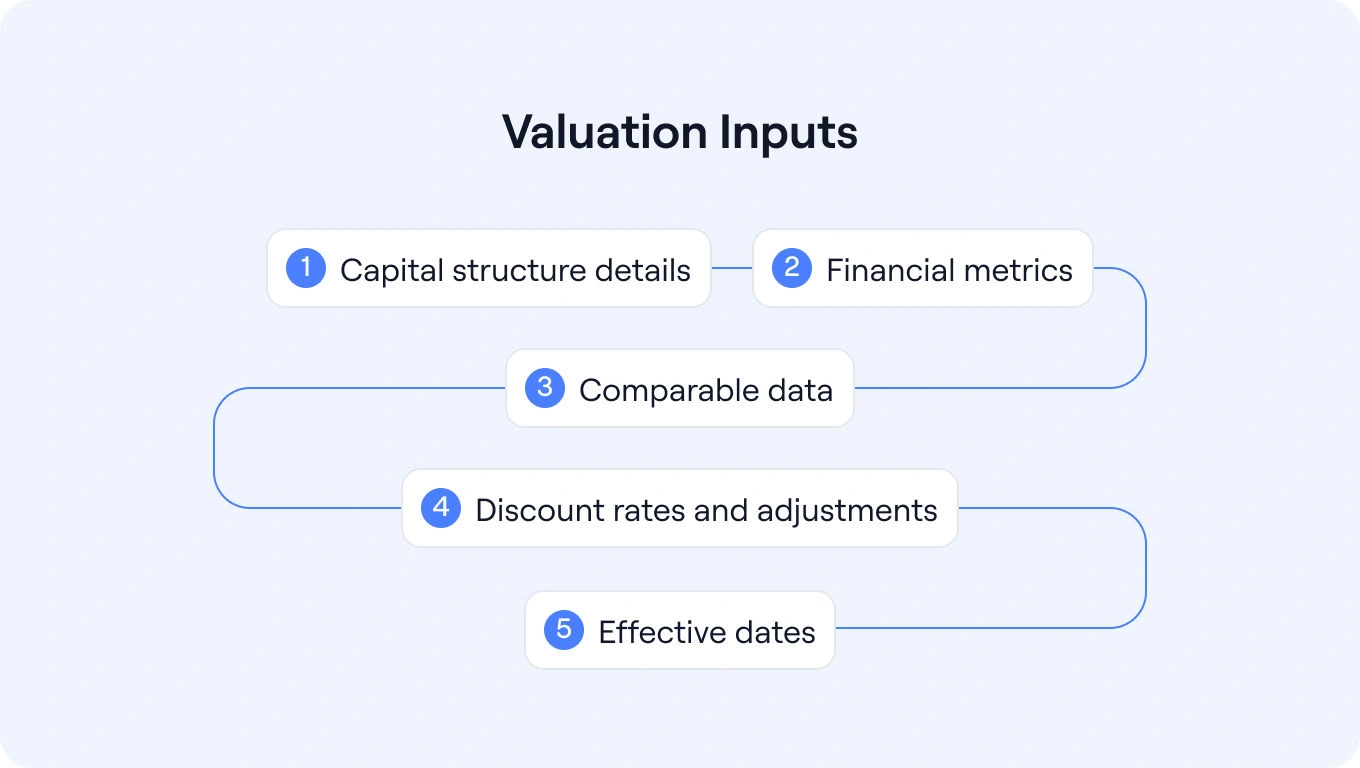

Regardless of the specific valuation methodology private equity teams apply, the same core inputs appear repeatedly. Understanding these inputs is often more important than mastering any single model. At a high level, family offices rely on:

A subtle but important point: the “as of” date is just as important as the valuation itself. Two values calculated using the same method are not comparable if their effective dates differ.

What separates high-quality valuation work from average reporting is how consistently these inputs are applied across the portfolio. For example, using different peer groups, discount rates, or KPI definitions for similar assets can introduce noise that looks like performance but is really just inconsistency.

Leading family offices treat inputs as part of a controlled framework, not a series of one-off decisions. This means documenting why certain comparables were chosen, how discount rates are derived, and when assumptions are updated, so that changes in valuation reflect real underlying movements rather than shifting methodologies. Many family offices rely on platforms like Asora to keep these inputs, assumptions, and supporting documents consistently organized across entities and reporting periods.

No single approach dominates across all situations. The most robust valuation methodologies for private companies combine multiple perspectives, each offering a different lens on value depending on the asset, stage, and available data.

In practice, family offices rarely apply just one valuation methodology in isolation. Instead, they build a repeatable toolkit of methods that can be applied consistently across the portfolio, then triangulate between them to arrive at a defensible view of fair value. This is particularly important in private markets, where limited transparency and infrequent pricing events mean that judgment plays a much larger role than in public equities.

The methods below are among the most commonly used approaches across fund and direct-investing contexts, with method selection depending on the investment’s characteristics. For each, it is important to understand how it works, when it is most reliable, where it can mislead, and how it should show up in quarterly reporting.

The market approach is one of the most widely used private equity valuation methods, particularly for businesses with clear peer groups among publicly traded companies. It provides a market-based lens on value, anchoring the private company’s valuation to observable pricing data from comparable companies, while requiring careful judgment around adjustments for size, liquidity, and growth differences.

When it’s used: Common in buyouts and growth equity, where comparable public companies exist

How it works: Applies valuation multiples (e.g., EV/EBITDA, EV/Revenue) from public peers to the target company

What can mislead you:

What to ask your General Partner (GP): How were comparables selected and adjusted for size, growth, and liquidity?

Quarterly reporting impact: Often used as a baseline method, with adjustments noted in valuation commentary

Precedent transaction analysis builds on the logic of the market approach but looks specifically at prices paid in actual acquisitions rather than trading multiples. Because these transactions reflect what buyers have been willing to pay for control, they can provide a useful benchmark for private company valuation, particularly when market conditions and deal structures are comparable.

When it’s used: When recent comparable acquisitions provide relevant benchmarks

How it works: Uses transaction multiples from similar deals

What can mislead you:

What to ask your GP: How recent and comparable are the selected transactions?

Quarterly reporting impact: Typically used as a secondary validation layer

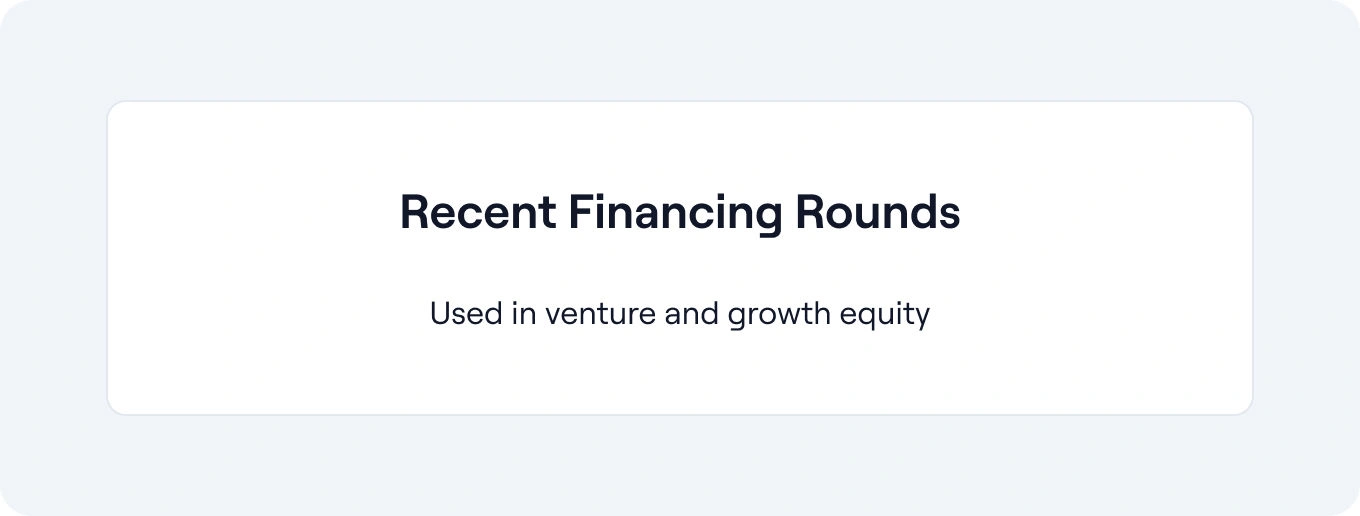

Recent financing rounds are often used as a reference point in venture and growth equity, where traditional valuation methods may be harder to apply due to limited profitability or evolving business models. While these transactions provide a real-world pricing signal, they require careful interpretation, as deal terms, investor protections, and shifting market conditions can significantly influence the implied valuation.

When it’s used: In venture and growth equity

How it works: Uses the price of a recent arm’s-length transaction as a reference point

What can mislead you:

What to ask your GP: What rights or preferences are embedded in the round?

Quarterly reporting impact: Used as a calibration anchor, not a standalone answer

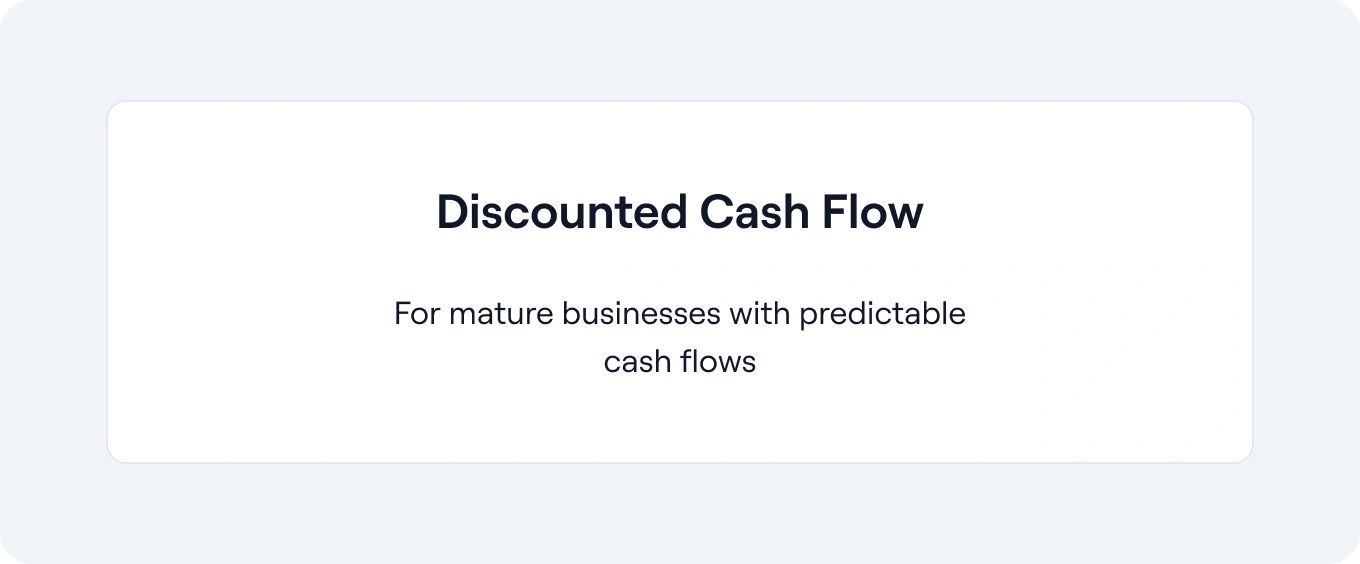

Discounted cash flow (DCF) is a more intrinsic approach to private company valuation, focusing on the company’s ability to generate future cash flows rather than relying on external market comparisons. It is particularly useful where financial performance is relatively stable, but it introduces a high degree of sensitivity to assumptions around growth, margins, and the cost of capital.

When it’s used: For mature businesses with predictable cash flows

How it works: Projects future cash flows and discounts them to present value

What can mislead you:

What to ask your GP: What assumptions drive growth and discount rates?

Quarterly reporting impact: Often used in conjunction with market-based methods

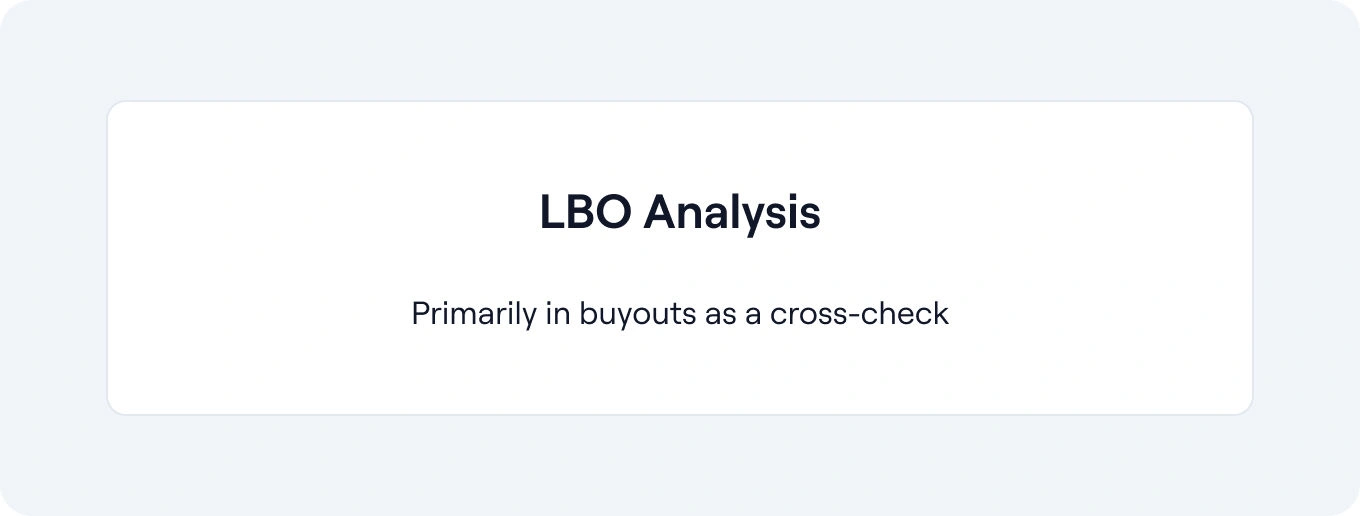

LBO analysis is commonly used in buyout contexts as a way to assess what a financial sponsor might be willing to pay for a business, given target returns and financing assumptions. Rather than directly determining fair value, it serves as a practical cross-check, helping to anchor valuations within the constraints of leverage, cost of capital, and expected exit outcomes.

When it’s used: Primarily in buyouts as a cross-check

How it works: Estimates what a financial sponsor might pay based on return targets

What can mislead you:

What to ask your GP: What IRR thresholds and financing assumptions were used?

Quarterly reporting impact: Used as a reasonableness check rather than a primary valuation

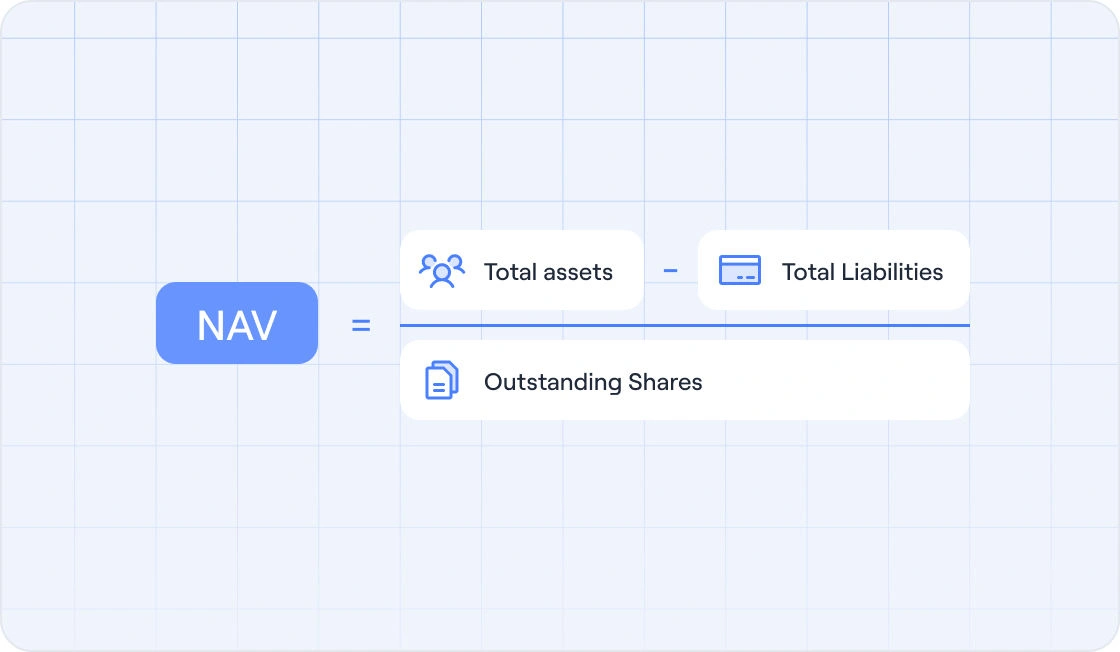

For family offices investing as LPs in private equity funds, valuation is typically based on manager-reported NAV rather than direct company-level analysis. This approach reflects the GP’s view of underlying portfolio value, but because it is both aggregated and lagged, it is often treated as a starting point for monitoring rather than a fully independent valuation.

When it’s used: For LP interests in private equity funds

How it works: Often starts with GP-reported NAV as a practical valuation input for the LP interest, subject to the applicable reporting framework and any factors indicating fair value may differ from NAV.

What can mislead you:

What to ask your GP: What valuation methodologies for private equity are applied at the portfolio company level?

Quarterly reporting impact: Serves as the primary input for LP portfolios

Backsolve methods are widely used in venture capital to infer the value of common equity based on the pricing of preferred shares in recent funding rounds. This approach helps translate complex capital structures into an implied equity valuation, but it relies heavily on assumptions about preferences, dilution, and how value is distributed across different shareholder classes.

When it’s used: Common in venture capital

How it works: Backsolves equity value based on the pricing of preferred shares

What can mislead you:

What to ask your GP: How are preferences and dilution modeled?

Quarterly reporting impact: Typically used alongside OPM or PWERM methods

Option pricing and scenario-based methods are designed for situations where capital structures are complex and outcomes are uncertain, such as early-stage or venture-backed companies. By modeling different exit scenarios and allocating value probabilistically, these approaches provide a more nuanced view of equity value across multiple share classes, though they require careful calibration of assumptions like volatility and timing.

When it’s used: For complex capital structures with multiple share classes

How it works: PWERM allocates value across scenarios using probability weights; OPM allocates value across securities using option-pricing techniques and assumptions such as volatility and timing.

What can mislead you:

What to ask your GP: What scenarios and probabilities are assumed?

Quarterly reporting impact: Essential for venture portfolios with layered capital structures

The asset-based valuation methodology focuses on the underlying value of a company’s assets rather than its future earnings potential. It is most relevant for asset-heavy businesses or situations where the company’s ability to generate future cash flows is uncertain, offering a more conservative view of value based on net asset or liquidation scenarios.

When it’s used: In asset-heavy businesses or distressed scenarios

How it works: Values assets minus liabilities (net asset valuation methodology)

What can mislead you:

What to ask your GP: How were asset values determined and updated?

Quarterly reporting impact: Often used in downside or wind-down cases

In practice, most professional valuations do not rely on a single method but instead combine multiple approaches to arrive at a balanced view of value. A hybrid or triangulation approach brings together insights from market-based, income-based, and asset-based methods, helping to reconcile differences and ensure that the final valuation reflects both external benchmarks and company-specific factors.

When it’s used: Across most sophisticated portfolios

How it works: Combines multiple valuation methods to reconcile differences

What can mislead you:

What to ask your GP: How are conflicting signals resolved?

Quarterly reporting impact: Provides the most defensible and balanced valuation view

In reality, most family office portfolios will contain a mix of these approaches at any given time. A venture investment may rely on last round calibration and option pricing methods, while a mature buyout may lean more heavily on market multiples and DCF analysis. The focus shouldn’t be on choosing the “right” single method, but ensuring that each valuation is supported by a clear rationale, consistent inputs, and appropriate cross-checks.

This becomes especially important when valuations are carried forward across reporting periods, where timing, updates, and data gaps can introduce additional complexity.

Even with strong valuation methodologies for private companies, timing remains a challenge. “Stale” does not necessarily mean incorrect; a value can be the latest official figure while still being outdated for decision-making.

Most family offices operate on a quarterly valuation cycle, aligned with the cadence of GP reporting. In practice, this means that portfolio values are formally updated every three months, often with a lag of several weeks as managers finalize their numbers. This cadence works for reporting consistency, but it does not always align with how quickly the underlying value can change.

As a result, more sophisticated offices treat quarterly valuations as a baseline rather than a constraint. When material events occur, such as a new financing round, a partial or full exit, covenant pressure, or adverse legal developments, there is often a strong case for reassessing value ahead of the next formal reporting cycle. Similarly, observable secondary transactions or meaningful shifts in public market comparables can provide new data points that challenge previously held assumptions.

The practical shift here is subtle but important: valuation becomes event-aware, not just calendar-driven. This can help decision-making reflect current conditions more closely than relying solely on the latest official mark. Maintaining that level of responsiveness often depends on having a clear system in place, which is why many offices use tools like Asora to track valuation updates, supporting data, and event-driven changes in one place.

In private markets, “stale” does not necessarily mean incorrect; it means no longer being decision-useful. A valuation can still be the latest official figure while failing to reflect what is actually happening in the market or within the business itself.

This typically becomes visible in a few ways. A portfolio company’s valuation may remain unchanged across multiple quarters despite clear movement in its sector, or there may be a growing disconnect between public comparables and the implied private market mark. In other cases, delays in GP reporting can leave gaps where the most recent available value lags meaningfully behind internal expectations or external signals.

Over time, these gaps compound. Without clear visibility into which values are current, reviewed, or pending update, it becomes harder to distinguish between true performance stability and reporting inertia.

Given these dynamics, revisions are not a sign of poor process; they are an expected part of private market investing. What matters is how they are handled and communicated.

A practical approach is to clearly separate the official reported value from any management-use estimate or interim view. This distinction can improve traceability and make internal reporting changes easier to explain. When GP updates arrive or assumptions change, revisions can then be reflected transparently, with a clear explanation of what changed and why.

Over time, this creates a more robust reporting framework; one where valuations are not only technically sound, but also traceable, explainable, and aligned with how decisions are actually made.

Even when family offices apply the right private equity valuation methods, the quality of reporting often breaks down at the process level rather than the technical level. The most common issues are about how valuations are implemented, updated, and presented across entities and reporting periods.

One of the most frequent problems is the misalignment between effective dates and reporting dates. In private markets, valuations are always tied to a specific “as of” date, but reporting packs often combine figures from different periods without clearly reconciling them. This creates a distorted view of performance, where movements may reflect timing differences rather than real economic change. Over time, this can undermine confidence in the numbers, particularly when stakeholders are trying to compare quarter-on-quarter trends.

Another recurring issue is the blurring of capital flows and valuation movements. Capital calls, distributions, FX movements, and unrealized gains or losses are fundamentally different drivers of portfolio change, yet they are often presented together without a clear bridge. This can lead to double-counting or, more subtly, to a misunderstanding of what is actually driving performance. A clean reporting structure should always separate these elements so that exposure changes and value changes are not conflated.

In multi-entity structures, inconsistent FX treatment is another source of error. If different entities apply different rates, timing conventions, or translation methodologies, the aggregated portfolio view becomes unreliable. What appears to be a valuation movement may simply be a currency effect applied inconsistently across holdings. Establishing a consistent FX policy and applying it uniformly is a small operational step that has a disproportionately large impact on reporting clarity.

Discounts for illiquidity or lack of marketability should only be applied when supported by the valuation method, facts and circumstances, and the relevant fair value framework. While these adjustments can be appropriate in certain contexts, applying them mechanically or inconsistently across similar assets introduces subjectivity that is difficult to defend. Each adjustment should be tied explicitly to the valuation methodology being used and supported by observable inputs or documented reasoning.

Finally, many reporting packs still rely too heavily on a single valuation methodology across diverse assets. Private equity portfolios are inherently heterogeneous; venture investments, buyouts, and fund interests each require different approaches. Applying the same method across all assets may create the appearance of consistency, but in reality, it reduces accuracy. The more robust approach is to standardize how methods are selected and documented, rather than forcing uniformity in the methods themselves.

Taken together, these issues point to a broader theme: valuation accuracy in family offices is less about model sophistication and more about process discipline, consistency, and transparency.

If valuation methods determine how numbers are calculated, governance determines whether those numbers can be trusted, repeated, and defended over time within a broader governance framework. For family offices, this is where valuation work moves from being technically correct to being operationally robust.

At the center of this is clear ownership of the valuation process. In many offices, responsibility is fragmented across investment teams, finance functions, and external providers. Without a defined owner, inconsistencies inevitably emerge, whether in methodology selection, documentation standards, or update timing. Establishing a single point of accountability, even if execution is distributed, creates the foundation for consistency.

Documentation is the next critical layer. High-functioning offices treat valuation documentation not as a compliance exercise, but as a core part of the investment record. Each quarter, the goal is to capture the output, as well as the reasoning behind it: which valuation methodologies for private equity were applied, what inputs were used, what changed from the prior period, and why. Over time, this creates a record that makes valuations easier to review, challenge, and explain.

In practice, this often takes the form of a standardized valuation memo. The most effective versions are concise, repeatable, and focused on key judgments, rather than being overly technical. They provide enough context to understand the valuation without requiring a full rebuild of the model, which is particularly valuable when portfolios span multiple asset types and geographies.

Equally important is the approval and sign-off process. This does not need to be overly complex, but it should be proportionate to the office’s structure and risk profile. Whether it involves an internal investment committee, external advisors, or a combination of both, the objective is to ensure that valuations are reviewed with appropriate scrutiny before they are finalized and reported.

Many family offices aim to maintain clear evidence trails and consistent documentation, regardless of whether they are subject to formal audits across all entities. This means maintaining clear evidence trails, ensuring consistency across periods, and being able to trace any valuation back to its underlying assumptions and data sources. The benefit is compliance alongside the ability to respond quickly and confidently to questions from principals, advisors, or external stakeholders.

In this context, governance is not an additional layer of work. It is what allows valuation methodologies for private companies to scale across increasingly complex portfolios without losing clarity or control.

Even the most rigorous valuation work loses impact if it is not translated into clear, decision-useful reporting. For family offices, the challenge isn’t just calculating value, but communicating what has changed, why it has changed, and how much confidence to place in the numbers.

A strong quarterly reporting structure starts by focusing on movement. Rather than presenting static valuations, reports should clearly articulate what has changed since the previous quarter and break that movement into its underlying drivers. This typically includes separating capital activity, FX effects, and unrealized valuation changes, so that stakeholders can quickly understand whether performance is being driven by operating results, market conditions, or cash flows.

Alongside this, it is increasingly useful to introduce a valuation status or quality framework. Not all valuations carry the same level of certainty, and treating them as if they do can be misleading. Categorizing values (for example, as manager-reported, internally reviewed, event-adjusted, or pending update) provides immediate context around how much judgment has been applied and whether further updates are expected. This is particularly helpful in periods where reporting lags or market conditions are changing

To support this, family offices should define clear review triggers that determine when a valuation needs to be revisited outside the normal reporting cycle. These triggers might include missing GP statements, covenant breaches, new financing rounds, or delays in expected reporting. By formalizing these conditions, offices can move from reactive updates to a more structured, proactive approach.

Exception tracking is the operational backbone of this process. Rather than allowing gaps or uncertainties to sit implicitly within the numbers, leading offices make them explicit through defined categories such as “missing statement,” “pending support,” “method under review,” or “value pending manager update.” This creates visibility not just into what is known, but into what is still in progress.

Over time, this approach shifts quarterly reporting from a static snapshot to a living view of the portfolio, where valuations are clearly linked to their underlying drivers across the portfolio, assumptions, and data quality. The result is reporting that is not only more transparent but also more aligned with how family offices actually make decisions. Platforms like Asora help bring this together by centralizing valuation data, documentation, and reporting workflows across the portfolio.

Private equity valuation methods are a critical foundation for understanding portfolio value, but on their own, they are not enough. Whether applying a market approach using comparable companies, a discounted cash flow model to estimate present value, or an asset-based approach grounded in net asset value, the real challenge lies in ensuring that these valuation methods are applied consistently across private equity funds, direct investments, and individual private company holdings.

Unlike public companies, where stock prices provide continuous signals, private equity relies on periodic updates and model-driven estimates. This makes the surrounding valuation process (how inputs are selected, how financial statements and cash flow assumptions are interpreted, and how market conditions are reflected) just as important as the valuation methodologies themselves. Without consistent documentation and clearly defined assumptions, even technically sound private equity valuations can become difficult to compare, defend, or use in decision-making.

The most effective family offices, therefore, focus on repeatability and evidence. Using consistent valuation methods, aligned dates, and clear inputs helps ensure that changes in company valuations reflect real performance and market conditions, not differences in how valuations are applied.

This is particularly important when working across multiple private equity firms and fund managers, where underlying methodologies may differ.

As a practical next step, family offices should look to standardize:

Over time, this creates a more robust framework for valuing private companies; one where fair market value is supported by consistent evidence, and where equity valuation decisions are easier to explain, audit, and act on.

If managing private asset records, documents, and follow-ups across entities each quarter is becoming complex, you can request a demo of Asora to simplify and centralize your workflows.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Discounted cash flow (DCF) estimates present value by discounting expected future cash flows using an appropriate discount rate, such as WACC or another required rate of return. It is particularly useful for businesses with predictable financial performance and stable cash flow projections, but it is highly sensitive to assumptions around growth potential and discount rates. As a result, it is often used alongside other valuation methods for private companies rather than in isolation.

Comparable company analysis relies on benchmarking against publicly traded companies or similar companies in the same industry, but truly comparable companies are often hard to find. Differences in scale, market position, financial health, and access to capital can distort valuation multiples such as enterprise value to EBITDA or price to earnings. This makes careful selection of comparable companies and adjustments for company-specific factors essential when valuing private companies.

The asset-based valuation methodology is most appropriate for private companies with significant tangible assets or in scenarios where future cash flows are uncertain, such as distressed situations or wind-downs. In these cases, valuation focuses on the fair value of assets minus liabilities, sometimes under a liquidation premise, rather than on future earnings potential. However, this approach may understate the value of intangible assets or future earnings potential in higher-growth businesses.

Accuracy in private equity valuations depends on a consistent process, sound method selection, reliable inputs, and clear governance rather than on any single method alone. Family offices should standardize documentation, review processes, and reporting conventions, while allowing valuation methods and inputs to vary appropriately by asset type, often supported by centralized platforms like Asora to keep records, documentation, and updates aligned. Clear documentation, periodic review, and structured governance are widely considered best practices for keeping valuations consistent and useful over time.

.png)

.jpg)

.png)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.png)

.png)

.png)

.png)

.webp)